We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Performance of European Bank AT1s and Tier 2s

December 21, 2023

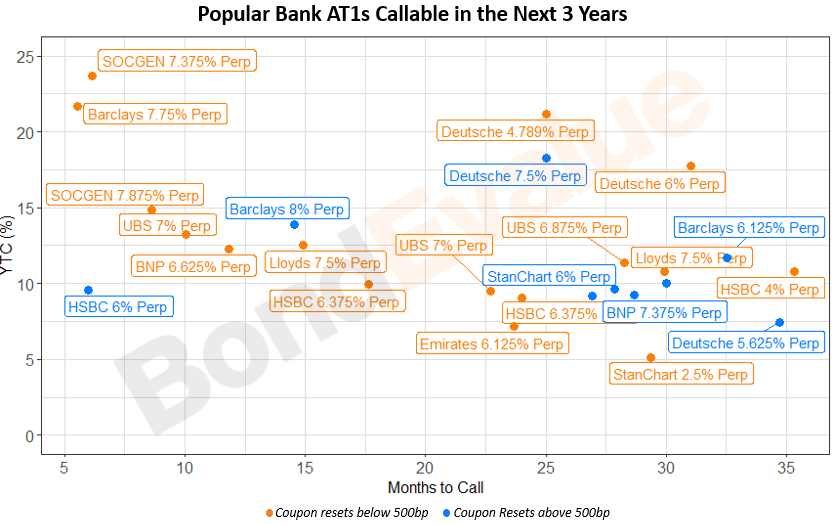

Bank capital forms a key part of private clients’ bond portfolios and 2023 saw its fair share of banking-led credit events. March of 2023 saw the collapse of Silicon Valley Bank in the US and the historic $17.3bn write-off of Credit Suisse’s AT1s following its government-led takeover by UBS. The events sent tremors across global bond markets and put the spotlight on risks associated with AT1s, a favorite among private clients owing to their juicy yields.

As the year progressed and credit spreads tightened, senior bonds performed inline with the broader IG universe, ending higher over the year. AT1s and Tier 2s however saw an impressive recovery from the March lows. For instance, European banks’ dollar AT1s delivered returns of 5.1% this year. In the table below, we have compiled a list of AT1s and Tier 2 bonds from popular European banks, sorted by change in credit spreads through the year. Make sure to switch between AT1s and Tier 2 via the tabs below the title. While page 1-3 lists bonds that saw the most tightening in spreads, page 4 includes bonds that witnessed a widening in spreads.

Our data shows that European Tier 2s outperformed AT1s with a greater spread compression. European AT1 spreads compressed by 5bp on average while Tier 2s compressed by 45bp and senior notes by 49bp. One major theme that stood out was the rally in Italian banks' bonds, on the back of tightening seen in the BTP-Bund spread, a widely followed risk measure, that has compressed 50bp this year to 163bp, near its tightest levels since early-2022. Further, Moody's revised its outlook on the sovereign from negative to stable while affirming its IG-rating of Baa3. Among Tier 2s, Italian banks led the list with Banca Monte, UniCredit and Intesa among the top gainers as seen in the table below. Other gainers in this space included Greece's Alpha Bank and Piraeus Bank that also rose by over 15% this year. Among European AT1s, again Italian banks including Intesa, UniCredit and Banco BPM led the gainers. Julius Baer's AT1s widened the most among European AT1s, following its disclosure of having large exposures to European conglomerate Signa, requiring additional loan loss provisions. Their notes have partly recovered since the announcement.

Disclaimer

The materials and information contained herein are solely for general information reference and educational purposes only, and not intended to constitute nor as a substitute for legal, commercial and/or financial advice from an independent licensed or qualified professional. The information, opinions and views expressed herein are not, and shall not constitute an offer or a recommendation to sell, a solicitation of an offer to buy or an offer to purchase any securities, nor should it be deemed to be an offer, or a solicitation of an offer, or a recommendation, to purchase or sell any investment product or service or engage in any investment strategy. Nothing herein has been tailored to the investment objectives or financial situation of any specific individual, are current only as of the date hereof and may be subject to change at any time without prior notice. No representation, warranty or claim whatsoever is made nor implied as to the accuracy or completeness of any material or information contained herein, nor we have no liability whatsoever for any error, inaccuracies or omissions. No reliance should be made on the materials or information herein for any investment decision, and we accept no liability whatsoever for any direct or indirect loss whatsoever which may arise from the use or reliance of any such material or information. The business of investing is a complicated matter that requires serious financial due diligence for each investment. No representation whatsoever on the suitability or otherwise of any securities, products, or services for any particular investor. Each investor is solely responsible for its own independent investment decision based on its personal investment objectives, financial circumstances and risk tolerance, and should seek its own independent legal, tax and other professional advice prior to any such decision.

The inclusion of any hyperlinks or external links should not be seen as an endorsement or recommendation of that website or the views expressed therein. We do not have any control over the content or actions of the websites we link to and will not be liable for anything that occurs in connection with the use of such websites.

All intellectual property rights, title and interest (including but not limited to copyrights, trademarks, patents and other proprietary rights) in and to these materials and the contents therein, shall remain the sole and exclusive ownership of and are fully reserved by Bondevalue Pte. Ltd.. No licence or rights whatsoever in or to these materials or their contents or any part thereof is granted or deemed to be granted to any recipient. No form of reproduction, dissemination, copying, disclosure, modification, distribution and/or publication of these materials or any part of its contents, shall be permitted.

Go back to Latest bond Market News

Related Posts:

Finding Value in Popular Bank AT1 & Tier 2 Bonds

April 5, 2023

Non-Call Risk in Focus as Bank AT1s Approach Call Date

April 19, 2023

Performance of APAC and Middle East Bank AT1s and Tier 2s

December 21, 2023

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.