This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Q1 2025: US Treasury Rally Pushes 78% of Dollar Bonds Up as Policy Uncertainty Looms

April 1, 2025

March was a tough month for bond investors, with 72% of dollar bonds in our universe closing the month in the red. This was on the back of the easing in tariff tensions earlier in the month as US President Donald Trump ceased plans to raise tariffs on Canadian steel and aluminum imports to 50%. Also, a US government shutdown was averted at the last minute. Adding to that was the continued steady pace of inflation leading to the Fed maintaining its stance on not moving interest rates in the near future.

However, investors are well in the green on a quarterly basis – Q1 2025 saw 78% of dollar bonds in our universe delivering a positive price return (ex-coupon). Both, investment grade (IG) and high yield (HY) bonds delivered promising returns. 79% of IG bonds and 73% of HY bonds ended in the green respectively. The strong performance was predominantly driven by the rally in Treasuries, given uncertainty over the Trump administration’s tariffs and rising likelihood of rate cuts by the Fed. The strong quarterly performance is on the back of a solid January and February, which saw 69% and 89% of dollar bonds close the month higher.

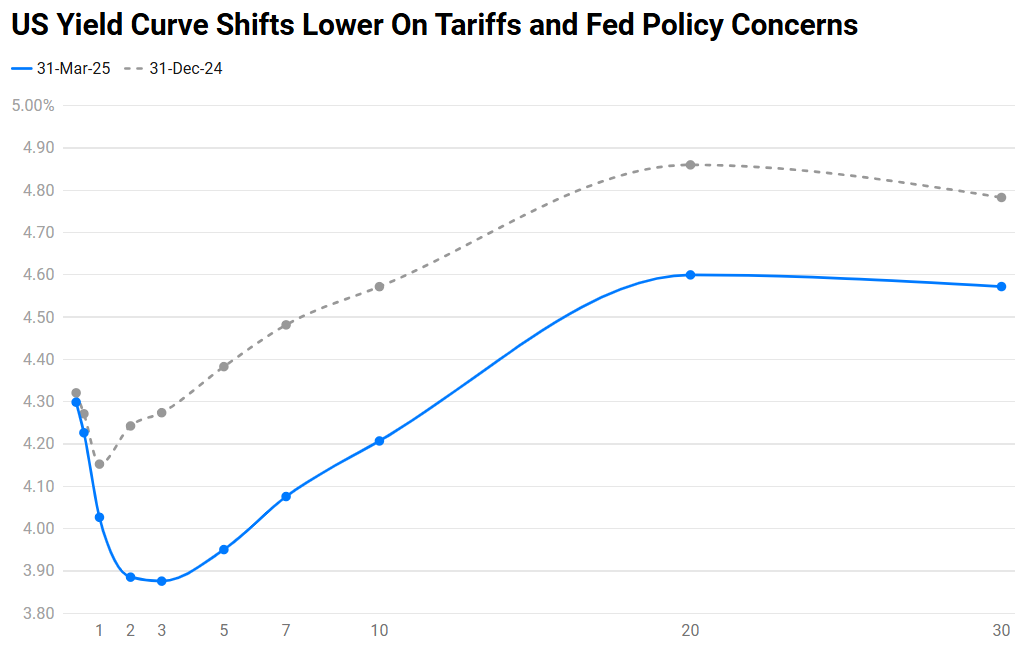

The Treasury yield curve saw a near parallel shift lower during the quarter. The 2Y and 10Y yields ended ~35bp lower, and the belly of the curve i.e., 5Y and 7Y ended 40bp lower. Q1 2025 presented a mixed US economic scenario. Average Non-Farm Payroll (NFP) figures indicated a deceleration in job growth to about 140-150k, while the average CPI readings showed inflation persisting above the Fed’s target, averaging near 2.8%. The average ISM data revealed fluctuating activity, with Manufacturing activity hovering around the 50-mark. Consumer sentiment averaged a decline to roughly 57.0, reflecting concerns about inflation and economic uncertainty brought about by tariffs. This combination of slowing job growth, persistent inflation, uneven industrial activity, and declining consumer confidence shaped the Fed’s cautious monetary policy approach. While the Fed has indicated that there is no urgency for them to cut rates, markets are currently pricing-in 75bp in rate cuts (vs. 50bp expected earlier in March).

Looking at the performance of bonds across bond indices/regions, all regional markets barring Europe performed well. Most other regions like the GCC, LatAm, Asian and US IG sectors and the Asian HY space rose by 2.3-2.7%. The EU region saw a drop in returns, and the US HY space underperformed most of the other indices.

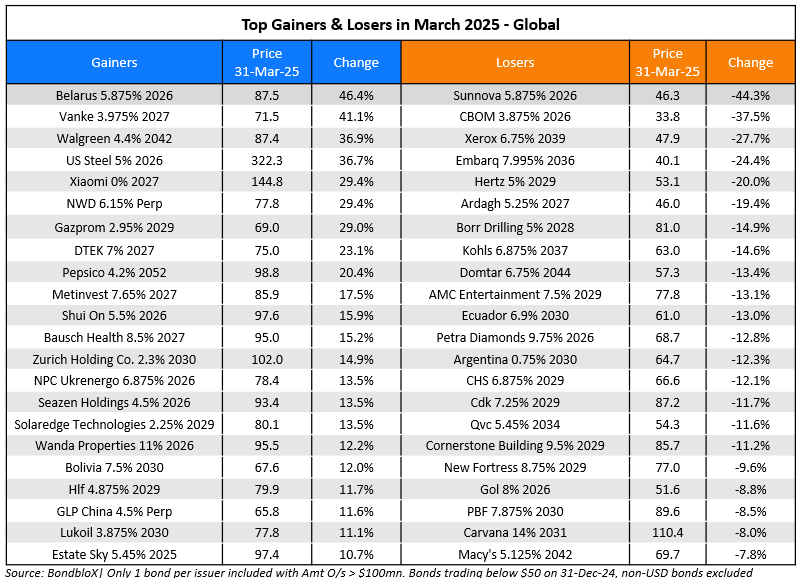

The IG-space saw long-dated bonds of corporates like Pepsico, Israel, BPCE, SBL and others, besides sovereigns like Israel, Colombia etc., again owing to the rally in Treasuries. The losers in this space included bonds of Borr Drilling, Cdk, Petra Diamonds, Domtar and other that fell almost 10%.

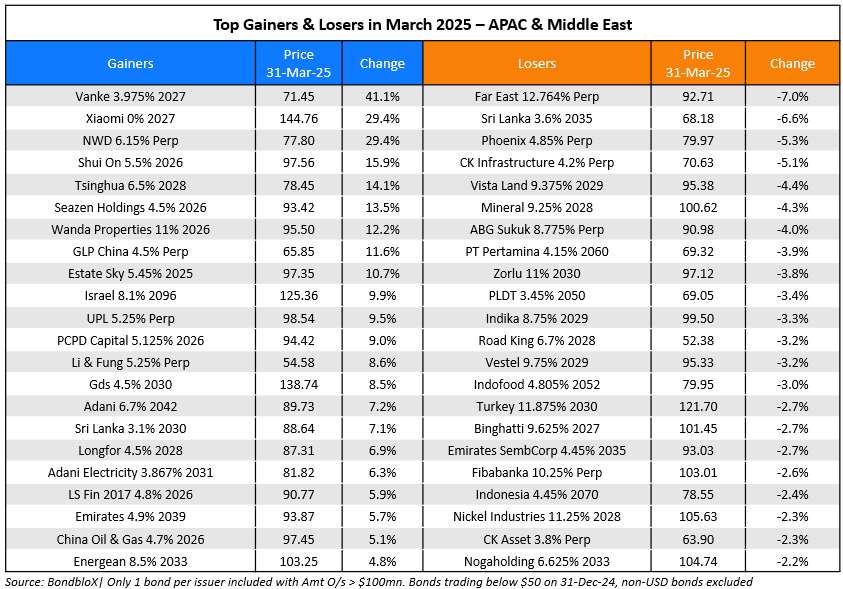

Dollar bonds of Belarus, Gazprom, Metinvest, Lukoil and Russia rallied by over 10-20% during the quarter on the possibility of peace talks led by US President Trump regarding the Russia-Ukraine war. Also, Hong Kong property developer NWD underwent a series of volatile events, – from reporting a loss of $852mn to news regarding potential support for its debt and high demand for its discounted luxury properties. Also, Vanke’s dollar bonds rallied over 20% after it redeemed its onshore notes, following it with support to repay its debt. Walgreens’ bonds rallied over 15% after is sealed a $10bn acquisition by Sycamore. Among the losers, Xerox’s bonds dropped over 20% after it saw a poor financial quarter. Kohls’ bonds fell ~15% amid store closures due to underperformance. Also, automaker Hertz’s bonds fell over 15% amid weak results and management changes.

Issuance Volumes

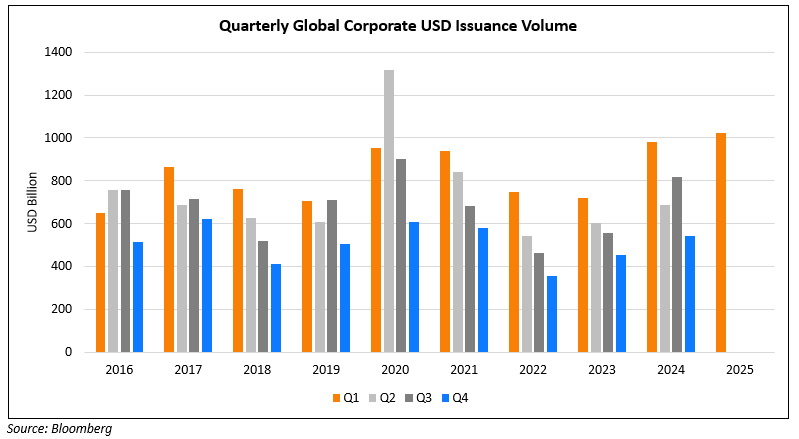

In Q1 2025, global corporate dollar bond issuances stood at over $1.02tn, 4% higher than the same quarter last year which was at $982bn. In comparison to Q4 2024, issuance volumes were 89% higher. Q1’s issuances were also the highest since Q2 2020 where issuers took to the primary markets after accommodative policy following the pandemic.

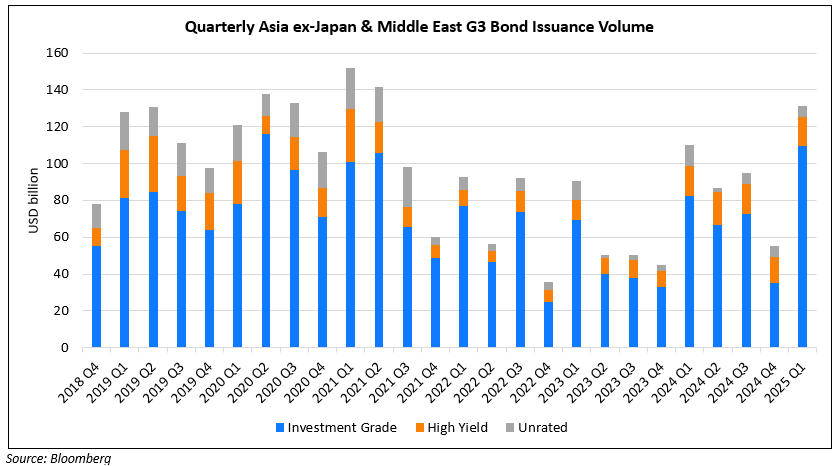

Asia ex-Japan & Middle East G3 issuances in Q1 2025 stood at $132bn, 2x higher Q4 2024, and 20% YoY vs. Q1 2024. 83% of the volumes in the recently concluded quarter came from IG issuers while HY contributed to 12% of deal volumes, with the remainder taken up by unrated issuers.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

High-Yield Bonds Lead The July Recovery

August 6, 2018

Bond Yields – Explained

December 26, 2024

What to Look for When Buying Bonds

December 4, 2024

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.