We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Fed Continues to Indicate 75bp Rate Cuts in 2024

March 21, 2024

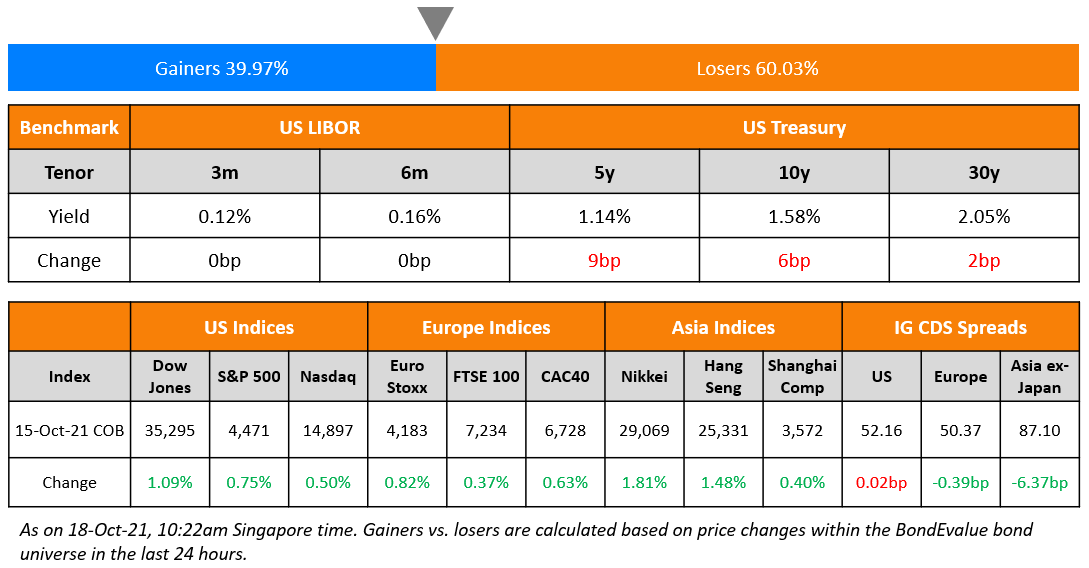

The US Treasury yield curve bull steepened with the 2Y and 5Y yields down 10bp and 7bp respectively while the 10Y yield was down 3bp. The Fed kept its policy Fed Funds Range unchanged at 5.25-5.5% as expected, for a fifth straight meeting. Policymakers maintained their outlook for 75bp in rate cuts for 2024. However, even as the median dots for rate cuts remained unchanged, more members now anticipate fewer rate cuts than December’s dot plot projections. Policymakers also moved toward slowing the pace of reducing bond holdings, suggesting they aren’t alarmed by a recent uptick in inflation. While Jerome Powell continued to highlight that officials would like to see more evidence that prices are coming down, he also said it will be appropriate to start easing “at some point this year”.

-gif.gif)

Credit markets saw US IG CDS spreads widen 3bp and HY spreads widen by 8.5bp. Looking at equity indices, S&P and Nasdaq rose 0.9% and 1.3% respectively.

European equity indices closed flat. European IG CDS spreads widened 3.2bp and HY spreads were 8.8bp wider. Asian equity markets have opened in the green today. Asia ex-Japan IG CDS spreads were 4bp wider.

New Bond Issues

-

Jinan Energy $ 1Y Green at 6.4% area

New Bond Pipeline

- Korea National Oil hires for $ 3Y/5Y bond

- Indiabulls Housing hires for $ 3.25Y bond

- Deqing Construction hires for $ bond

Rating Changes

- Fitch Upgrades Qatar to ‘AA’; Outlook Stable

- Moody’s downgrades Intrum’s corporate family rating to B3 and senior unsecured debt rating to Caa1; places all ratings on review for downgrade

- Fitch Revises Outlook on Nemak to Negative; Affirms IDR at ‘BBB-

Term of the Day

Fed Dot Plot

The Fed dot plot is a visual representation of interest rate projections of members of the Federal Open Market Committee (FOMC), which is the rate-setting body within the Fed. Each dot represents the Fed funds rate for each year that an anonymous Fed official forecasts. The dot plot was introduced in January 2012 in a bid to improve transparency about the range of views within the FOMC. There are typically 19 dots for each year, representing the median rate of each voting member on the committee.

Talking Heads

On Short-End Bonds Rally as Fed Reassures Market of Cuts in 2024

Zachary Griffiths, head of US investment grade and macro strategy at CreditSights

“This seems more dovish than market anticipated with no change to the 2024 median dot”

Ben Emons, a senior PM at Newedge Wealth

“Projections are bullish-hawkish in that they are bullish on the economy — higher GDP/lower unemployment — and hawkish on inflation”

On Funds Selling Indonesian Bonds on Fiscal Fears, Free Lunch Pledge

Goldman Sachs strategists

EM-focused real money and hedge funds have “expressed concerns over potential fiscal loosening by the new incoming government”

Jon Harrison, MD for EM macro strategy at GlobalData

“It is important that any fiscal expansion is done in a sustainable way – so we should watch the spending pledges carefully”

Top Gainers & Losers- 21-March-24*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.