This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

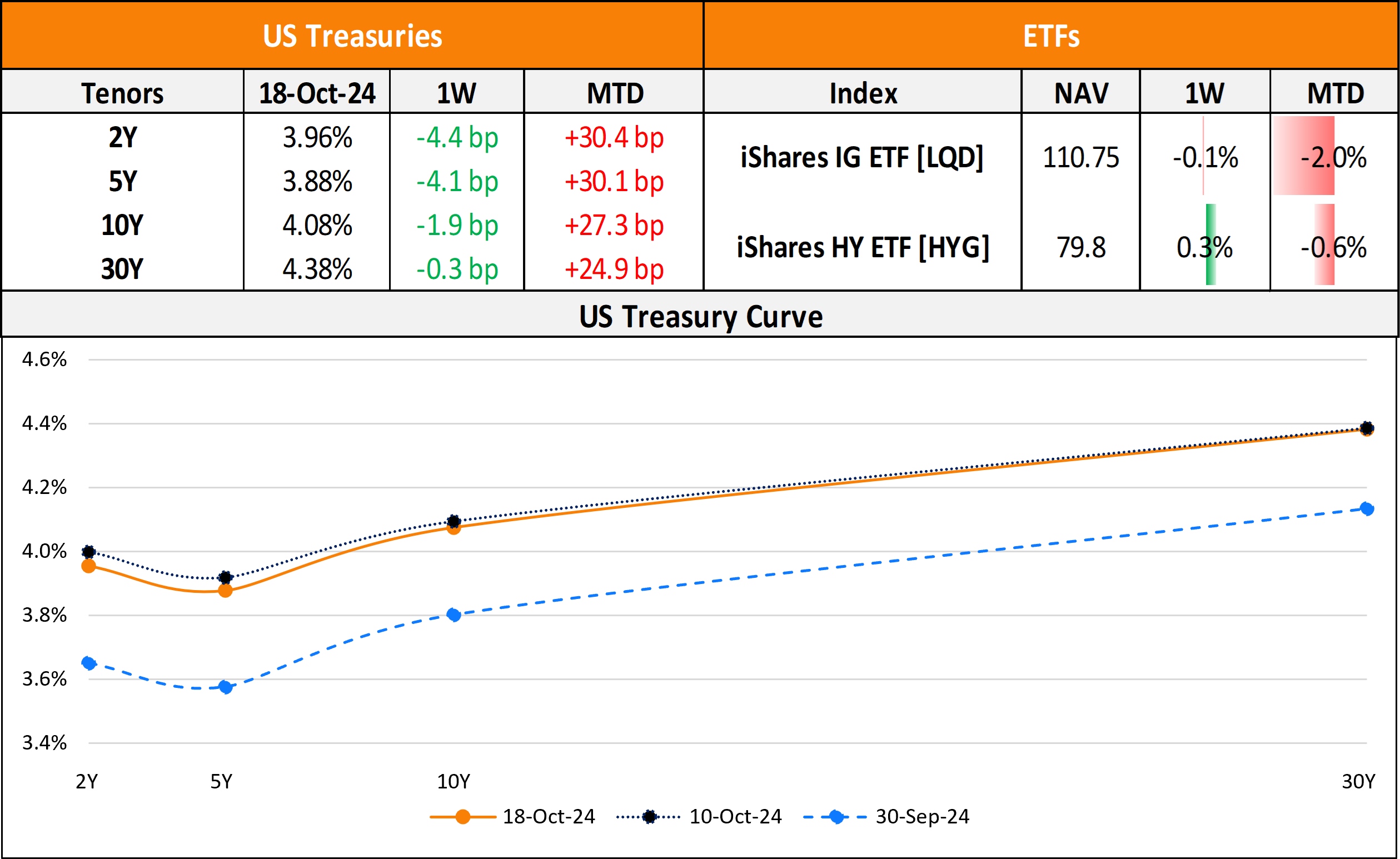

The Week That Was (14 – 20 Oct, 2024)

October 21, 2024

US primary market issuances jumped higher last week to $28.6bn vs. only $12.3bn seen in the week prior to it. IG issuers took up $25.3bn of the total, led by JPMorgan’s $8bn four-trancher and Morgan Stanley’s $5.75bn three-part deal. Last week saw $3.3bn in HY issuances from the region, led by Jane Street’s $1.15bn issuance and NRG Energy’s $1.88mn two-part deal. In North America, there were a total of 34 upgrades and 47 downgrades across the three major rating agencies last week. US IG funds saw $2.17bn of inflows last week, adding to the $1.83bn of inflows during the week before that. HY funds witnessed a net $664mn in inflows during the same period, reversing the $146mn of inflows in the week prior to it.

EU Corporate G3 issuances dropped last week to $15.4bn vs. $24.5bn in the prior week. Informa AG’s €1.75bn two-part deal and Argenta Spearbank’s €1.5bn issuance led the tables. The region saw 40 upgrades and 47 downgrades, across the three major rating agencies. The GCC dollar primary bond market saw no new deals last week vs. $1.3bn in deals seen in the prior week. In the Middle East/Africa region, there were 9 upgrades and 10 downgrades across the major rating agencies. LatAm saw $2.9bn in issuances last week vs. $3.2bn in the week prior to it. Issuance volumes were led by Ecopetrol’s $1.75bn deal and ABRA Global’s $510mn deals each. The South American region saw 3 upgrades and no downgrades across the rating agencies.

G3 issuance volumes from APAC ex-Japan rose to $5.3bn vs. $3.9bn seen in the previous week. CSI Ltd’s $1bn two-trancher and Export Finance & Insurance’s $750mn deals led the table, followed by $500mn deals from Korea Land & Housing and Wuhan Metro. In the APAC region, there were 2 upgrades and 11 downgrades, across the three rating agencies last week.

Go back to Latest bond Market News

Related Posts:

1, 2, 3, 4th Fed Hike!

June 14, 2017

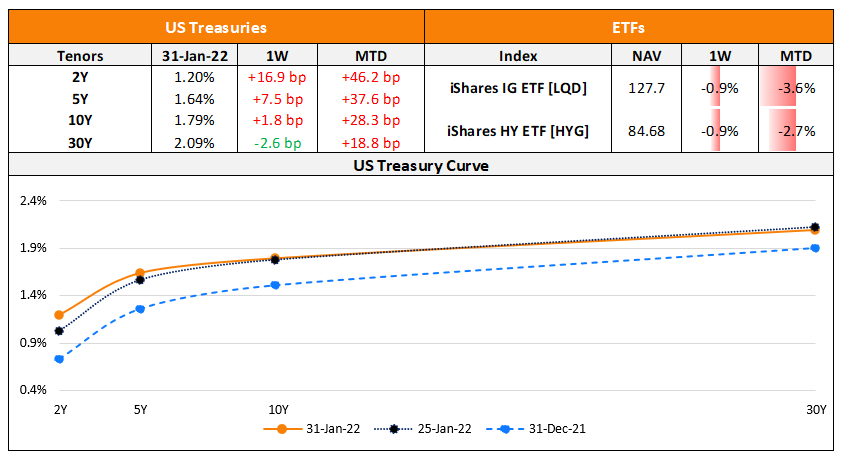

The Week That Was (24 – 30 Jan, 2022)

January 31, 2022

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.