We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

The Week That Was (1 – 7 July, 2024)

July 8, 2024

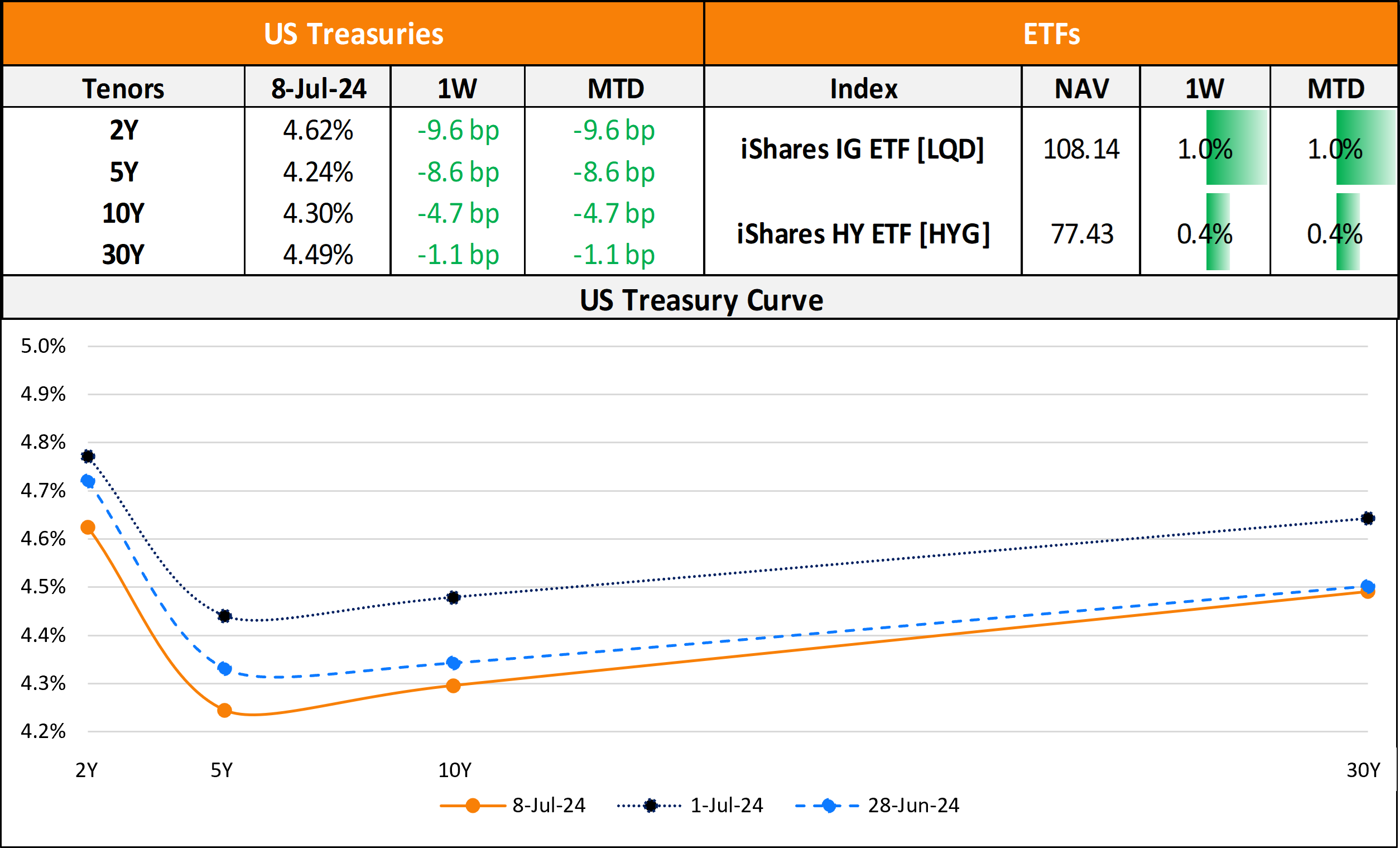

US primary market saw no issuances last week after a mild week of issuances prior to it that stood at only $8.6bn. After seeing a flurry of deals in mid-June, volumes have dropped considerably over the past two weeks. The week was also impacted by the US Independence Day holidays, besides elections in two other major markets like UK and France. US IG funds saw inflows of $2.4bn for the week ending July 3, adding to the $389.2mn inflows seen in the prior week. HY funds saw $289mn in outflows, adding to $225mn outflows seen a week before this.

EU Corporate G3 issuances recorded a sharp drop in new deals last week to $12.8bn vs. $28.9bn seen in the week prior to it. Deutsche Bank’s €2.25bn deal led the tables, followed by NatWest’s $1.5bn two-tranche deal. The region saw 54 upgrades and 15 downgrades each across the three major rating agencies. The GCC dollar primary bond market saw $600mn in new deals last week compared to $3.3bn in new issuances in the week prior, led by Warba’s $500mn sukuk. In the Middle East/Africa region, there were no upgrades and downgrades across the major rating agencies. LatAm saw no new deals after $4.3bn in new deals seen during the week prior to it. The South American region saw no upgrades and 1 downgrade across the rating agencies.

G3 issuance volumes from APAC ex-Japan stood at $2.6bn vs. $10.5bn in the week prior to it. Taizou Urban Construction’s $500mn deal led the table, followed by SMRC Automotive’s $350mn deal, CMB’s $400mn deal and China Citic’s $300mn issuance. In the APAC region, there were 6 upgrades and 5 downgrades across the three rating agencies last week.

.png)

Go back to Latest bond Market News

Related Posts:

1, 2, 3, 4th Fed Hike!

June 14, 2017

The Week That Was (24 – 30 Jan, 2022)

January 31, 2022

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.