This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

January 17, 2023

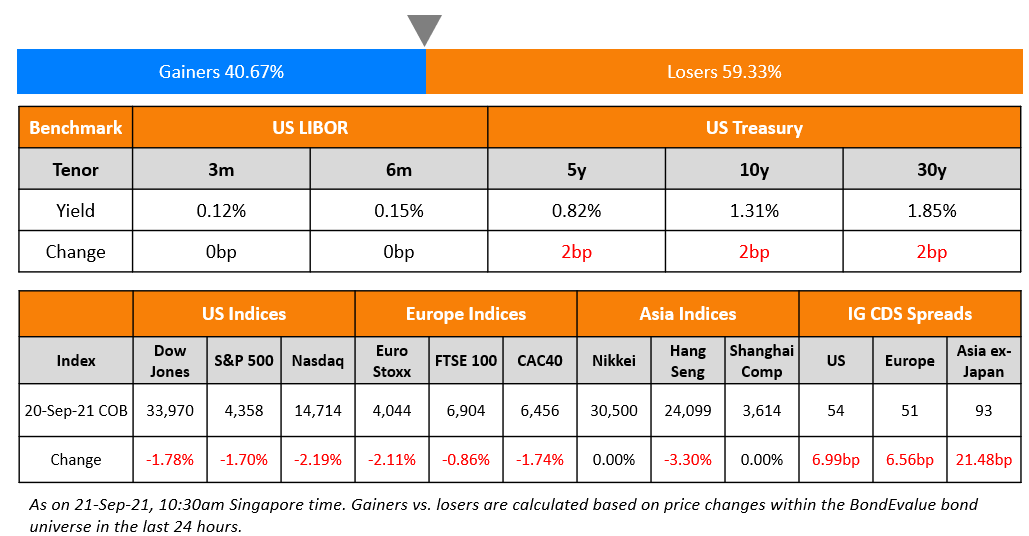

US Treasury yields moved higher by 3-5bp across the curve. The peak Fed funds rate was 1bp higher at 4.93% for the June 2023 meeting. The probability of a 25bp hike at the FOMC’s February 2023 meeting stands at 91%, almost unchanged. US equity markets ended were closed on account of Martin Luther King Day. US CDS markets were also shut.

European equity markets ended slightly higher. The European main and crossover CDS spreads widened by 0.4bp and 6.4bp respectively. Asian equity markets have opened mixed today. Asia ex-Japan CDS spreads tightened by 0.5bp. All eyes now focus on the BOJ’s monetary policy meeting decision due tomorrow where markets are expecting a further alteration in policy. This comes after the BOJ surprised markets in December by tweaking their yield curve control (Term of the Day, explained below) policy where they widened the trading band to allow 10Y JGBs to move 50bp on either side of its 0% target, wider than the previous 25bp band.

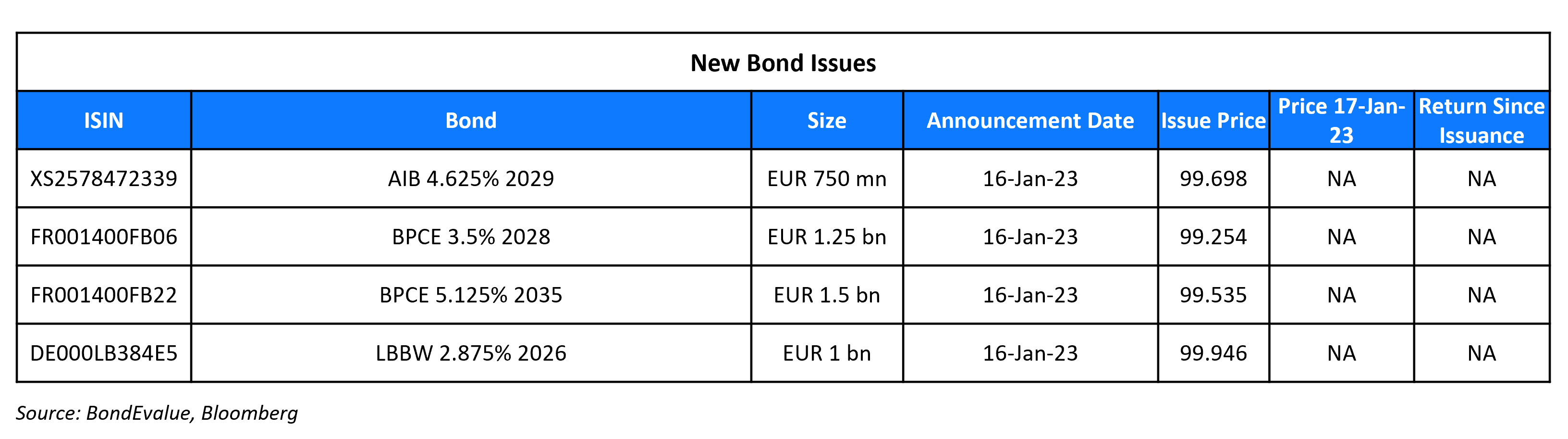

New Bond Issues

- Woori Bank $ 5Y Sustainability at T+175bp area

- Asahi Life Insurance $ PerpNC5 at 7.5% area

BPCE raised €2.75bn via a two-tranche deal. It raised:

- €1.25bn via a 5Y bond at a yield of 3.666%, 25bp inside initial guidance of MS+115bp area. The senior preferred bonds have expected ratings of A1/A/AA-.

- €1.5bn via a 12NC7 bond at a yield of 5.206%, 30bp inside initial guidance of MS+280bp area. The subordinated Tier 2 notes have expected ratings of Baa2/BBB/A-.

Proceeds will be used for general corporate purposes and capital adequacy regulatory purposes.

New Bonds Pipeline

- Khazanah Nasional Bhd hires for $ bond

- Tereos hires for € 300 mn 5NC2 bond

Rating Changes

-

Americanas S.A. Downgraded Multiple Notches To ‘D’ From ‘B’ After Being Granted Injunction Relief

-

Moody’s downgrades Americanas to Caa3; rating under review for further downgrade

- Moody’s downgrades Azure Power Energy to Ba3 and Azure Power Solar Energy to Ba2; outlook negative

- Fitch Downgrades Azure Power Restricted Groups; Maintains Rating Watch Negative

Term of the Day

Yield Curve Control

Yield Curve Control (YCC) is a policy that targets long term interest rates by buying or selling long term bonds to keep the interest rate from rising above it’s target. This is a measure taken to stimulate economic growth. Yield curve controls are also sometimes referred to as Interest Rate Pegs. The Bank of Japan (BOJ) is famous for having a YCC policy in place where they peg the yield on 10-year Japanese Government Bonds (JGB) to fight persistently low inflation.

Talking Heads

On Goldman, UBS Joining Bullish Bets on Global Assets as China Reopens

Paras Anand, London-based CIO at Artemis Investment Management

“We are in the early phase of recovery in terms of asset prices. A recovery or normalization of the Chinese economy will be positive for global growth at the margin”

Fidelity International’s George Efstathopoulos

“This time round the recovery is going to be services- and consumption-led”

Alan Wilson, money manager at Eurizon SLJ Capital

“We think this is a real turning point for the Chinese economy, its underlying assets, and the broader emerging market universe”

On US Dollar Shorts Become Favorite Trade as Fed Seen Slowing Hikes

Patrick Bennett, strategist at CIBC

“Just two weeks into the year, and it feels like the big ‘buy dollar’ trade of 2022 is turning into the hottest macro short now… we are also being driven by a reversal in China with Zero Covid scrapped well ahead of when it was expected.”

Strategists at Morgan Stanley

“Macro forces once constraining USD weakness are now amplifying it. Global growth is showing signs of buoyancy, macro and inflation uncertainty are waning, and the USD is rapidly losing its carry advantage”

On Basis Trade Back in Japan’s Bond Market as BOJ Meeting Nears

Ataru Okumura, a rates strategist at SMBC Nikko

“Some arbitrage trading seem to be going on that involves short positions on cash bonds and long positions on futures. The very low amount of bonds left in the market and the increase in BOJ lending of the securities suggest arbitragers may be borrowing bonds”

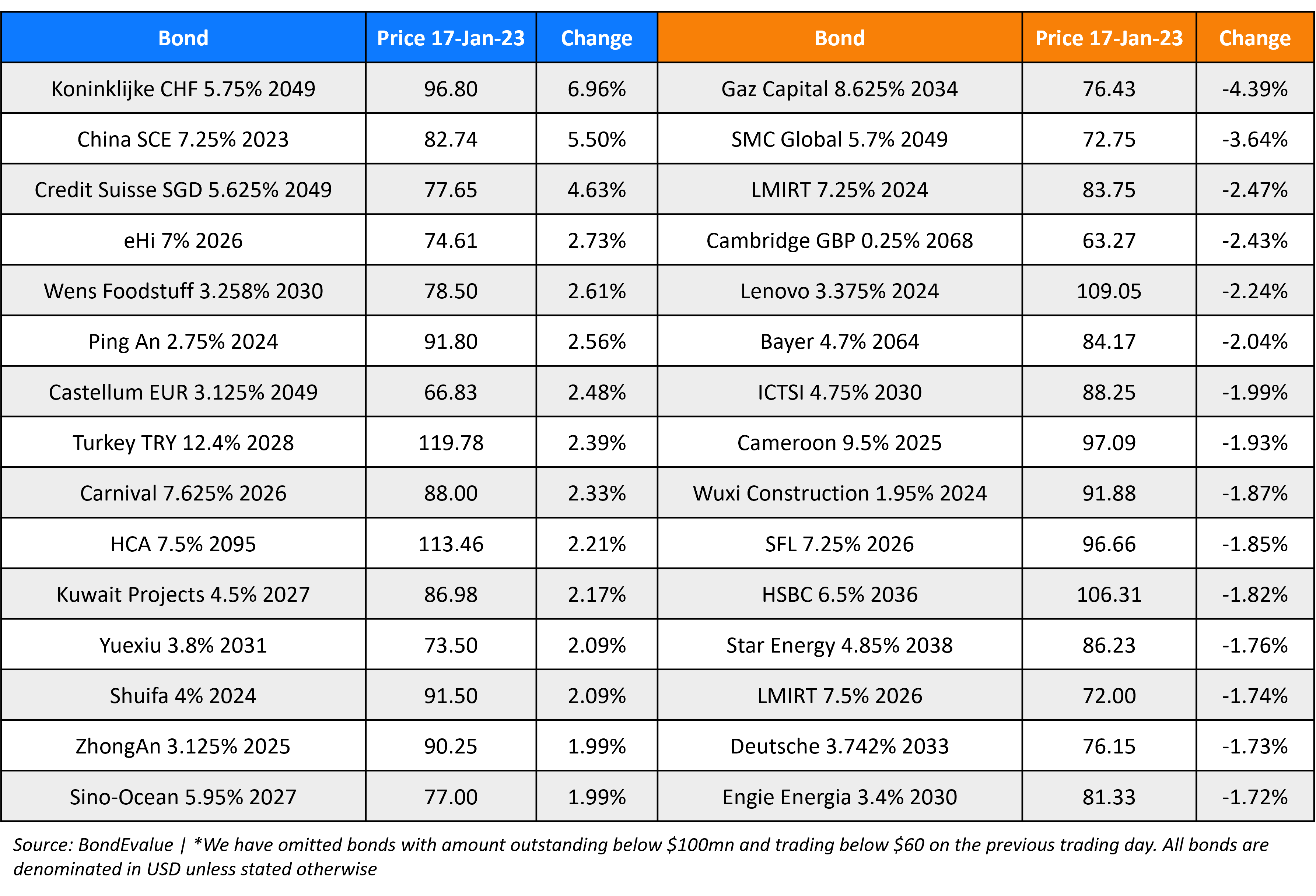

Top Gainers & Losers – 17-January-23*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.