We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Syngenta Downgraded to BBB by Fitch

July 16, 2024

Syngenta AG and its senior unsecured notes were downgraded by a notch to BBB from BBB+ by Fitch. The downgrade reflects the weakening credit profile of the company due to increase in net leverage and weaker market dynamics. Syngenta’s gross debt increased to $14.1bn in 2023 from $11.6bn in 2022 as a result of lower sales, higher inventory costs and idle capacity expenses. Its adjusted EBITDA net leverage also rose to 5x in 2023 from 3.5x in 2022, with higher interest costs and working capital outflows contributing to negative free cash flows. According to Fitch, Syngenta has a low to medium incentive of support from Chemchina, its parent and Sinochem, its ultimate parent.

Syngenta’s bonds traded stable with its 4.892% 2025s at 99.3, yielding 5.79%.

Go back to Latest bond Market News

Related Posts:

Pampa Energia Upgraded to B-

June 25, 2021

Bed Bath’s Bonds Downgraded to CCC- by S&P

September 2, 2022

US PMI Data Comes in Stronger Than Expected

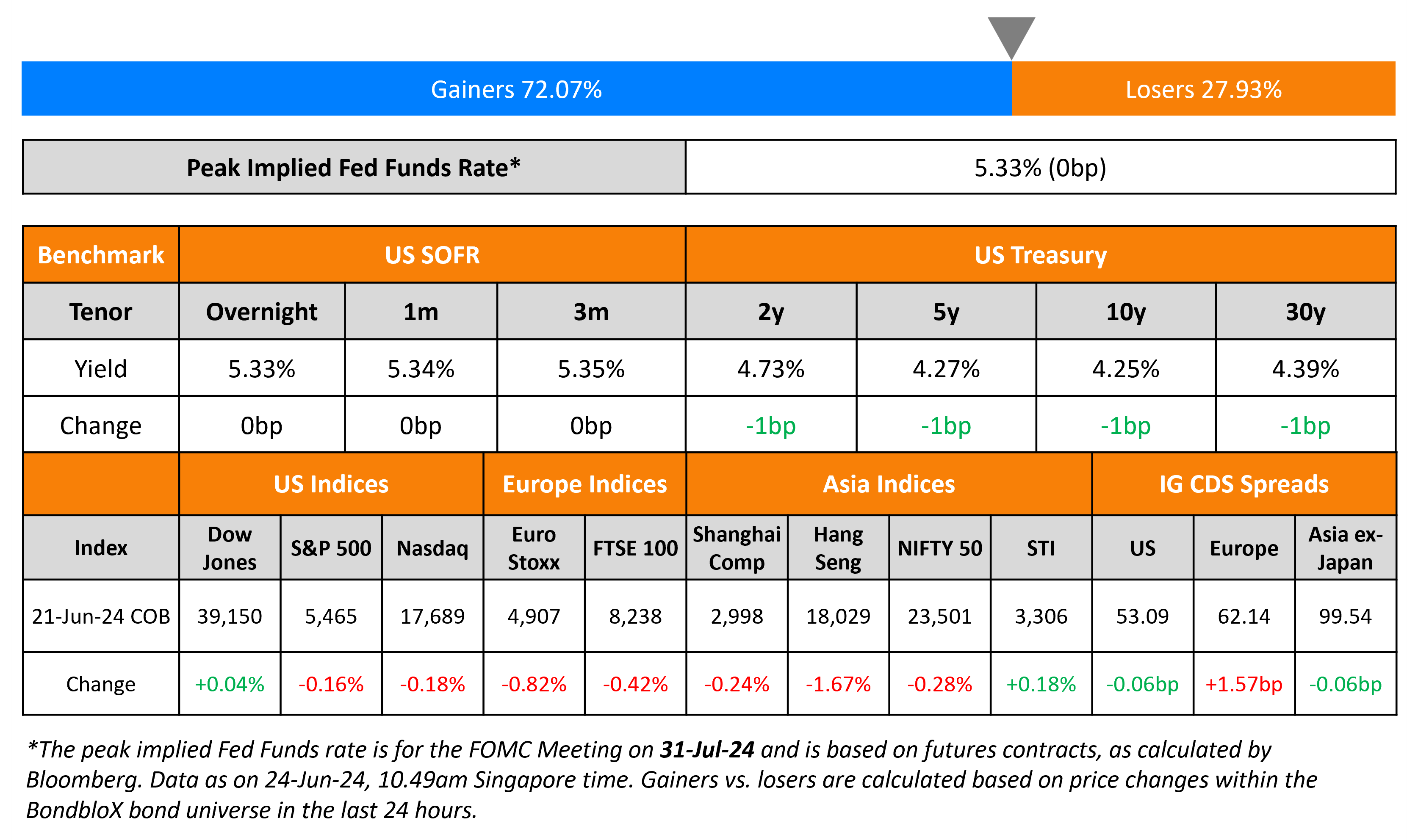

June 24, 2024

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.