We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

UBS Raises $3.5bn Via Dual AT1 Bonds at 9.25%

November 9, 2023

UBS raised $3.5bn via a dual-trancher AT1 issuance, its first since Credit Suisse’s historic AT1 write-down. The deal was met with strong demand, receiving combined orders of more than $36bn, over 10x issue size.

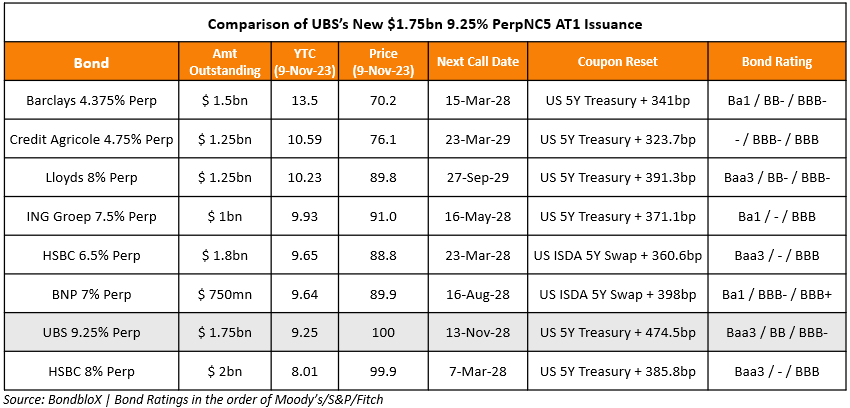

– It raised $1.75bn via a PerpNC5 AT1 bond at a yield of 9.25%, a solid 75bp inside initial guidance of 10% area. If not called before the call date on 13 November 2028, the coupons will reset to the US 5Y Treasury plus 474.5bp then, and every five years thereafter. The table above compares the latest UBS 9.25% PerpNC5 against similar rated European AT1s to assess relative value.

– It also raised $1.75bn via a PerpNC10 AT1 bond at a yield of 9.25%, a massive 87.5bp inside initial guidance of 10.125% area. If not called before the call date on 13 November 2033, the coupons will reset to the US 5Y Treasury plus 475.8bp then, and every five years thereafter. While the new 9.25% PerpNC10 does not have a direct comparable, they are priced 68bp tighter to UBS’ older 4.375% Perp (callable in February 2031, with a reset of US 5Y Treasury + 331.3bp) that currently yield 9.93%.

Both the junior subordinated notes are rated Baa3/BB/BBB-. Upon the occurrence of a trigger event or viability event a contingent write-down will occur and the full principal amount and any accrued/unpaid interest will permanently be written-down to zero. Steven Boothe, head of global IG fixed income at T. Rowe Price said, “At current yields you are getting decent compensation for these risks”.

Go back to Latest bond Market News

Related Posts:

UBS Said to be Lining Up AT1 Issuance

August 28, 2023

UBS’s AT1 Yield Premium Over non-Swiss Peers Vanishes

October 4, 2023

HSBC, UBS Report Earnings

October 26, 2022

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.