This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

US Treasuries Trade Stable with Mixed Data

July 26, 2024

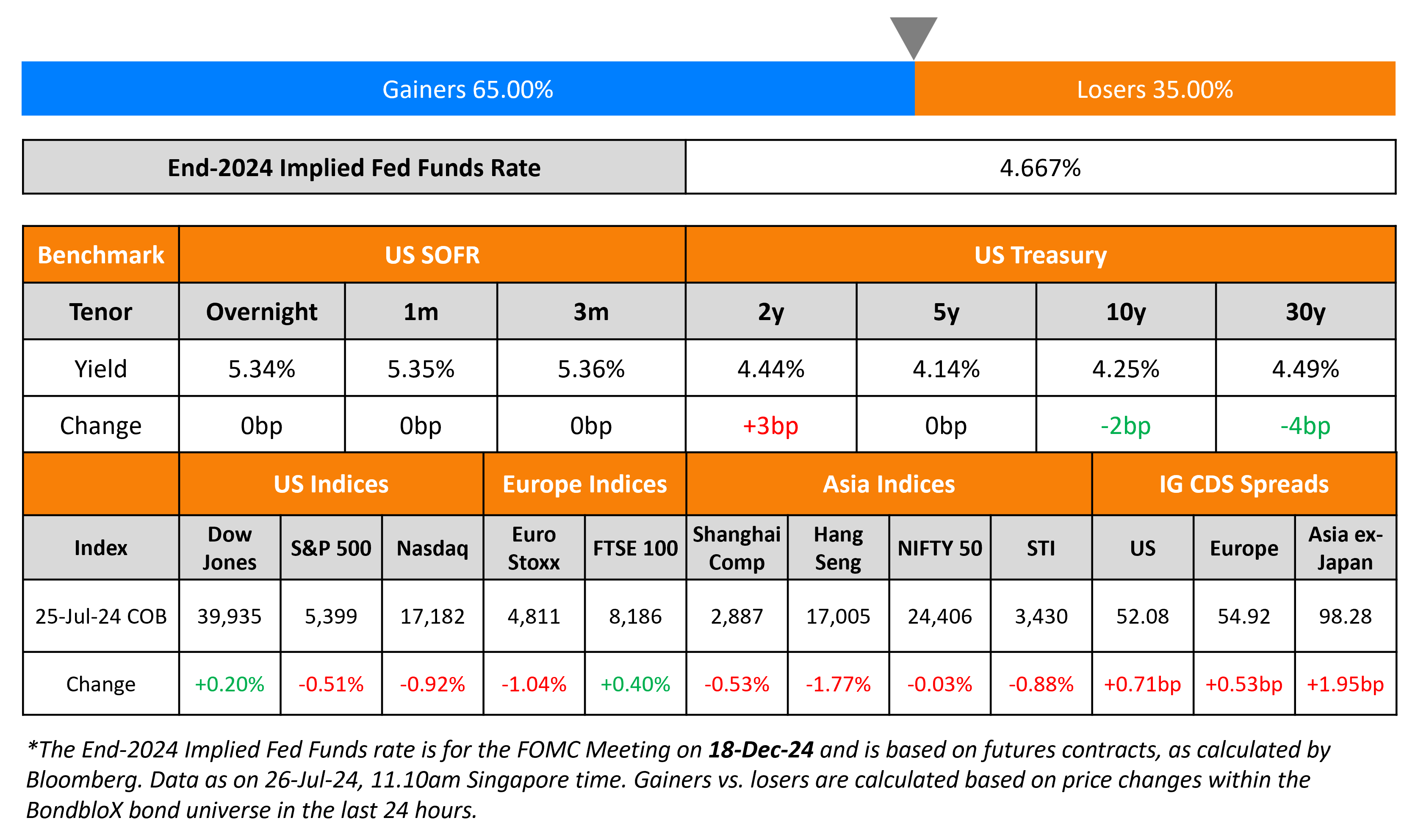

The US Treasury curve saw the 2Y yield rise 3bp while the long-end moved lower by 2-4bp. US economic data was mixed. US preliminary Durable Goods Orders for June dropped sharply by 6.6% vs. expectations of a 0.3% rise on the back of a near 20% fall in commercial aircraft orders. On a positive note, ex-transport orders were up 0.5% vs. expectations of 0.2%. Initial jobless claims rose by 235k vs. the surveyed 238k. US equities continued to dip with the S&P and Nasdaq down 0.5% and 0.9% respectively. US IG and HY CDS spreads widened by 0.7bp and 3.1bp respectively.

European equity markets were mixed. Looking at Europe’s CDS spreads, the iTraxx Main and Crossover spreads widened by 0.5bp and 1.6bp respectively. Asian equity indices have opened in the green this morning. Asia ex-Japan CDS spreads were wider by over 2bp.

New Bond Issues

Rating Changes

- Vedanta Resources Upgraded To ‘B-‘ From ‘CCC+’ On Improving Capital Structure And Liquidity; Outlook Stable

- Moody’s Ratings upgrades Carnival Corporation’s CFR to B1, outlook positive; downgrades taxable revenue bond issued by Long Beach (City of) CA

- Moody’s Ratings upgrades Volcan’s CFR to Caa1; places all ratings under review for further upgrade

- Fitch Upgrades EQM’s Rating to ‘BB+’ Following Acquisition by EQT

- Fitch Revises Arabian Centres’s Outlook to Negative; Affirms IDR at ‘BB+’

Term of the Day

Private Placement

A private placement is a sale of securities directly to select private investors, rather than issuing them via a public offering. Investors in privately placed bonds generally comprise large banks, mutual funds, or insurance companies. The advantage of private placements is that they may not be subject to the same strict regulations regarding disclosure and reporting of public offerings. Also, the cost and time savings add to its attractiveness. On the other hand, they may carry a higher rate to entice investors and they limit the number and variety of investors that can take part unlike public offerings. Unlike bonds issued via public offerings, privately placed bonds may not trade on the secondary market.

Talking Heads

On ECB Should Be Able to Cut If Data Stay on Course – Joachim Nagel

“If the figures remain the same over the next twelve months, there might be a chance that we can reduce interest rates further at one or the other meeting”… ECB isn’t on “autopilot”

On Markets Tearing Up Popular Trades That Reached ‘Stupid Levels’

Louis-Vincent Gave, chief executive officer of Gavekal Research

“It does seem that an unwinding has begun of popular trades that brought valuations to stupid levels”

Torsten Slok, chief economist at Apollo Global Management

“If the economy starts slowing down, the speed of the slowdown becomes essential. A faster slowdown would have negative implications for earnings… increase the probability of a selloff in stock markets and credit markets”

James Athey, portfolio manager at Marlborough Group

“Valuations of mega-cap tech were increasingly impossible to justify with anything but the most heroic forecast for future growth, earnings and monetary policy”

On global investors scrambling to dodge US election curveballs

Ross Yarrow at investment bank Baird

“Markets hate uncertainty and, as the polls head towards 50-50, this is about uncertain as it can get”

Trevor Greetham, Royal London

“We think there’s the potential for markets to get more nervous about the U.S. presidential race… We could find the U.S. Treasury market starts to get antsy towards November if both (candidates) are saying they will spend more”

Top Gainers & Losers- 26-July-24*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.