We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

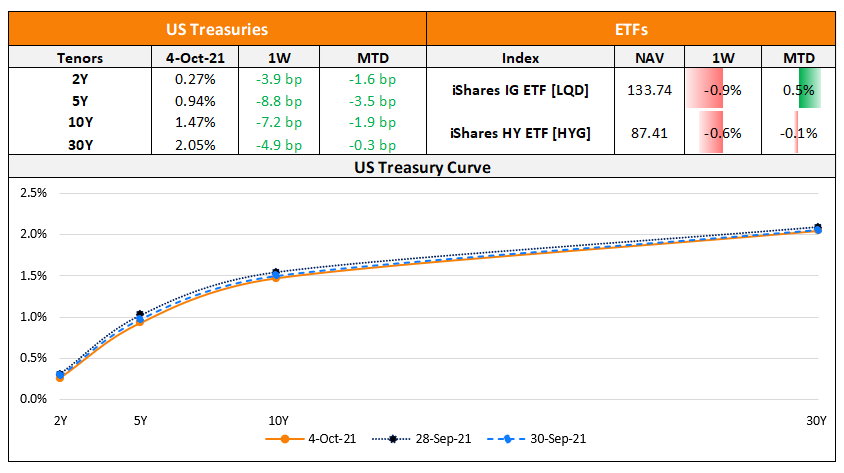

The Week That Was (27 Sep to 3 Oct 2021)

October 4, 2021

US primary markets saw an increase issuance to $27.8bn vs. $21.2bn in the prior week. IG issuances rose to $14.1bn vs. $8.2bn in the prior week and HY issuances were also higher at $ 13.4bn vs. $11.6bn in the prior week. The IG space was led by Charter Communications’ $4bn three-trancher and Analog Device’s $3.5bn four-part deal. In the HY space, Medline raised alone $7bn via a dual-trancher, the largest junk-bond deal since 2015. In North America, there were a total of 41 upgrades and 26 downgrades combined across the three major rating agencies last week. LatAm saw $2.2bn in issuances vs. only $150mn in the week prior led by Guatemala’s $1bn two-part issuance and Becle SAB’s $800mn deal. In South America, there were 7 upgrades and 8 downgrades combined across the major rating agencies. EU Corporate G3 issuances on the other hand fell to $17.3bn vs. $29.4bn in the week prior led by Grifols’ $2.31bn multi-currency dual-trancher and ING-DiBa AG’s €1.25bn deal. Across the European region, there were 38 upgrades and 20 downgrades across the three major rating agencies. GCC G3 issuances saw $300mn in issuances last week as compared to no issuances in the week before that with Qatar International Islamic Bank raising $250mn. Across the Middle East/Africa region, there were 4 upgrades and 2 downgrades across the three major rating agencies. APAC ex-Japan G3 issuances saw an increase to $7.35bn as compared to only $2.2bn in the week before that was marred by volatility on concerns over Evergrande and contagion risks. NBN Bank raised $2bn via a three-part deal, Commonwealth Bank of Australia raised $1.5bn and Macquarie raised $1bn as Aussie companies lead the tables. In the Asia ex-Japan region, there were 9 upgrades and 11 downgrades combined across the three major rating agencies last week.

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.