We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

NFP Sees 92k Drop; Treasury Yields Jump as Brent Surges to $115/bbl

March 9, 2026

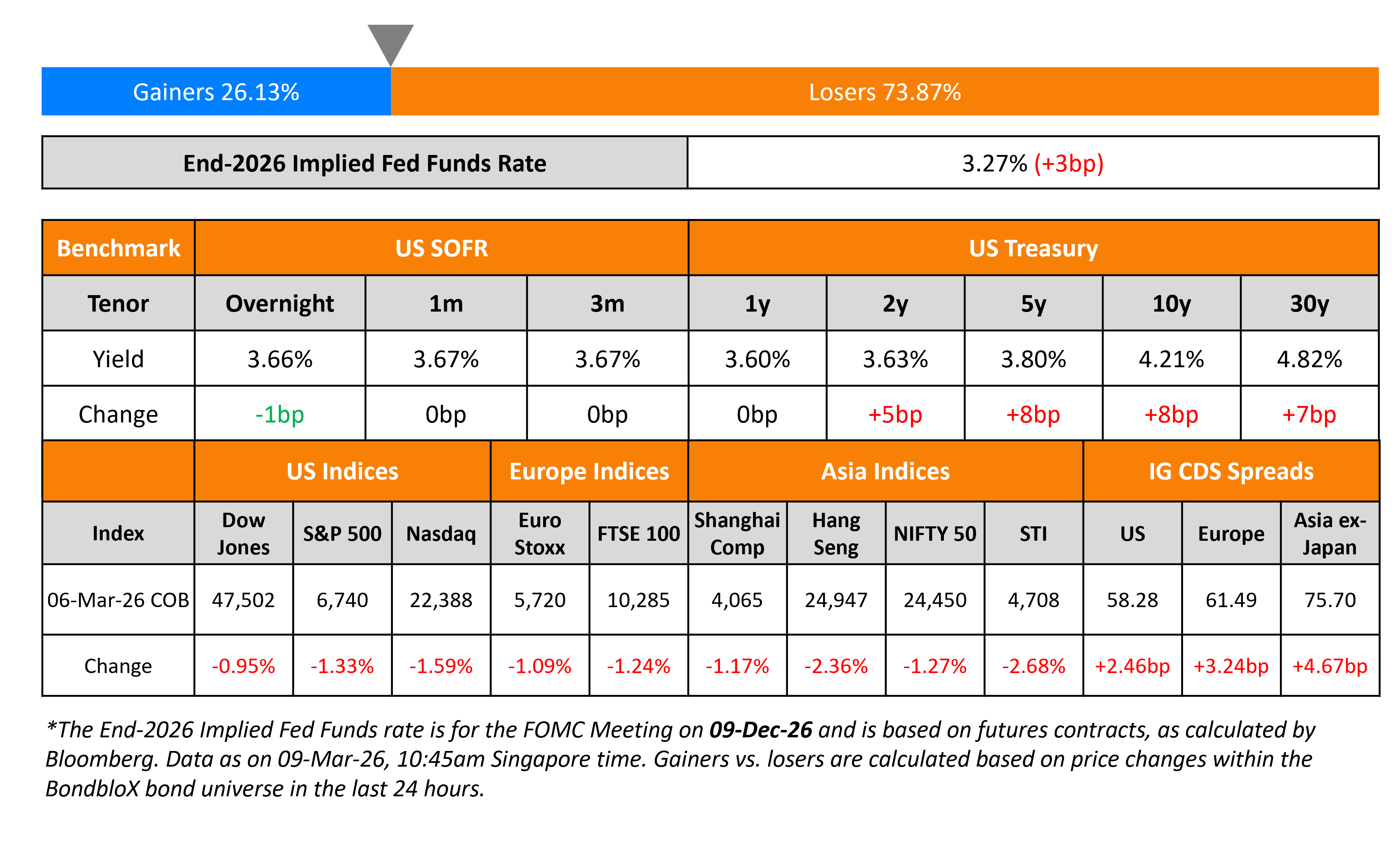

US Treasury yields jumped higher by 5-8bp with oil prices breaching the $100/bbl mark. Brent crude surged to trade at $115/bbl amid fears of prolonged supply shortages due to the war in the Middle East. Besides the Strait of Hormuz being blocked, Yemen is also said to have closed the shipping strait Bab-el Mandab. Analysts cite inflationary concerns due to the geopolitical developments, and markets are now pricing-in only one 25bp rate cut this year as compared to nearly two cuts a week ago. On the data front, US NFP for February showed a drop of 92k jobs, coming in much below estimates of a 55k gain. Besides, the NFP numbers for the December and January were also revised lower. Average Hourly Earnings (AHE) YoY rose by 3.8%, higher than the surveyed 3.7%. The Unemployment Rate inched higher to 4.4%. The soft jobs report came on the back of the winter storms, labor strikes in the healthcare sector and government jobs layoffs that slowed hiring activity.

Looking at US equity markets, the S&P and Nasdaq ended lower by 1.3% and 1.6% respectively. US IG CDS spreads widened by 2.5bp and HY CDS spreads were 13.2bp wider. European equity indices ended lower too. The iTraxx Main CDS spreads were 3.2bp wider and the Crossover CDS spreads were 15bp wider. Asian equity markets have opened sharply lower this morning. Asia ex-Japan CDS spreads widened by 4.7bp.

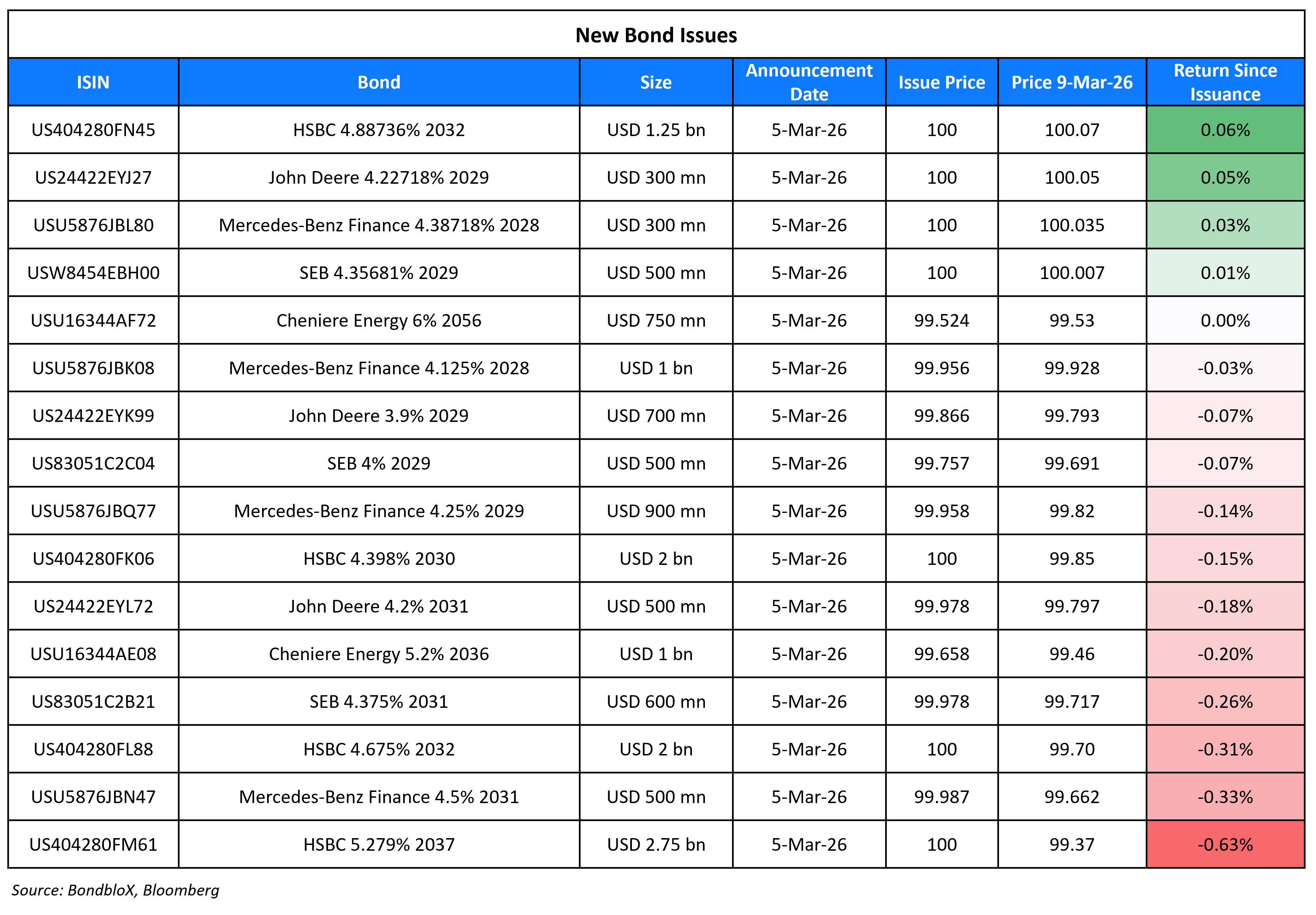

New Bond Issues

- ICBC (Luxembourg) € 3Y at MS+55bp area/ ICBC (London) £ 3Y at UKT+75bp area/ ICBC (HK) $ 3Y FRN at SOFR+100bp area

Rating Changes

- Fitch Upgrades Commonwealth Bank of Australia to ‘AA’; Outlook Stable

- Moody’s Ratings downgrades Yuexiu Property’s ratings to Ba2; outlook stable

- Moody’s Ratings upgrades Seazen Group’s ratings to B3/Caa1; outlook stable

- Fitch Upgrades CK Hutchison to ‘A’; Outlook Stable; Resolves UCO

- Cosan S.A. Downgraded To ‘BB-‘ From ‘BB’ And Placed On CreditWatch Negative On Weaker Financial Flexibility

- Rumo S.A. Ratings Lowered To ‘BB-‘ From ‘BB’ And Placed On CreditWatch Negative Following Same Action On Parent Cosan

- Moody’s Ratings downgrades Beazer Homes’s CFR to B2; stable outlook

- Moody’s Ratings downgrades VMED O2’s CFR to B1 from Ba3; outlook remains negative

- Fitch Revises Portugal’s Outlook to Positive; Affirms IDR at ‘A’

- Moody’s Ratings changes Morocco’s outlook to positive from stable; affirms Ba1 rating

Term of the Day: Net Asset Value (NAV)

Net Asset Value (NAV) is the value of a fund’s assets minus its liabilities per unit at a point in time. It is calculated as the (Value of Assets-Value of Liabilities)/number of units outstanding. NAV is often associated with mutual funds and ETFs, and helps an investor track the fund’s performance. NAVs should not be confused with the market price for example in an ETF. The latter is just the price at which shares in the fund can be bought or sold determined by demand and supply while the former is more akin to book value.

Talking Heads

“My expectation has been that inflation would start making progress towards our 2% target. I don’t think we’ll get there by the end of this year by any stretch, but I think we’ll make some decent progress… rates should be on hold for …quite some time”

On Bond Traders Awaiting US Inflation Data With Oil Rise in Focus – Kevin Flanagan, WisdomTree

“The energy market is still top of mind for bond investors, and the data is taking a backseat… will get knee-jerk moves in bonds as we saw after payrolls, but what’s going on in oil is the focus of the bond market”

On Iran Conflict Putting EM Revival to the Test

Nick Eisinger, JPMorgan Asset Management

“We’re waiting for more clarity… We like the fundamental story across a lot of EM, but unfortunately the fundamental stories don’t really count for very much right now”

Bill Campbell, DoubleLine Group

“I’m not in the camp that this fundamentally changes everything, that it’s time to close out all emerging markets. I’m much more in the camp that this is an exogenous shock”

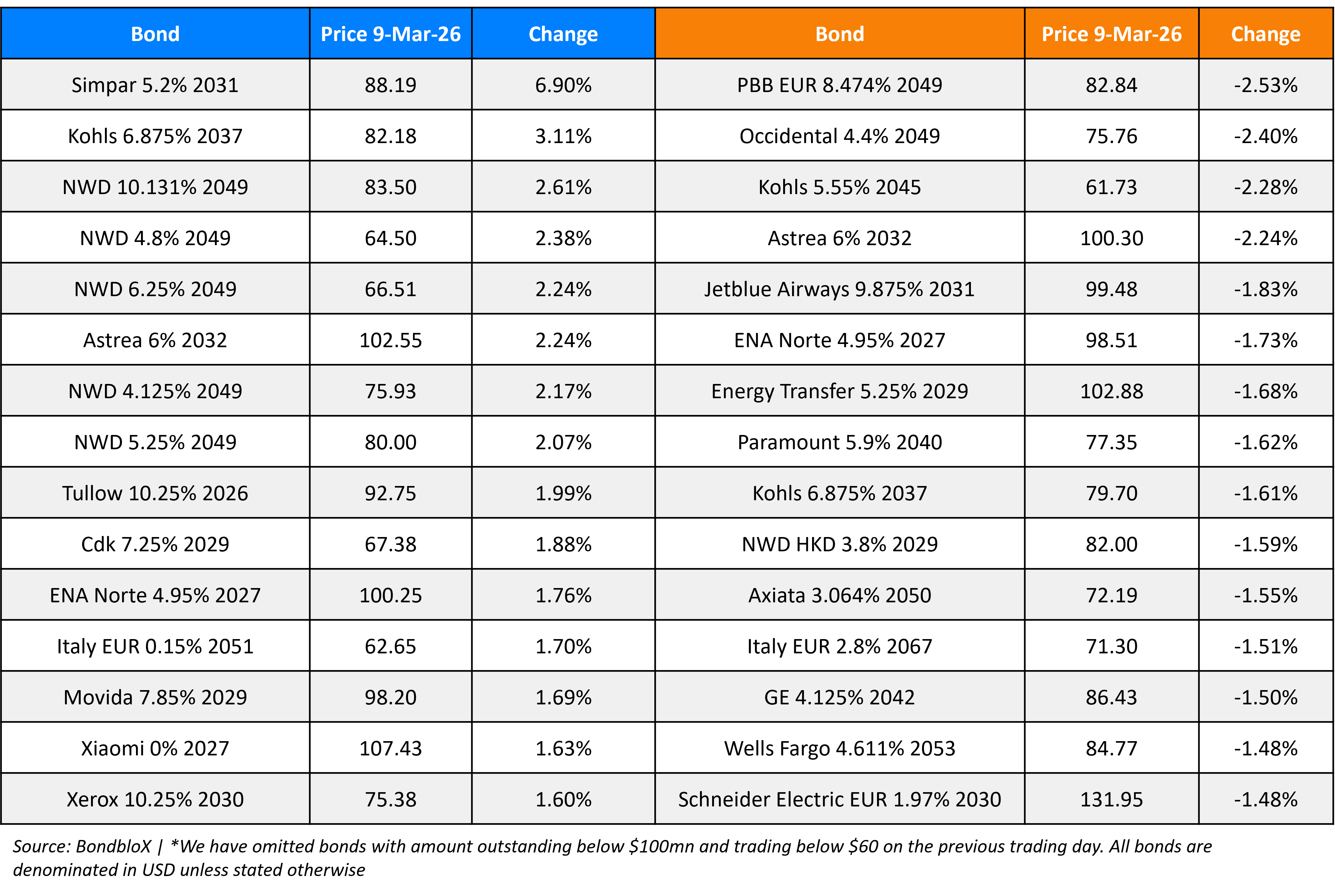

Top Gainers and Losers- 09-Mar-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.