We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

November 30, 2022

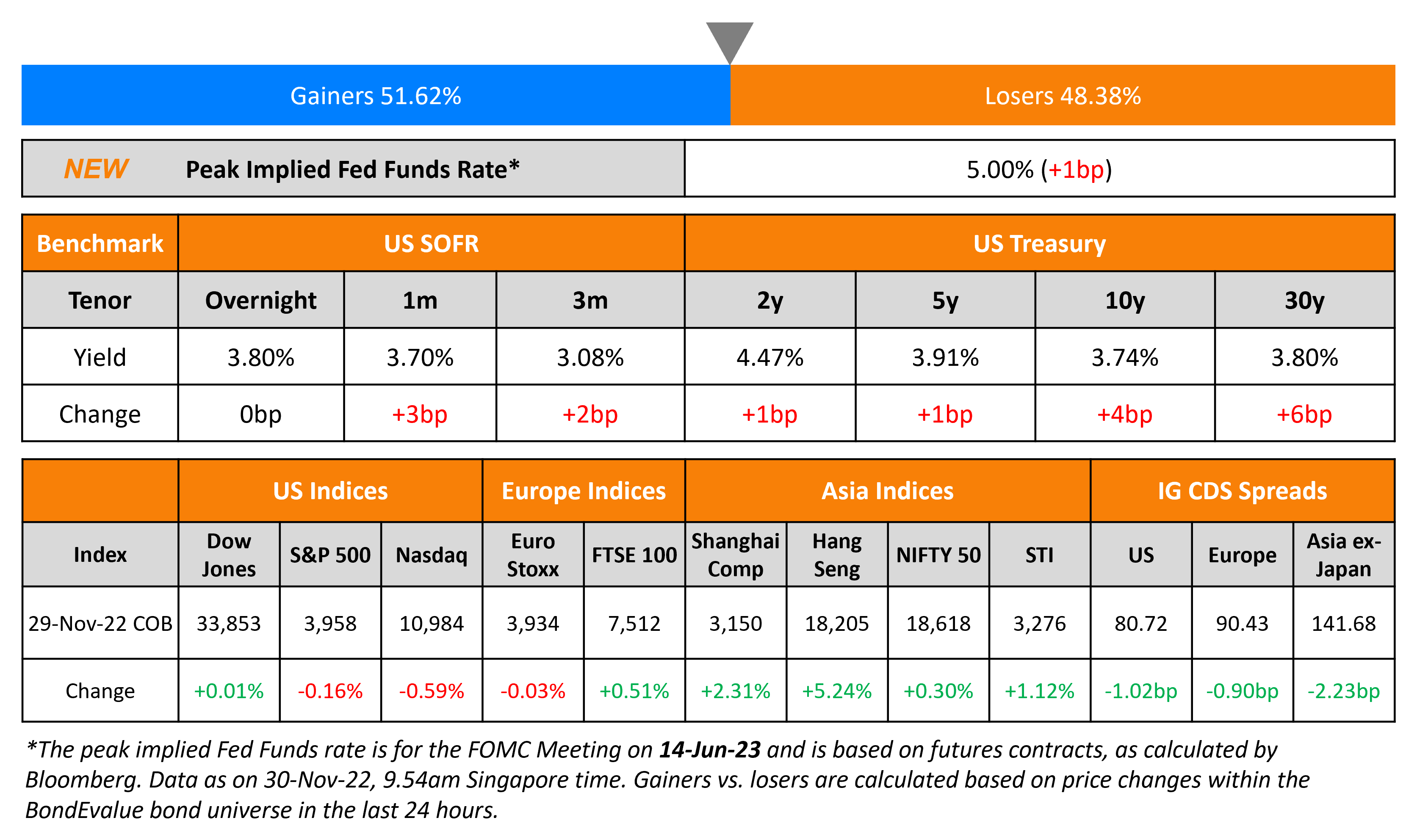

US Treasuries sold off on Tuesday led by the long-end, with 10Y and 30Y yields up 4/6bp to 3.74% and 3.80% respectively. The peak Fed Funds rate also moved 1bp higher to 5.00% for the June 2023 meeting. The probability of a 50bp hike at the FOMC’s December meeting currently stands at 68%, down from 76% a week ago amid hawkish comments by Fed officials this week. All eyes are now on Fed chair Jerome Powell’s speech later today on the future path of interest rates. US IG and HY CDS spreads tightened 1bp and 4.3bp. US equity markets ended with a negative bias led by Nasdaq down 0.6% and S&P down 0.2%. US consumer confidence in November fell to a four-month low of 100.2, down from October’s revised print of 102.2 as persistent inflation and rising rates weigh on sentiment.

European equity markets ended mixed. EU Main CDS spreads tightened 0.9bp and Crossover spreads tightened 4.4bp. Asian equity markets have opened mostly higher with the Hang Seng, Shanghai Composite and Nifty up 0.1-0.2% while Nikkei and STI are in the red. Asia ex-Japan CDS spreads tightened by 2.2bp.

%20x%20311px%20(h).jpg?upscale=true&width=1400&upscale=true&name=Tablet%20banner%20661px%20(w)%20x%20311px%20(h).jpg)

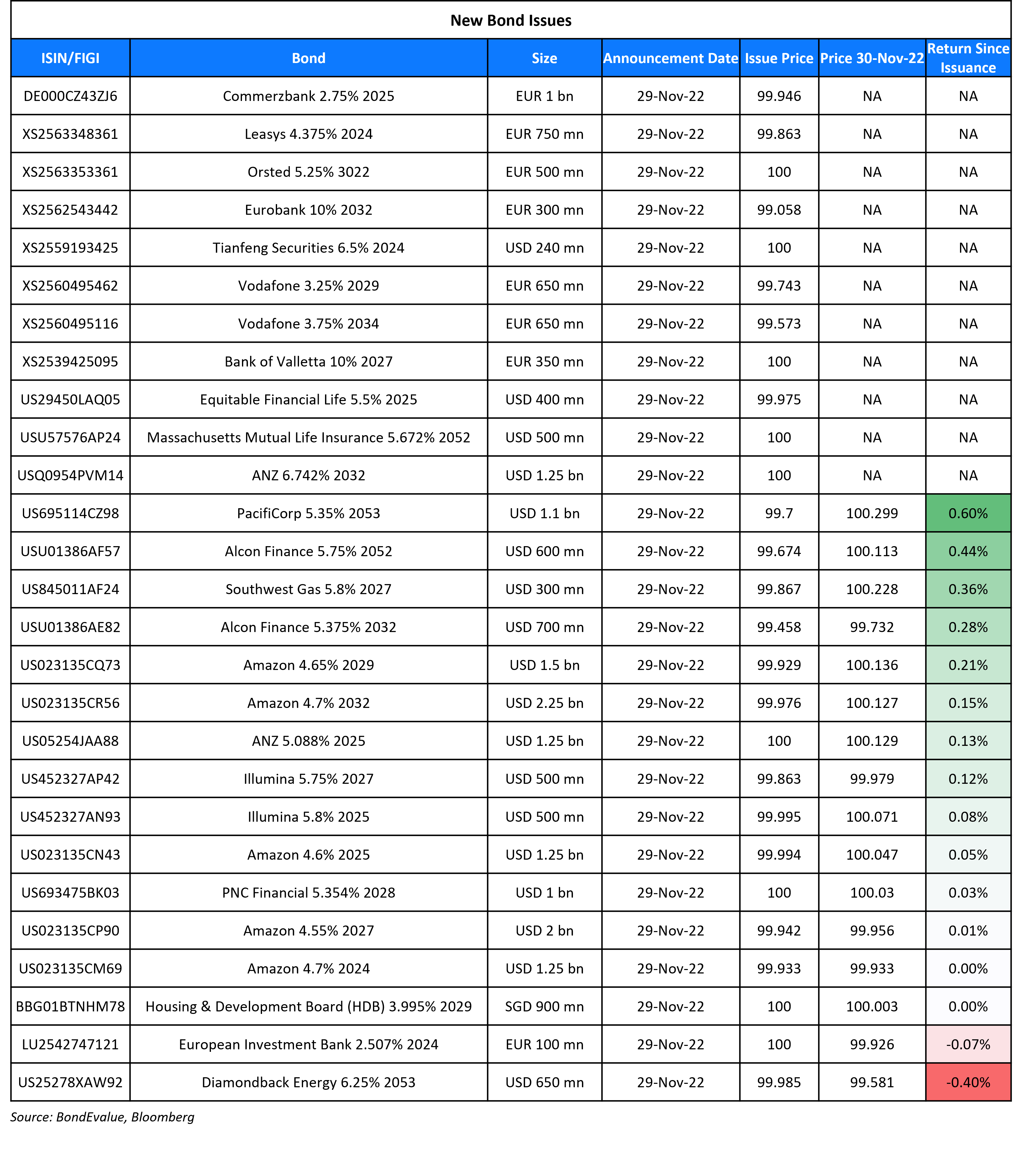

New Bond Issues

- Guilin ETDZ Investment $ 3Y Sustainability at 6.8% area

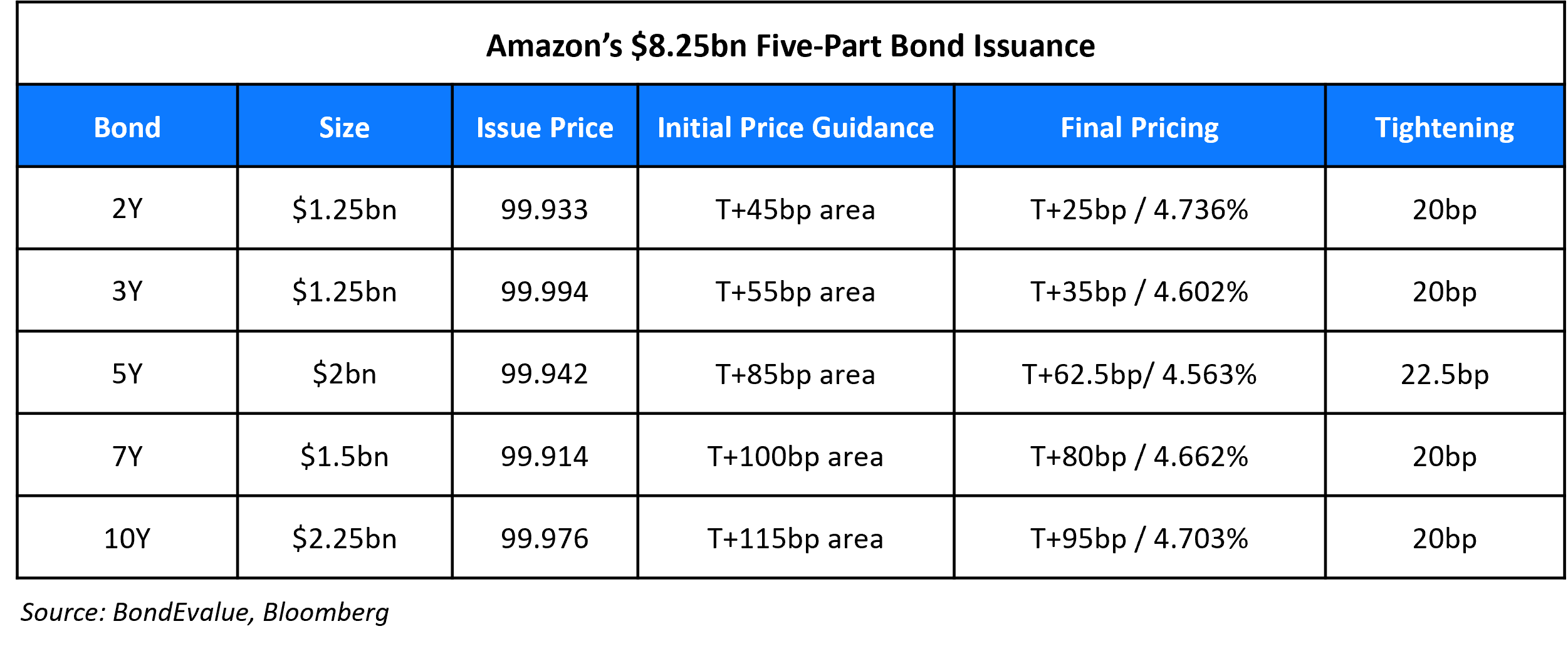

Amazon raised $8.25bn via a five-tranche deal. It raised

The senior unsecured bonds have expected ratings of A1/AA/AA-. The retail giant paid up for the new deal with new issue premiums across all tranches:

- The new 2Y bonds priced at a new issue premium of 5.6bp vs. its existing 3.8% 2024s that yield 4.68%

- The new 3Y bonds priced at a new issue premium of 7.2bp vs. its existing 3% 2025s that yield 4.53%

- The new 5Y bonds priced at a new issue premium of 8.3bp vs. its existing 3.15% 2027s that yield 4.48%

- The new 7Y bonds priced at a new issue premium of 14.2bp vs. its existing 3.45% 2029s that yield 4.52%

- The new 10Y bonds priced at a new issue premium of 7.3bp vs. its existing 3.6% 2032s that yield 4.63%

ANZ raised $2.5bn via a two-tranche deal. It raised

- $1.25bn via a 3Y bond at a yield of 5.088%, 30bp inside the initial guidance of T+115bp area. The senior unsecured bonds have expected ratings of Aa3/AA-/A+. The new bonds are priced at a new issue premium of 17.8bp vs. its existing 3.7% 2025s that yield 4.91%

- $1.25bn via a 10Y Tier 2 bond at a yield of 6.742%, 35bp inside the initial guidance of T+335bp area. The subordinated tier 2 notes have expected ratings of Baa1/BBB+/A-. The new bonds are priced at a new issue premium of 35.2bp vs. its existing 5.548% 2032s that yield 6.39%.

Vodafone raised ~$2bn via multi-currency deal. It raised

- €650mn via a 6.25Y bond at a yield of 3.298%, 32bp inside the initial guidance of MS+100bp area

- €650mn via a 12Y bond at a yield of 3.795%, 32bp inside the initial guidance of MS+145bp area

- £600mn via a 30Y bond at a yield of 5.216%, 25bp inside the initial guidance of UKT+205bp area

The senior unsecured bonds have expected ratings of Baa2/BBB/BBB.

Singapore’s HDB raised S$900mn via a 7Y bond at a yield of 3.995%. The senior unsecured bonds have expected ratings of AAA. Proceeds will be used to finance development programs and working capital requirements. The new bonds priced at a new issue premium of 15.5bp vs. its existing 3.08% 2030s that yield 3.84%.

New Bonds Pipeline

- Korea Investment & Securities hires for $ Green bond

- Zhongrong International Trust hires for $367mn Short 1Y bond

- Kunming Rail Transit Group hires for $ Green bond

- Deyang Development hires for $ Sustainability bond

Rating Changes

-

Moody’s downgrades Ghana ratings to Ca with a stable outlook, concluding its review

-

Moody’s places BHP’s ratings (A2 issuer rating) on review for upgrade

Term of the Day

SLB Trigger

SLB trigger refers to an event wherein an issuer fails to meet a pre-defined KPI on its sustainability-linked bonds (SLB), which leads to a penalty on its bonds. The most commonly seen penalty is a coupon-step up.

The ESG bond markets witnessed the first-ever SLB trigger on Poland-based PKN Orlen’s local-currency SLBs, which had KPIs linked to the issuer’s ESG rating. The company’s ESG rating was recently cut by MSCI from A to BBB, which led to a trigger on its SLBs leading to a coupon step-up.

Talking Heads

On the recent rally in bond markets

Omar Slim, a fixed-income portfolio manager at PineBridge Investments

“We are starting to see a number of economic indicators that point to the fact that inflation has peaked or is peaking…While trading in US Treasuries is likely to be volatile amid economic data and Fed rhetoric, the bond market rally ‘has legs.'”

Steven Boothe, portfolio manager and head of the investment-grade fixed income team at T. Rowe Price Group Inc.

“This hiking cycle is going to extend for longer than people anticipate…The market was a bit over-hedged so it didn’t really take much in terms of relatively good news in order to get this snapback rally. I would not expect this to persist.”

“We are in an ongoing base money-destruction mode from the central bank tightening, so outflows should be the central tendencies for all asset classes on aggregate…Clearly at this time of year, some money gets taken out of the market, particularly if performance has recently been strong, which with LQD it has.”

On muted Latin American bond issuances

Teresa Alves, an analyst at Goldman Sachs Group

“The potential for rates to stay at current levels or go higher is probably deterring issuers from coming to the market…hat is likely to remain an issue until we reach peak hawkishness.”

Phil Torres, global co-head of emerging-market debt at Aegon Asset Management

“If the world continues like this for another 18 months of high stress and high yields, we may see bankruptcies among companies that aren’t able to roll over their debt.”

Andre Silva, head of Latin America debt capital markets for BNP Paribas

“The hope is that we’ll start to see more issuance activity next year, first from sovereigns and quasi-sovereigns, and then corporates…Once the market tests a few names, investors may get more confident about testing BB+ and BB credits.”

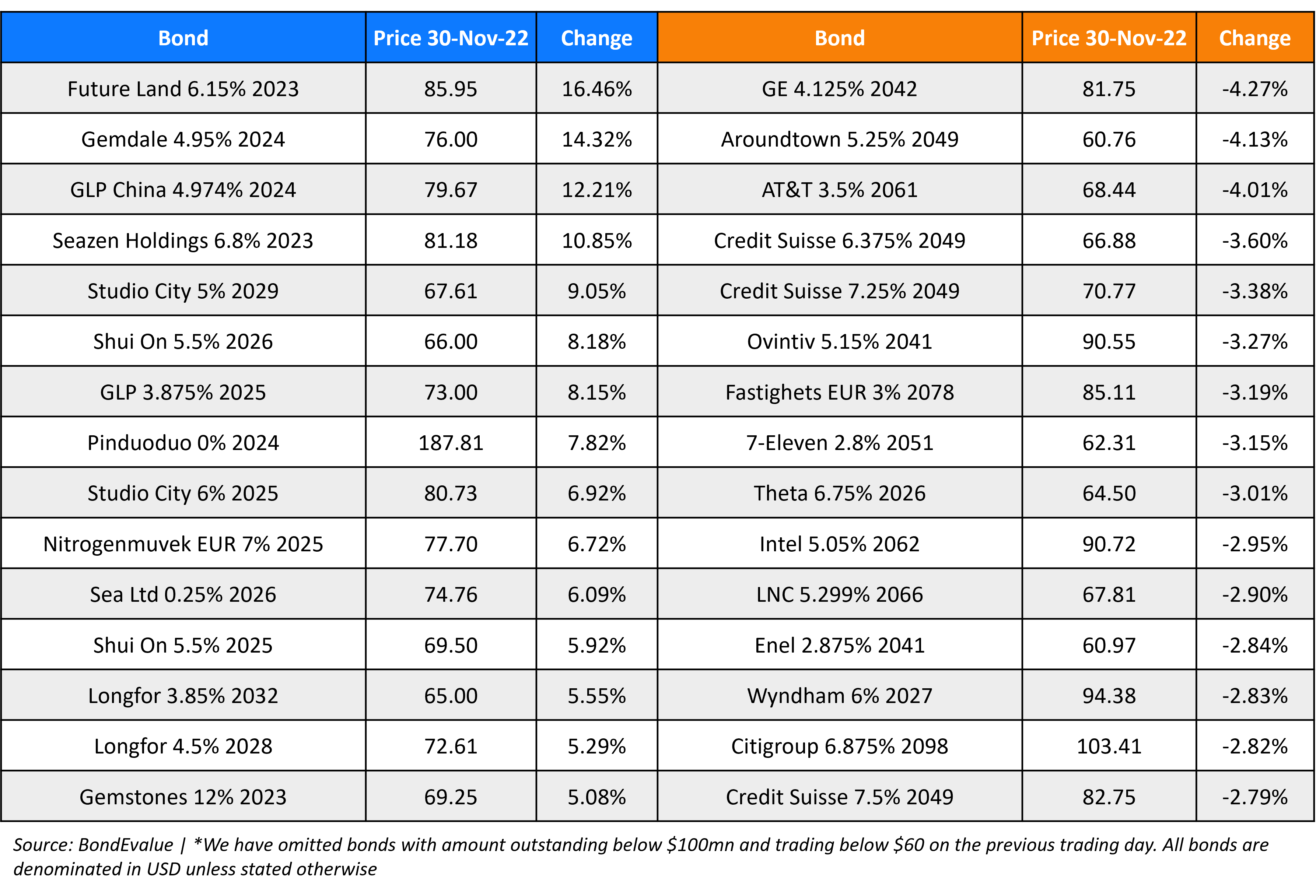

Top Gainers & Losers – 30-November-22*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.