We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

APAC Issues Ramp Up Issuances; SoftBank, Mizuho, Nomura Launch $ Bonds

June 27, 2024

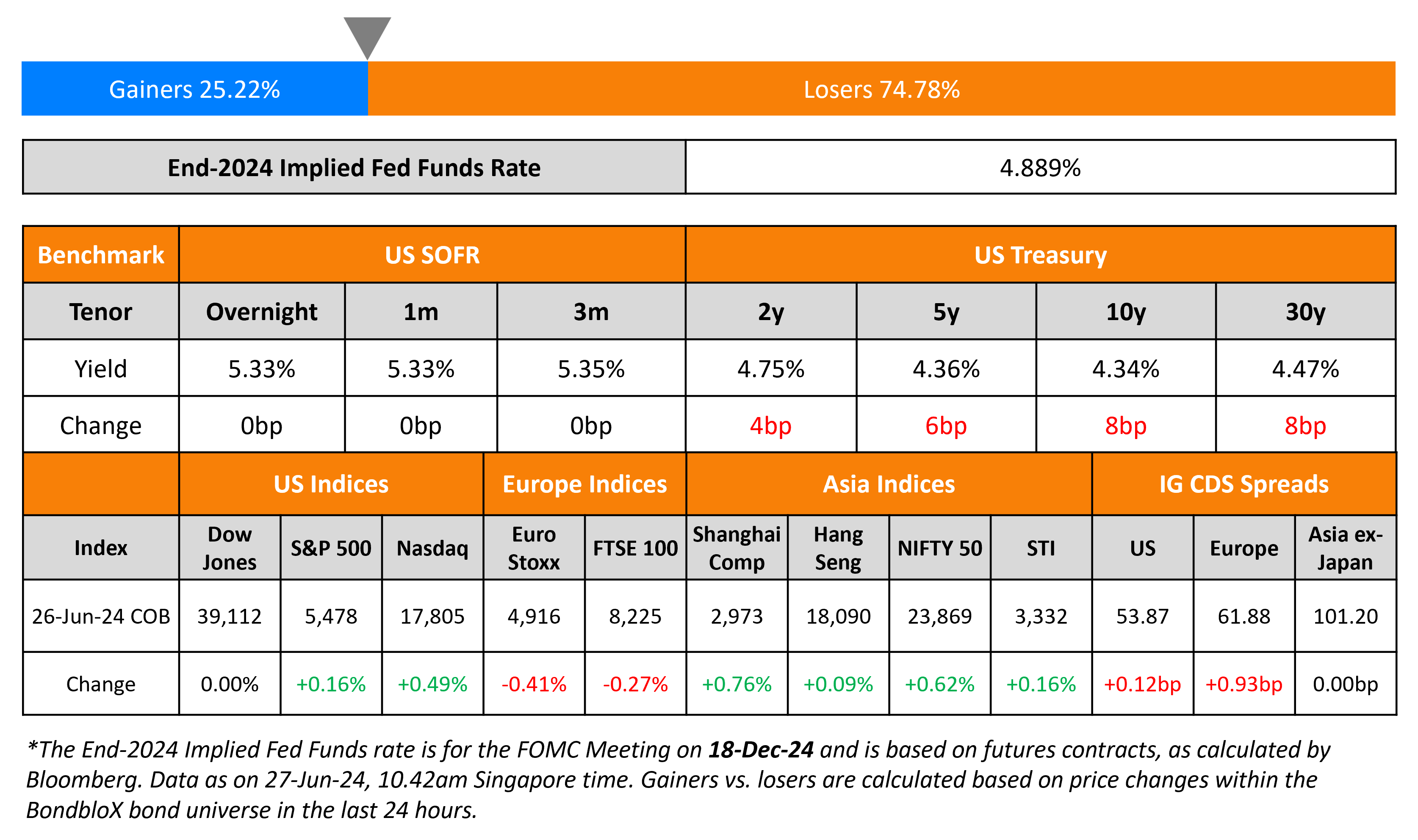

US Treasury yields jumped higher across the curve by 6-8bp. While there was no major economic data release, markets observed that the Japanese Yen weakened past the 160-mark. This is considered to be a threshold where analysts expect the BOJ to step-in and intervene, to support the currency by selling dollars, that might also include US Treasury holdings. This is particularly notable after the BOJ’s $60bn intervention in the forex market in late-April, to support the currency when it breached the same level. Besides, a Japanese official earlier this week, said that they would respond to any excessive moves in currency markets. Separately, the US Treasury’s auction of 5Y notes saw solid demand at a yield of 4.331%, stopping through by 0.4bp. The bid-to-cover ratio was at 2.35x, higher than the previous auction’s 2.30x and indirect bidders took up 68.9% of the notes vs. 65% previously. Looking at equity markets, S&P and Nasdaq were up 0.2% and 0.5%, respectively. US IG spreads were 0.1bp wider while HY CDS spreads widened by 0.7bp.

European equity indices ended lower. In credit markets, the iTraxx Main and Crossover spreads were wider by 0.9bp and 2.4bp respectively. Asian equity indices have opened weaker this morning. Asia ex-Japan CDS spreads were flat. APAC corporates and sovereigns have issued a combined $14bn of bonds this week, marking its busiest week this year. Bloomberg notes that the region’s dollar bond issuance have hit a nine-month high this week, with more deals expected to be priced by Friday.

New Bond Issues

- SoftBank $ 5Y/7Y at 7/7.25% area, € 4.5Y/8Y at 5.5/5.875% area

- Swire Pacific $ 5Y at T+120bp area

- Korea Gas $ 5Y at T+105bp area

- Mizuho $ 6NC5/11NC10 at T+135/155bp area

- Nomura $ 3Y/3Y FRN/10Y at T+135bp/SOFR Equiv./T+180bp area

.png)

Cathay Life Insurance raised $600mn via a 10Y Tier 2 bond at a yield of 5.988%, 35bp inside initial guidance of T+205bp area. The subordinated notes are rated BBB+/BBB+ (S&P/Fitch), issued by Cathaylife Singapore Pte, and guaranteed by Cathay Life Insurance Co Ltd. Proceeds will be used to supplement and strengthen the guarantor’s financial structure and capital base, and to improve its capital adequacy ratio.

Vakifbank raised $700mn via a 10.25NC5.25 Tier 2 bond at a yield of 9.00%, ~11.25bp inside initial guidance of 9.25-9.375% area. The subordinated notes are rated CCC+ (Fitch), and received orders of over $1.45bn, 2.1x issue size. Proceeds will be used for general corporate purposes.

China Huaneng raised $500mn via a PerpNC3 bond at a yield of 5.3%, 55bp inside initial guidance of 5.85% area. The bonds are rated A3. The notes have a change of control put at 101% and a dividend stopper. A coupon step-up of 300bps will be applicable upon the occurrence of a distribution stopper event, change of control event, breach of covenant or indebtedness default event. There will be a decrease of 300 bps if the relevant event is remedied. Proceeds will be used to repay overseas debt.

Macquarie raised $1.6bn via a two-tranche deal. It raised $750mn via a 3Y bond at a yield of 5.272%, 20bp inside initial guidance of T+95bp area. It also raised $850mn via a 3Y FRN at SOFR+92bp vs. initial guidance of SOFR equivalent area. The senior unsecured bonds are rated Aa2/A+/A+. Proceeds will be used for general corporate purposes.

Bangkok Bank raised $750mn via a 10Y bond at a yield of 5.716%, 25bp inside initial guidance of T+165bp area. The senior unsecured bonds are rated Baa1/BBB+ (Moody’s/S&P). Proceeds will be used for general corporate purposes.

Korea raised $1bn via a 5Y bond at a yield of 4.576%, 1bp inside initial guidance of T+25bp area. The bonds are rated Aa2/AA/AA-. Net proceeds will become part of the Foreign Exchange Stabilization Fund established and managed under Korean Foreign Exchange Transactions Act. This was the nation’s first dollar bond issuance since 2021. The new bonds were priced ~4bp tighter to its existing 3.5% bonds due September 2028.

EDO raised $750mn via a 7Y sukuk at a yield of 5.662%, 35bp inside initial guidance of T+170bp area. The notes are rated BB+/BB+, and are guaranteed by Energy Development Oman SAOC. The bonds have a clean-up call (Term of the Day, explained below) at 75%.

Allianz raised €600mn via a 5Y bond at a yield of 3.363%, 25bp inside initial guidance of MS+80bp area. The senior unsecured bonds are rated Aa2/AA. Allianz Finance II BV is the issuer, and proceeds will be used for general corporate purposes.

New Bonds Pipeline

- NongHyup Bank hires for $ 3Y/5Y bond

- Ho Bee Land hires for S$ 5Y Green bond

Rating Changes

- Fitch Downgrades Maldives’ Long-Term IDR to ‘CCC+’

- Moody’s Ratings downgrades Intrum’s Corporate Family Rating to Caa1 and the senior unsecured rating to Caa2; outlook negative

- Fitch Downgrades Rockies Express’ IDR to ‘BB’ Post Tallgrass Buy-In; Outlook Negative

Term of the Day

Clean-up Call

A clean-up call refers to a call provision, whereby once a stated percentage of a security is retired, the issuer is obliged to call the remainder of the tranche. While clean-up calls are generally more commonly observed in mortgage-backed securities (MBS), they may also be present as a feature in some bonds. This is different from a normal call option in a bond where the issuer has an option to redeem their bond fully during the specified call date./period.

Talking Heads

On Treasuries Sliding as Weak Yen Offers Reason to Shun Bonds

George Catrambone, head of fixed income at DWS Americas

“The market is taking a pause given the uncertain political backdrop emerging both domestically and abroad… re-inflation surprises in Canada and Australia don’t help”

On Need To Be Ready to Handle Any Political Risks – ECB’s Panetta

“Political and geopolitical risks remain high, and call for awareness, flexibility and state-contingent action plans… (political turnover) can trigger capital outflows and currency depreciations, creating upward price pressures. But it could also shake confidence and weaken demand… should be prepared to deal with the consequences of such shocks”

On Seeing Bets for Two More Cuts in 2024 as Reasonable – ECB’s Olli Rehn

“If you look at market data, it implies that there would be two more rate cuts so that we would end up at 3.25% by the end of this year”

Top Gainers & Losers- 27-June-24*

.png)

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.