We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Westpac NZ, KHFC, Mizuho Launch $ Bonds

February 20, 2024

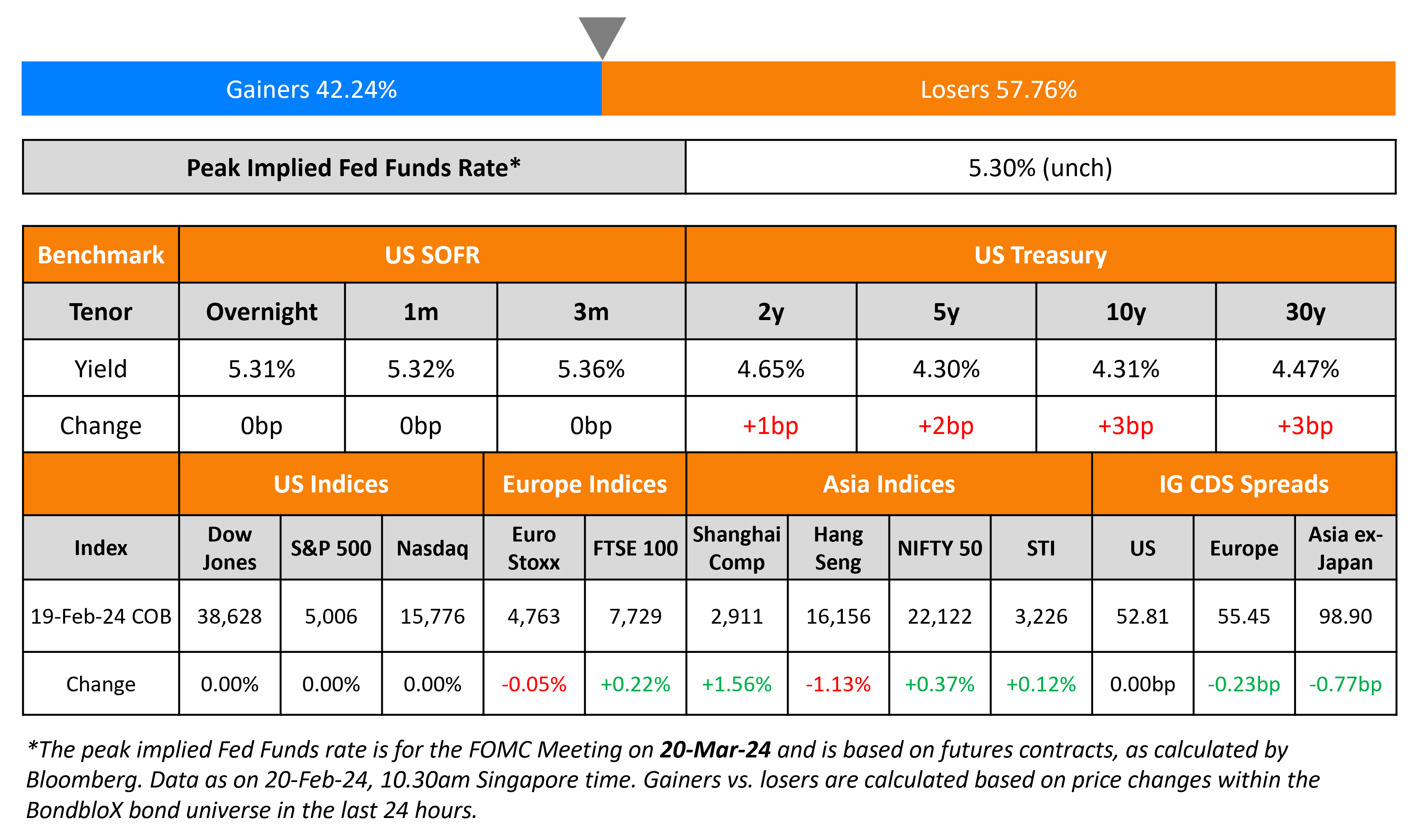

US Treasury yields are marginally higher by 2-3bp today. Equity and credit markets were closed yesterday due to Presidents’ Day.

European equity markets ended mixed. Credit markets in the region saw the European main CDS spreads tighten by 0.2bp while crossover spreads widened by 1.4bp. Asian equity markets have opened weaker today. Asia ex-Japan IG CDS spreads tightened by 0.8bp. In China, authorities lowered the five-year loan prime rate to 3.95% in February from 4.20% in January while maintaining the one-year rate at 3.45%.

New Bond Issues

- Westpac New Zealand $ 3Y/5Y at T+100/120bp area

- Korea Housing Finance Corp $ 3.5Y Social at T+90bp area

- Mizuho $ 6.25NC5.25/11.25NC10.25 at T+145/165bp area

SGX raised S$300mn via a 3Y bond at a yield of 3.45%, 15bp inside initial guidance of 3.6% area. The senior unsecured notes are rated Aa2 (Moody’s). The notes are issued under its overall S$1.5bn multicurrency debt issuance program. Proceeds will be used to refinance existing debt and for general corporate purposes. The bonds can be called at par any time on or after 26 January 2027 and have a make-whole call at the prevailing SGD SORA-OIS+0.10%.

Credit Agricole raised €1.25bn via a 12Y bond at a yield of 4.132%, 35bp inside initial guidance of MS+170bp area. The senior non-preferred bond was rated A3/A-/A+, and received orders of over €6bn, 4.8x issue size.

New Bond Pipeline

- Del Monte Philippines hires for $ Perp

- Daewoo Engineering & Construction hires for S$ bond

- Greenko Mauritius hires for $ bond

Rating Changes

- Moody’s downgrades Arabian Centres’ ratings to Ba3, stable outlook

- Moody’s downgrades Alicorp’s rating to Ba1; stable outlook

- Moody’s changes the outlook on ArcelorMittal to positive from stable; affirms its Baa3 ratings

- Moody’s changes Afreximbank’s outlook to negative from stable, Baa1 rating affirmed

Term of the Day

Make Whole Call

A Make Whole Call (MWC) is a type of call option on a bond that gives the issuer the right to redeem a bond before its maturity date by compensating (making whole) bondholders for future coupon payments. MWC provisions were introduced in the 1990s and are rarely exercised by issuers. If exercised, the issuer has to pay a lump sum amount to the bondholders that represent the net present value of future foregone coupon payments, typically stated as a formula in the bond prospectus.

MWCs are different from traditional call options in that investors are compensated for foregoing future coupon payments. With traditional call options, the issuer can exercise the call option at the predefined call price without having to pay bondholders for foregoing future coupons. This makes MWCs beneficial to bondholders as compared to traditional call options and are typically expensive for the issuer to exercise.

Talking Heads

On $6tn Cash Wall Holding Firm as Fed Delays Cuts

Peter Crane, president of Crane Data

“The year of cash wasn’t a flash in the pan… overall resensitization to interest rates is still spreading and even a lot of money hasn’t moved or looked at it yet”

Joseph Abate, Barclays strategist

“Relative to expected earnings, cash is relatively attractive”

Jerome Schneider, head of short-term portfolio management at PIMCO

“Once we get to a point where the Fed is already cutting rates, it might be a little late for investors to continue to perform at a higher income”

On Shareholder Returns at Peak for European Banks – JPMorgan

“EPS revisions of European banks have just recently entered negative territory”… underweight on banks is “one of the sector calls where we face the most pushback from investors”… given bond yields have likely peaked, “banks should be peaking, as well”

On Investors Wary of Crowded India Trade After Run-Up

Sean Taylor, chief CIO at Matthews Asia

“India is the best longer-term story, but we are taking a bit of profit… will be trimming more of India into Fed cuts on a relative basis because I need to put more capital into places like Korea and Taiwan.”

Vicki Chi, Hong Kong-based PM at Robeco

“Underweighting the country because we’re value investors and we struggle in this market”

Top Gainers & Losers- 20-February-24*

Other News

Capital One Enters $35bn Stock Deal to Buy Discover Financial

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.