We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

ISM Manufacturing Stays in Contraction Territory

December 4, 2023

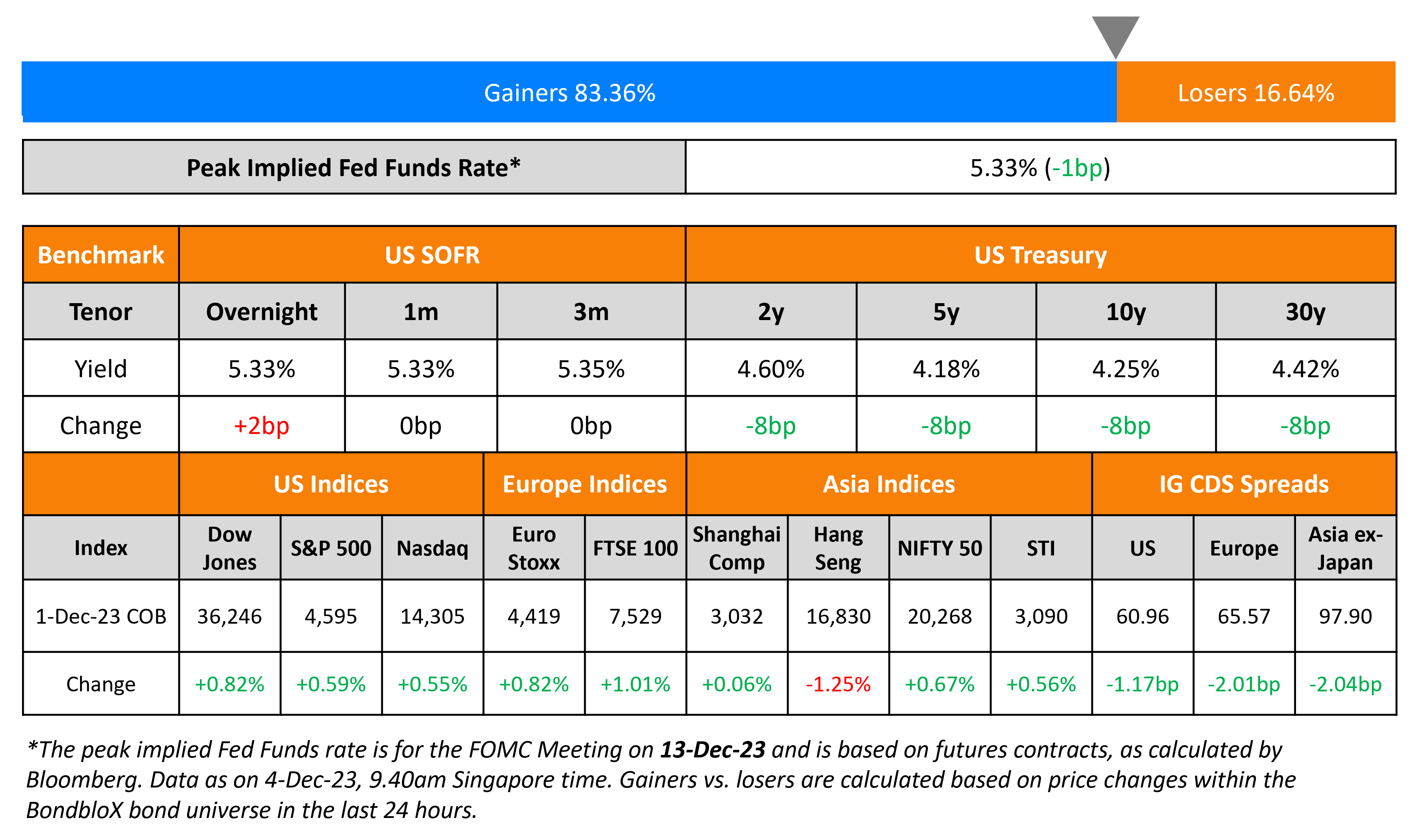

US Treasury yields were down by 8bp across the curve on Friday. Fed Chairman Jerome Powell noted that policy is “well into restrictive territory”, though the central bank is ready to hike further if needed. Separately, US ISM Manufacturing PMI was unchanged at 46.7 last month, the thirteenth consecutive month that the PMI stayed below 50, indicating a contraction in manufacturing. US credit markets saw IG CDS spreads tighten 1.2bp and HY tightening 6.7bp. Equity markets ended the week in the green, with the S&P and Nasdaq up ~0.6% each.

European equity markets were higher too. In credit markets, European main CDS spreads were tighter by 2bp and crossover spreads tightened by 9.7bp. Asian equity markets have opened weaker today. Asia ex-Japan IG CDS spreads were tighter by 2bp.

New Bond Issues

Guangzhou Development raised $500mn via a 2Y green bond at a yield of 6.3%, 45bp inside initial guidance of 6.75% area. The senior unsecured bonds have expected ratings of BBB+ (Fitch), and received orders over $1.4bn, 2.8x issue size. Proceeds will be used to finance/refinance Eligible Green Projects as defined in the Company’s Green Finance Framework.

New Bond Pipeline

- Guangzhou Development District hires for $ green bond

Rating Changes

-

Fitch Upgrades Greece to ‘BBB-‘; Outlook Stable

-

Moody’s downgrades Seazen Group’s ratings to B2/B3; outlook negative

-

Fitch Downgrades Ardagh Group’s IDR to ‘B-‘; Outlook Negative

-

PG&E Corp., Pacific Gas And Electric Company Outlooks Revised To Positive From Stable On Rate Increase; Ratings Affirmed

Term of the Day

Restricted Group/Subsidiaries

Restricted Group or restricted subsidiaries refer to a parent or holding company’s subsidiaries that are tied to the debt covenants of the parent issuer. Restricted groups may have covenants that restrict cash upstreaming to shareholders, additional indebtedness, liens, dividend payments, making new investments etc. Unrestricted subsidiaries on the other hand are not bound by the parent or holdco’s bond covenants and are thus not required to support repayment of the debt securities.

Take the case of a parent company that has various subsidiaries, and that the debt is issued at the parent’s or holdco’s level. Here, a restricted subsidiary’s assets are ringfenced such that during normal operations, the parent company is not able to use the cash of these units via transactions like inter-company loans etc. simply because it is a holding company. Therefore, in the event of distress, given that restricted subsidiaries are bound by restrictive debt covenants, bondholders’ credit risk is reduced as they have access to assets of the restricted subsidiary.

Talking Heads

On ECB Nearing The End of Rate Hikes

Francois Villeroy de Galhau, Bank of France Governor

“Barring any shock, rate hikes are now over. The question of a cut may arise when the time comes during 2024, but not now: when a remedy is effective, you have to be patient enough on its duration.”

On Regional Bank Debt Being a Bargain

Scott Kimball, chief investment officer at Loop Capital

“Loop Capital has been combing the secondary market for bargains, expecting most lenders to pull through if benchmark rates stabilise and the economy continues to grow.”

On Buying Emerging Market Debt

Pramod Dhawan, Pacific Investment Management Co.’s head of emerging-market debt

“I’m very fundamentally positive. EM is an under-owned asset class, but when you look under the hood and you dig a little bit deeper, then this is an asset class you should want to own.”

Brad Gibson, co-head of Asia-Pacific fixed income at AllianceBernstein

“At times when an investor could collect a yield of about 5% by owning a US 2Y bond, why would you buy Indonesia? Why would you buy anything else?”

Top Gainers & Losers- 04-December-23*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.