This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Treasury Yields Drop by 20bp on Softer Inflation

November 15, 2023

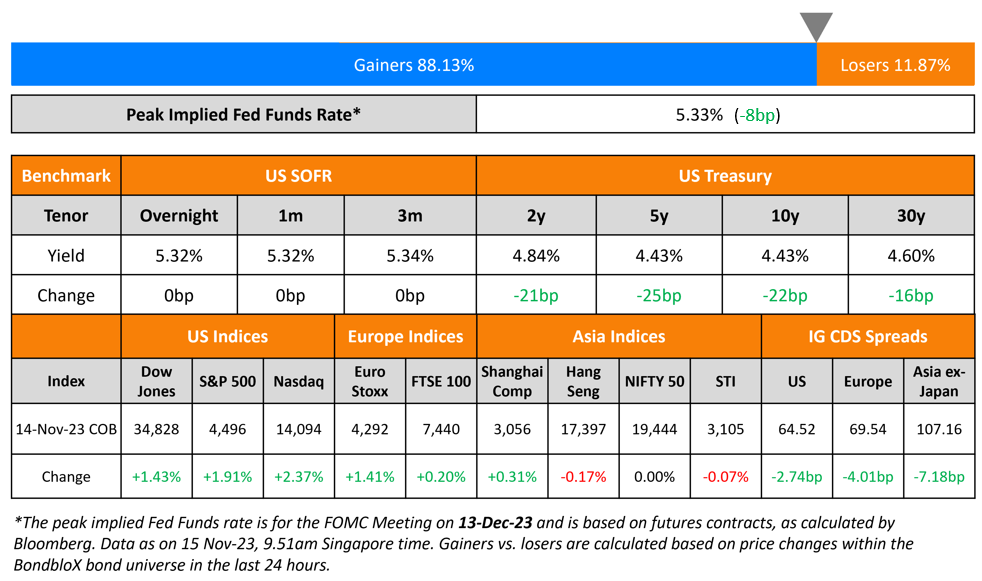

US Treasuries saw a massive rally across the curve, after a softer than expected inflation report. Treasury yields fell by over 20bp across the curve on Tuesday. US Headline CPI for October 2023 rose by 3.2%, lower than expectations of 3.3% and the previous month’s 3.7%. Core CPI came at 4.0%, lower than expectations and the previous month’s 4.1% print. Markets have priced out any further hikes by the Fed and more analysts now expect the Fed to cut rates in the second half of 2024. The Peak Fed Funds Rate fell 8bp. US credit markets saw IG CDS spreads tightening by 2.7bp while HY spreads tightened by 16.5bp. S&P rose and Nasdaq rallied 1.9% and 2.4% respectively.

European equity markets closed higher too. In credit markets, European main CDS spreads were tighter by 4bp and crossover spreads tightened by 16bp. Asian equity markets have opened in the green today and Asia ex-Japan IG CDS spreads were tighter by 7.2bp. Separately, China has planned to provide at least RMB 1bn ($137bn) of low-cost financing to its urban village renovation and affordable housing programs via banks, with an effort to see the money trickle down to households for home purchases.

We are excited to share that our company has raised a $6mn in Series B funding. The round saw new investor Beacon VC, the corporate venture arm of Thailand’s Kasikornbank, join existing shareholders MassMutual Ventures and Citigroup who also participated in the round. Click on the banner below for details.

New Bond Issues

- Barclays $ Perpetual bond at 10.5% area

- ABC London $300mn 3Y FRN at SOFR+105bp area

Jinan Shuntong raised $210mn via a short 1Y bond at a yield of 6.7%, 40bp inside initial guidance of 7.1% area. The senior unsecured bonds have expected ratings of A- (Fitch), in line with its guarantor, Jinan Rail Transport’s ratings. Proceeds will be used to refinance existing offshore indebtedness.

Rating Changes

- Fitch Downgrades Liquid Telecom to ‘B’; Outlook Remains Negative

- Tata Motors, TML Holdings Upgraded To ‘BB+’ On Strong Free Operating Cash Flow, Deleveraging Prospects; Outlook Positive

- Jaguar Land Rover Upgraded To ‘BB’ On Stronger Free Cash Flow And Improving Profitability; Outlook Positive

Term of the Day

Term Premium

The term premium is the yield premium that investors expect to receive in order to be compensated for lending for longer periods as compared to shorter periods. The term structure of interest rates in a normal scenario is upward sloping, with longer term yields higher than short term yields. However, research by the BIS and other institutions note that the term premium can also be affected by other factors, thereby reducing the yield compensation – for example flight to quality towards long-end treasuries, liquidity considerations etc.

Talking Heads

On Investors Dumping Cash to Chase Bonds – BofA Survey

Investor playbook for 2024 is soft landing, lower rates…the “big change” was not the macro outlook, but expectations that inflation and yields will move lower in 2024.

On Sri Lanka’s Dollar Bond Rally May Be Approaching End

Carlos de Sousa, PM at Vontobel Asset Management

“Estimated recovery values are in line with market prices, so I don’t see sufficient potential upside from here”

Patrick Curran, senior economist at Tellimer Markets

“The government’s rejection of the proposal shows that there is a risk of negotiations dragging out or leading to less creditor-friendly terms”

Johnny Chen, fund manager at William Blair Investment Management

“Sri Lanka bonds are still relatively attractive because they are in an IMF program and restructuring talks are ongoing”

On Fed seen pivoting to interest rate cuts in May

Brian Jacobsen, chief economist at Annex Wealth Management

“You can say goodbye to the rate hiking era”

Nationwide Chief Economist Kathy Bostjancic

“The Fed for now will maintain its tightening bias, erring on the side of caution”

On Calling for Bond Rally in 2024 – Pimco

Bonds have rarely been as attractive as they appear today” relative to stocks… History suggests equities likely won’t stay this expensive relative to bonds… an optimal time to consider overweighting fixed income in asset-allocation portfolios.

Top Gainers & Losers- 15-November-23*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.