This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Macro; Rating Changes; New Bond Issues; Talking Heads; Top Gainers & Losers

April 29, 2021

S&P closed 0.1% lower and Nasdaq 0.3% lower. The FOMC maintained its dovish stance with Chairman Jerome Powell saying that it was “not time yet” and that the Fed were a long way from reducing support to the economy. US 10Y Treasury yields dipped on the back of the dovish Fed before ending almost unchanged. European indices were higher with bank stocks benefitting after their results – the FTSE and DAX closed up ~0.3% each and CAC up 0.5%. US IG CDS spreads were 0.7bp tighter and HY tightened 3.6bp. EU main CDS spreads were flat and crossover spreads widened 0.5bp. Asian equity markets are trading higher by 0.3% today and Asia ex-Japan CDS spreads were 1.3bp tighter.

New Bond Issues

- Nanjing Jiangbei New Area Industrial Investment 364-day $ notes at 3.1% area; books over $750mn

- XiAn Qujiang Cultural Industry Investment $ 3Y at 5.5%

- Guangzhou Finance Holdings Group $ 3Y at 2.75% area

Beijing Enterprise raised $700mn via a two-trancher. It raised $300mn via a 5Y bond at a yield of 2.107%, 50bp inside initial guidance of T+175bp. It also raised $400mn via a 10Y bond at a yield of 3.279%, 45bp inside initial guidance of T+210bp area. The bonds have expected ratings of Baa1/BBB+ and received orders over $4.6bn, ~6.5x issue size. Asia took 97% and EMEA 3%. Asset/fund managers received 29%, banks and financial institutions 68%, and private banks and others 3%. Proceeds will be used for offshore debt refinancing.

BIM Land raised $200mn via its debut dollar bond, a senior green bond at a yield of 7.75%, 12.5bp inside initial guidance of 7.875% area. The bonds have expected ratings of B2/B, and received orders over $625mn, ~3x issue size. Asia bought 58%, EMEA 41% and the rest went to offshore US investors. Fund/asset managers took 92% and private banks 8%. The Vietnamese property developer plans to use the proceeds to fund eligible green projects as well as for working capital and general corporate purposes.

Kookmin Bank raised $500mn via a 5Y Sustainability bond at a yield of 1.406%, 30bp inside initial guidance of T+85bp area. The bonds have expected ratings of Aa3/A+ and received orders over $2.1bn, 4.2x issue size. Asia took 73%, Europe 16% and the US 11%. Asset managers and insurers bought 47%, banks 33%, central banks and sovereigns, supranationals and agencies 19% and others 1%. Proceeds will be used for eligible projects under the Korean bank’s sustainable financing framework.

New Bond Pipeline

- Khazanah Nasional Berhad $ 5Y/10Y Sukuk

- KB Kookmin Card $ Sustainability bond

-

China Water Affairs Group $ green bond

Rating Changes

- Fitch Upgrades Drax’s Senior Secured Rating to ‘BBB-‘; Removes UCO

- Fitch Affirms Walt Disney’s IDR at ‘A-‘; Outlook Revised to Stable

- Fitch Revises Outlook on Mitsui Sumitomo Insurance to Stable; Affirms IFS Rating at ‘A+’

- Volkswagen AG Outlook Revised To Stable From Negative By S&P On Stronger-Than-Expected Free Cash Flow Generation

- ADES International Holdings PLC Outlook Revised To Stable From Negative By S&P On Cash Flow Visibility; ‘B+’ Ratings Affirmed

- Delhi International Airport ‘B-‘ Ratings Affirmed By S&P, Off CreditWatch; Outlook Positive On Improving Cash Flow Prospects

- DTE Energy Center LLC ‘BBB+’ Senior Secured Bonds Rating Affirmed By S&P; Outlook Revised To Positive From Stable

- Caleres Inc. Outlook Revised To Stable From Negative By S&P On Expected Performance Improvement; ‘B+’ Rating Affirmed

Term of the Day

Haircut

Haircut refers to a reduction in value of an asset for the purpose of calculating either margin requirements, level of collateral or salvage value. The haircut is generally stated as a percentage and is the difference between the value of the asset and its reduced value. For example, in a restructuring, if a bond worth $100mn faces a haircut of 20%, then holders would receive only $80mn. In the case of a loan, if the collateral is worth $100mn, a haircut of 30% would imply that a loan of $70mn, giving the lender a cushion in case the market value of the collateral falls. Peking University Founder Group is said to be considering up to a 70% haircut for bondholders as part of a debt restructuring plan.

Talking Heads

Jerome Powell, Federal Reserve Chairman

“The economy is beginning to move ahead with real momentum,” Powell said. “An episode of one-time price increases as the economy re-opens is not the same thing as, and is not likely to lead to, persistently higher year-over-year inflation,” he said. “When the time comes for us to talk about talking about it we’ll do that. But that time is not now,” he said. “We’ve had one great jobs report. It’s not enough. We’re going to act on actual data, not on a forecast, and we’re just going to need to see more data. It’s no more complicated than that.” If inflation were to move “persistently and materially above 2% in a manner that threatened to move longer-term inflation expectations materially above 2% we would use our tools to bring inflation expectations down to mandate consistent levels.”

Carl Tannenbaum, chief economist at Northern Trust

“I took away that not even any preliminary discussion of a change in policy is imminent,” said Tannenbaum. “He gave a spirited defense of the Fed’s view on inflation and employment. They are very happy with the course they are on and not likely to change it soon.”

Jerome Powell, Federal Reserve Chairman

“We’ve had one great jobs report, it’s not enough,” Powell said. “We’re going to act on actual data, not our forecast.” “We’re a long way from our goals,” he added. “We think of bottlenecks as things that in their nature will be resolved as workers and businesses adapt, and we think of them as not calling for a change in monetary policy since they’re temporary and expected to resolve itself,” Powell said. “We know the base effects will disappear in a few months.” “If we see inflation moving materially above 2 per cent in a persistent way that risks inflation expectations drifting up, then we will use our tools to guide inflation and expectations back down to 2 per cent. No one should doubt that we will do that,” he said.

In comments by the Federal Open Market Committee members

“Amid progress on vaccinations and strong policy support, indicators of economic activity and employment have strengthened. The sectors most adversely affected by the pandemic remain weak but have shown improvement,” the committee said.

Tom di Galoma, a managing director at Seaport Global Holdings

Powell “made it pretty clear that they are a fairly long way away from tapering,” said di Galoma. “I think the Fed is still quite unsure of how the economy is going to be six months from here.” “With all the money that is being spent … it puts the Fed in a very difficult position to taper,” di Galoma said.

Patrick Leary, chief market strategist and senior trader at Incapital

“It’s just hard to know what transitory is,” said Leary. “I think the market is going to get impatient about the level of inflation and how long it might last, and it might be perceived by the market that that inflation is not transitory, causing a little bit of a revolt, so to speak, in the bond market,” Leary added.

In a note by Nikolaos Panigirtzoglou and team, JPMorgan Chase & Co. strategists

“The big improvement in funding ratios implies a high incentive” for “U.S. private defined benefit pension plans to lock in the recent gains in their funding position by accelerating their de-risking going forward.” That means “accelerating their buying of long-dated bonds and selling of equities.” “So public pension funds have less incentive to de-risk in general,” Panigirtzoglou wrote. “But they do face a problem. Their equity allocation is already very high and their bond allocation stands at a record low of 20%. So, from an asset/liability mismatch point of view they are under some pressure to buy bonds.”

Zorast Wadia, a principal at Milliman

“The main reason for the overall shift from equities into fixed income has had to do with the change in pension regulations,” said Wadia. “And as these pensions’ funding status have improved they have continued to shed equity risk — getting more and more into fixed income.”

Adam Levine, investment director of Aberdeen Standard Investment’s client solutions group

What corporate pension plans “are looking for is to be well funded, not necessarily to get strong returns,” said Levine. “It is possible that as rates rise, corporate pensions move enough to the fixed income that to some degree it counters the rise in rates. You can certainly make that case if the moves are big enough and the industry is big enough.”

On record defaults clouding India’s resilient bonds and equities

Sunil Subramaniam, managing director of Sundaram Asset Management Co

“One can’t expect there will be good news on the economy, good news on earnings and stock prices will go up,” said Subramaniam. “It is undoubtedly going to be a volatile period for the market.”

Vikas Goel, managing director and chief executive officer at PNB Gilts Ltd

“Markets are getting cautious on the credit side as economic growth is seen slowing down, raising concerns distressed debt may rise,” said Goel.

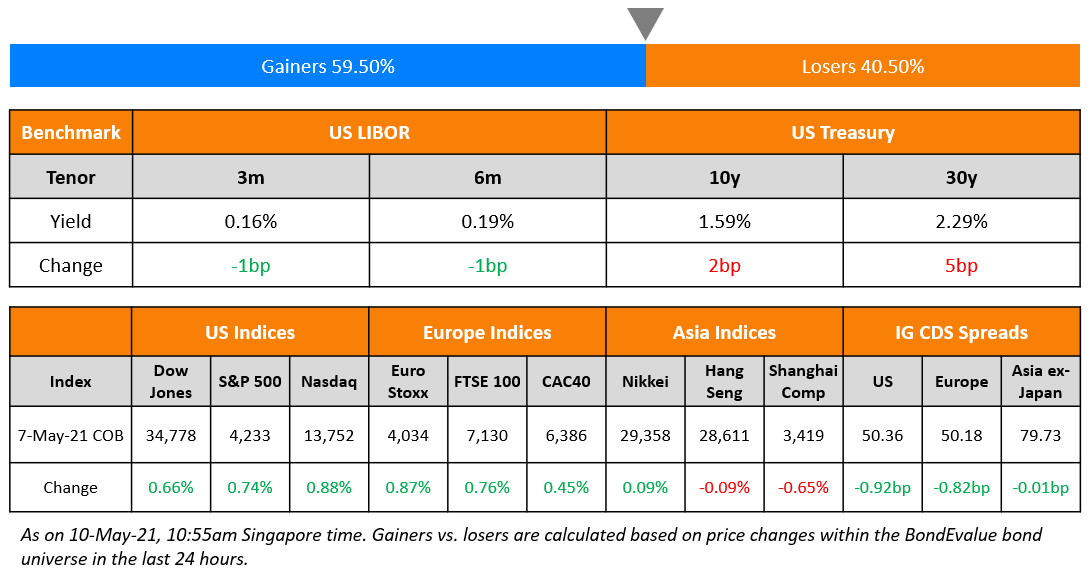

Top Gainers & Losers – 29-Apr-21*

‘

‘Other Stories

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.