This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

US Treasuries March Upwards; PBOC Cuts 1-Year Prime Loan Rate

August 21, 2023

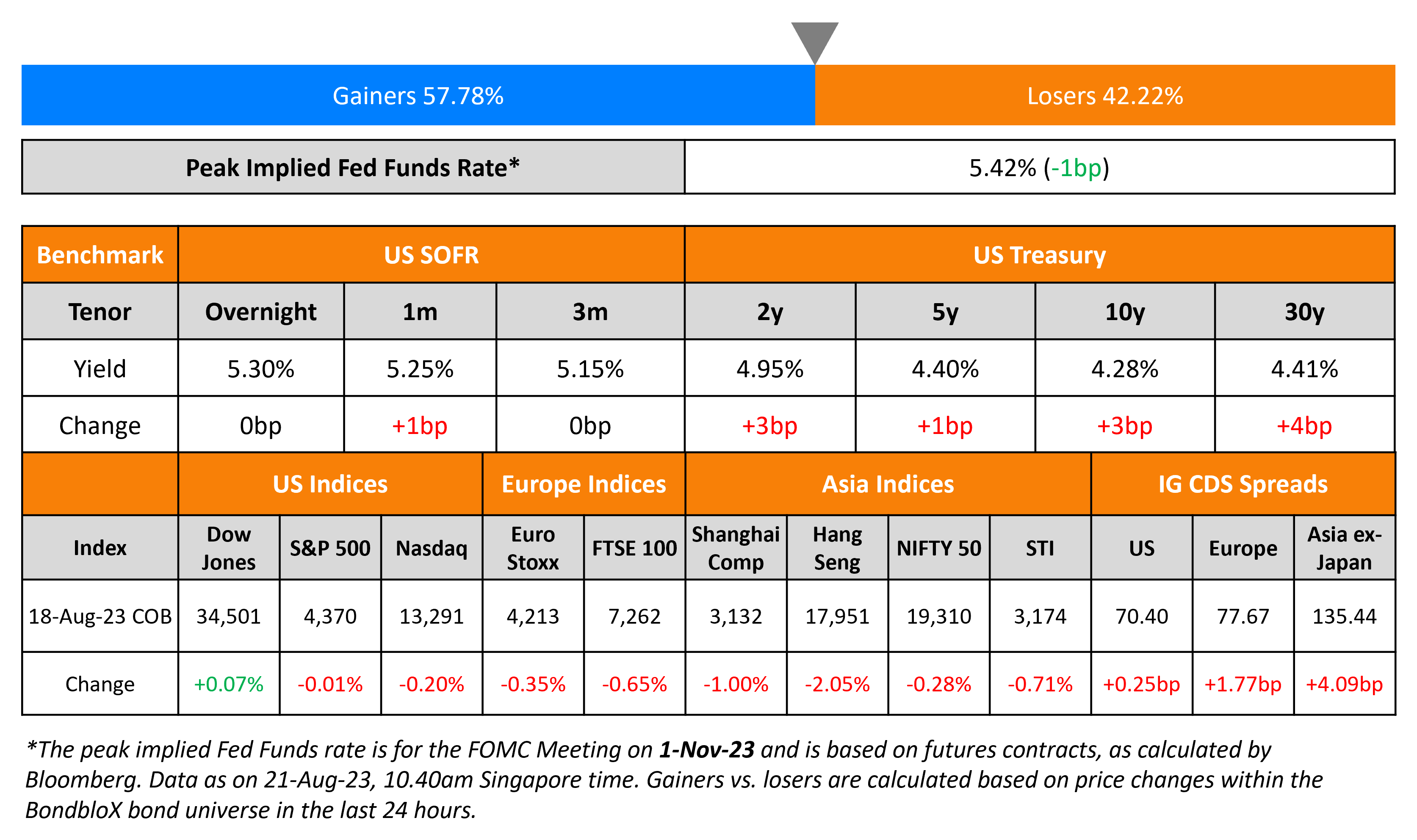

US Treasury yields continued their climb after a brief pause. The 2Y and 10Y rose by 3bp each to 4.95% and 4.28% respectively. The 30Y continued to hover around 4.4%, the highest level since 2011. US IG credit spreads were wider by ~0.3bp while HY CDS spreads remained flat. The S&P closed flat while Nasdaq closed lower by ~0.2%.

European equity markets traded lower. In credit markets, European main CDS spreads were 1.8bp wider and Crossover CDS widened 4.5bp. Asia ex-Japan CDS spreads widened further by 4bp to 135.4bp on the back of concerns regarding China. Asian equity markets have opened broadly weaker this morning. The PBOC cut its 1-year prime loan rate by 10bp (vs. estimates of a 15bp cut) to 3.45% and left the 5-year rate unchanged at 4.2% (vs. estimates of a 15bp cut). Further, Chinese financial regulators called for coordinating financial support to resolve local debt risks and adjust policy for real estate loans, at a video conference on Friday.

New Bond Issues

Rating Changes

- Rumo S.A. Outlook Revised To Positive, Mirroring Action On Parent Cosan; ‘BB-‘ Rating Affirmed

-

Fitch Downgrades and Withdraws HSBC Bank Oman’s Ratings on Merger Completion

Term of the Day

Restricted Group/ Subsidiaries

Restricted Group or restricted subsidiaries refer to a parent or holding company’s subsidiaries that are tied to the debt covenants of the parent issuer. Restricted groups may have covenants that restrict cash upstreaming to shareholders, additional indebtedness, liens, dividend payments, making new investments etc. Unrestricted subsidiaries on the other hand are not bound by the parent or holdco’s bond covenants and are thus not required to support repayment of the debt securities.

Talking Heads

On Buying Bonds and Yield Protection

Kathy Jones, chief fixed income strategist at Schwab Center for Financial Research

“We have been suggesting investors move out in duration and buy intermediate-term bonds, in the five- to 10-year area. Target the average duration for a laddered bond portfolio to around six years. Those can generate a 5%-5.5% rate depending on how much credit risk you want to take. That’s been the highest yield you could get in about a decade and the highest real rates we’ve seen in a very long time.”

On Upcoming Treasury Auction before Jackson Hole

George Catrambone, Head of fixed income at DWS Americas

“No one wants to step in front of the issuance freight train, especially in the long end at the moment. There aren’t great reasons to front-run a hawkish Fed, additional supply and very resilient US economic data prints.”

On Expectations Of ‘Hard Landing’ For US Economy

Jamie Patton, co-head of global rates at TCW Group

“If officials think interest-rate hikes “are going to impact the economy sooner – and we think that’s not true — that means the Fed is very likely to keep rates too high for too long. That would raise the risk of a larger-than-expected decline in growth, and eventually, inflation. That supports our long-duration position.”

On Tackling Local Government Debt Woes and Property Crises

Statement by Central Bank of China

“Major financial institutions should act proactively and disburse more loans as big state-owned banks continue to act as pillars. They have to focus on keeping the growth in loans steady, give appropriate guidance to lessen fluctuations in lending and increase the stability of financial support for the real economy.”

Top Gainers & Losers- 21-August-23*

Other News

Total Play Bonds Under Pressure Due To Concerns Over Financing Strategy

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.