We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

January 2024: 54% of Dollar Bonds End Higher Thanks to Late Rally

February 1, 2024

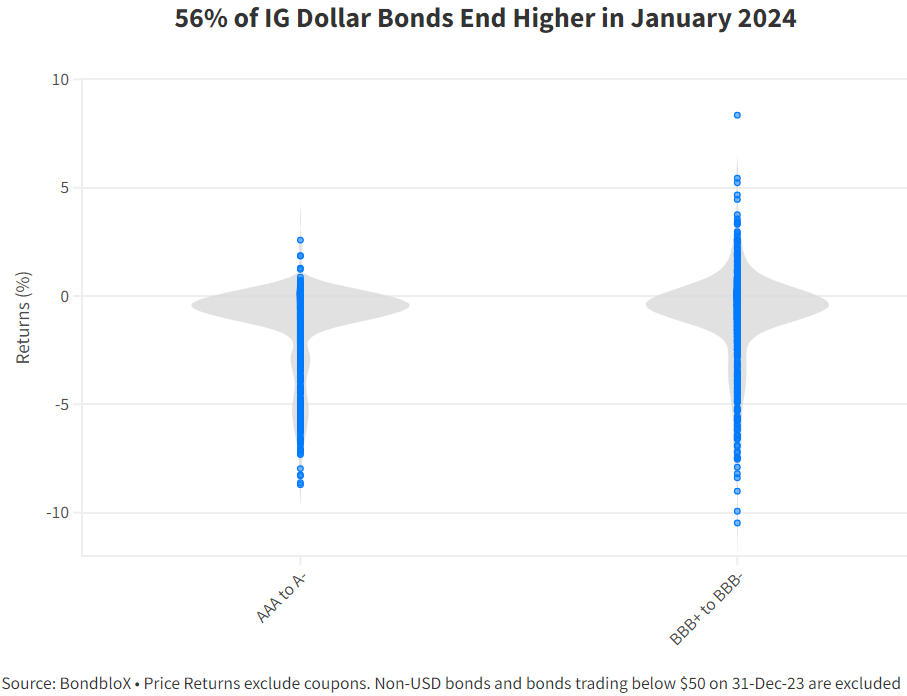

The first month of 2024 was a mixed bag for bond investors with 54% of dollar bonds ending higher. About 56% of IG bonds ended higher and about half of the HY bonds ended higher. This comes after a late rally on the last few days of the month, leading up to and following the FOMC meeting on 30-31 January (scroll for details).

January saw longer-term Treasury yields inch higher after markets repriced their expectations of Fed rate cuts in 2024. The 2Y yield closed almost unchanged at 4.24% and the 10Y yield was up 6bp to 3.95% during the month, after a late-rally in the last week, owing to a reduction in the US Treasury's federal borrowing estimate for 1Q 2024 and regional banking fears. The US Treasury now estimates $760bn in net borrowing for the current quarter, down from a previous $816bn estimate released in late October 2023.

The US economy continued to show resilience, beginning the month with the non-farm payrolls (NFP) showing a pick-up of 216k jobs, higher than the surveyed 175k. Average Hourly Earnings (AHE) YoY rose 4.1%, higher than the surveyed 3.9%. Besides, US inflation also showed an uptick, with December CPI YoY up 3.4%, the most in three months. This was above estimates of 3.2% and the prior month’s 3.1%. Core CPI YoY also rose 3.9%, higher than the estimated 3.8%. Manufacturing activity improved slightly, albeit in a continued contractionary state. The notable move in yields were seen in the 30Y where yields initially rose by 28bp over the course of the month, helped by a weak auction where demand hit its lowest levels since December 2021. Primary dealers had to buy 18.2% of the 30Y that saw a bid-to-cover ratio of 2.37x, lower than the prior 2.43x. However, the reduction in auction sizes and the late risk-off move saw 30Y yields ease, ending the month 15bp higher.

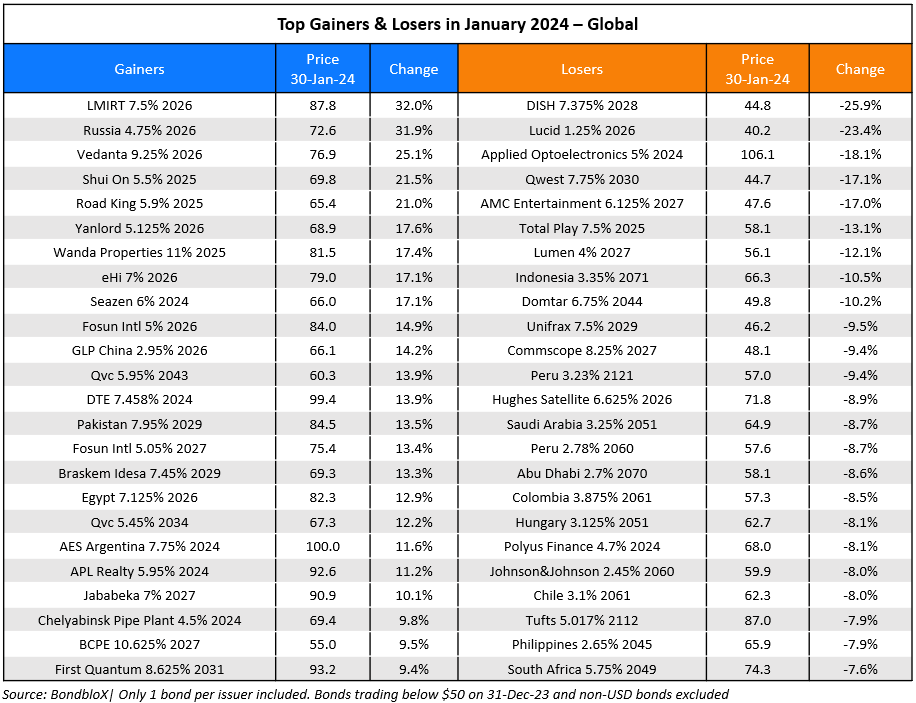

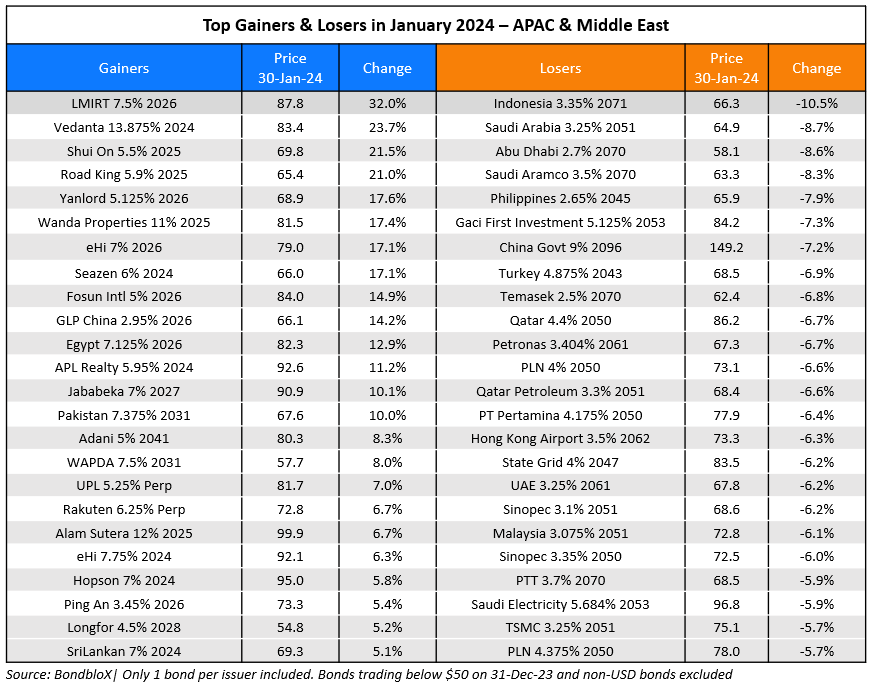

In the IG space, the biggest gainers were bonds of Adani Group after it got a clean chit from the Supreme Court on SEBI's probe and its subsidiary, Adani Green securing funding to redeem its September 2024s. Also, bonds of Chinese property developers and related REITS including those of Beijing Capital, Longfor and China Vanke continued to inch up on the back of Beijing's easing measures. Longer-dated bonds of sovereigns such as Indonesia, Philippines, Saudi Arabia and Abu Dhabi were among the top losers in the IG space due to the jump in the 30Y Treasury yield by ~40bp until earlier last week.

In the HY space, top gainers included the 2024s and 2026s bonds of Lippo Malls for which the company had launched a tender offer last month. Vedanta's dollar bonds were also among the gainers on the back of the company getting bondholders' consent for its debt restructuring. Similar to the IG space, gainers in the HY segment also included Chinese corporates related to the real estate sector like Road King, Yanlord, Shui On, Seazen and others. The losers in HY were mainly concentrated among longer dated bonds of sovereign and sovereign related entities like HK Airport, Oman and Sharjah that fell primarily owing to the jump in longer dated treasury yields. Egypt's bonds were also among popular losers as Moody's changed its outlook to negative citing the difficult macroeconomic conditions faced by the country.

Issuance Volumes

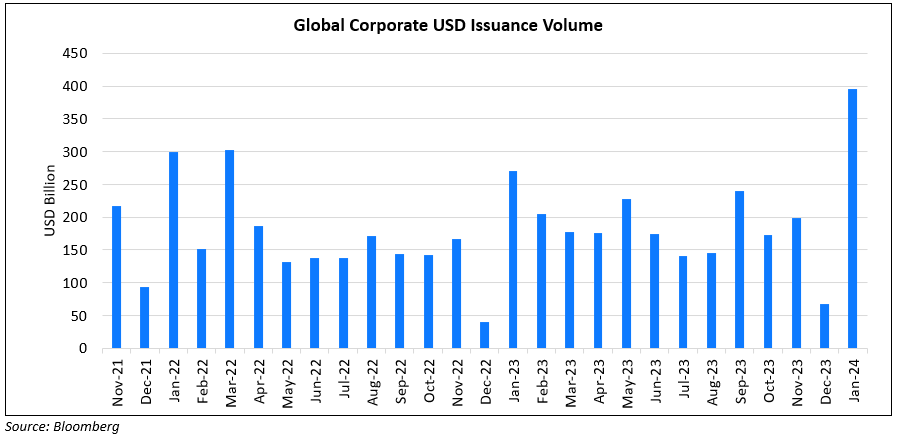

Global corporate dollar bond issuances stood at $396bn in January, ~5x higher than December. As compared to January 2023, issuance volumes were up 1.5x. 88% of the issuance volumes came from IG issuers with HY comprising 11% and unrated issuers taking the remainder.

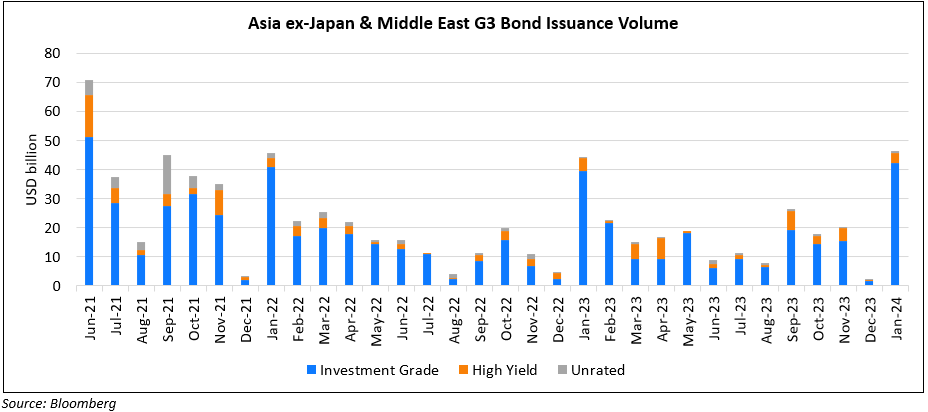

Asia ex-Japan & Middle East G3 issuance stood at $48.5bn, up 23x MoM and 1.1x YoY. 89% of the volumes came from IG issuers with HY issuing 9% and unrated issuers taking the rest.

Largest Deals

Several big banks across US and Europe dominated the issuance volumes globally, following their earnings releases. These included JPMorgan's and Wells Fargo’s $8.5bn and $8bn four-trancher deals each, SocGen that raised $5bn via a five-trancher and Lloyds' ~$4.35bn dual-currency issuance.

In the APAC and Middle East region, deal volumes were led by Saudi Arabia’s $12bn four-trancher, followed by Saudi PIF’s $5bn three-tranche sukuk and NAB’s $3.25bn four-part deal. Besides, other large deals included Indonesia’s $2.05bn and KEXIM’s $2bn three-tranchers each, SK Hynix’s $1.5bn two-trancher and KEPCO’s $1.2bn deal.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

Bond Yields – Explained

December 26, 2024

Bond Investors Up $75.4 Billion in 1Q19

April 10, 2019

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.