We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Fed Takes Dovish Stance Post 25bp Hike

July 27, 2023

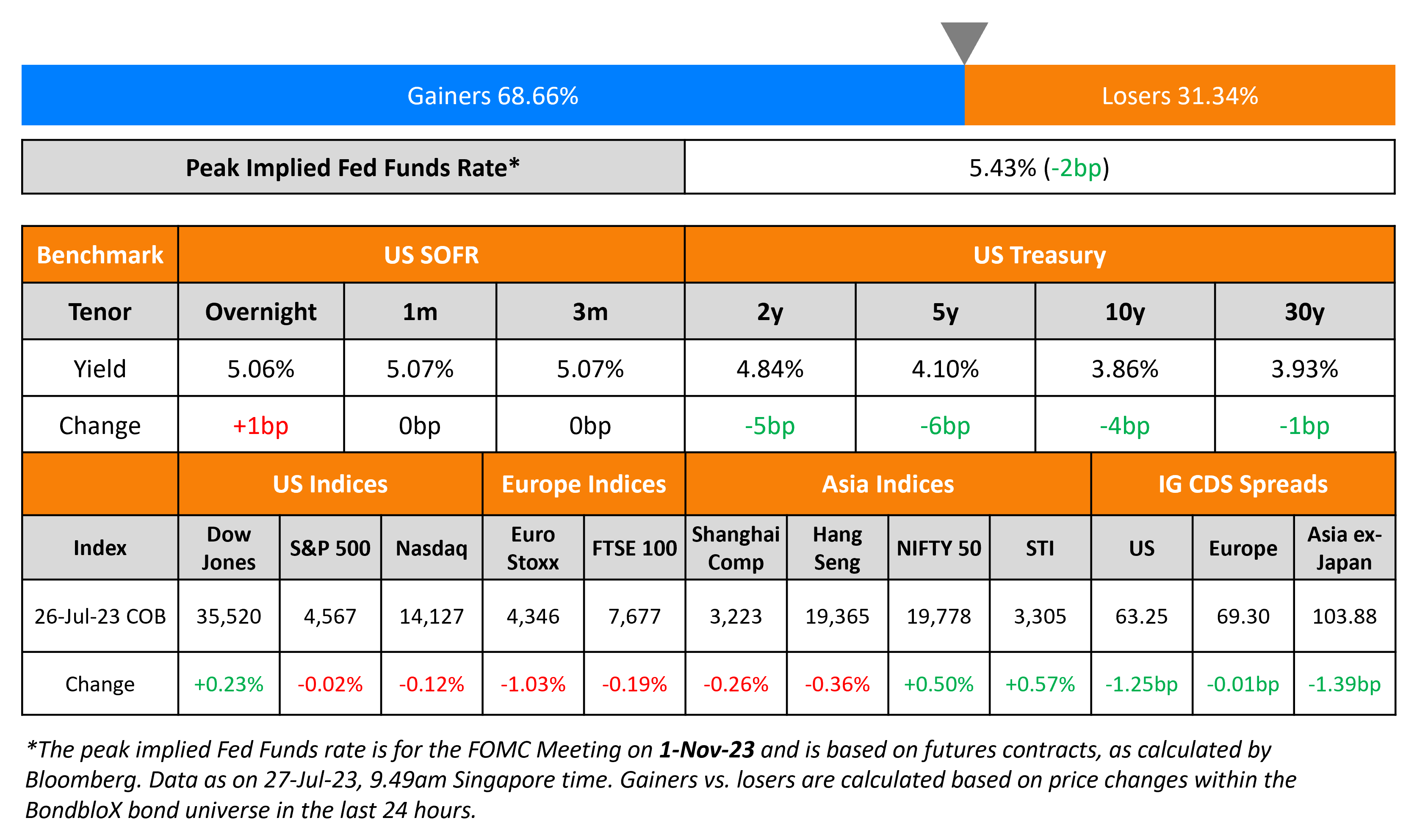

Treasury yields inched lower by 4-6bp across the curve on Wednesday after the FOMC meeting was considered to have a relatively dovish tone. The FOMC hiked interest rates by 25bp with the policy Fed Funds Range at 525-550bp. Fed Chair Jerome Powell highlighted that the interest rate decision in September will be data dependent, with two more jobs reports and two more inflation reports to be released before the meeting takes place. Further, he mentioned that Fed staff no longer forecast a recession. The peak Fed Funds rate eased 2bp to 5.43%. US IG credit spreads tightened 1.1bp while HY CDS spreads were tighter by 5.3bp. The S&P and Nasdaq ended almost flat.

European equity indices closed lower. The ECB is expected to hike its policy rates by 25bp European main CDS spreads were flat and Crossover CDS tightened 0.8bp. Asia ex-Japan CDS spreads continued to tighten, by 1.4bp to 103.88bp. Asian equity markets have opened lower this morning.

.png)

New Bond Issues

Hangzhou Qiantang raised $300mn via a 3Y bond at a yield of 6.28%, 42bp inside initial guidance of 6.7% area. The senior unsecured bonds are unrated. Proceeds will be used to repay $300mn of the issuer’s outstanding 3.2% bond that will mature in August 2023. The bonds have a change of control put at 101.

Rating Actions

- Fitch Upgrades Brazil to ‘BB’; Outlook Stable

- Las Vegas Sands Corp. And Sands China Ltd. Raised to ‘BBB-’ On Macao Recovery And Strong Singapore Performance

- Moody’s downgrades Dish Network’s CFR to Caa1; outlook negative

Term of the Day

Dovish

A dovish stance is a central banking policy stance which is accommodative, in favour of maintaining interest rates at low levels and generally not worried about inflation. This stance is generally taken to ease financial conditions from the monetary policy side to stimulate the economy.

Talking Heads

On Further Fed Rate Decisions Beyond July

Jerome Powell, Fed Chair

“(Jobs reports, consumer-price inflation reports and employment costs data are) going to inform our decision as we go into (the September FOMC) meeting…It is certainly possible that we would raise (rates) again at the September meeting, if the data warranted. And I would also say it’s possible that we would choose to hold steady at that meeting.”

Stephen Stanley, chief US economist at Santander US Capital Markets

“The default at this point is that the Fed is going to go again – at least once more…But the timing is open and will depend on the data. He emphasized yet again that the Fed is taking things on a meeting by meeting basis.”

Anna Wong, chief US economist at Bloomberg

“While the lack of substantive changes to the policy statement suggests the majority of officials still want to keep the door open for another rate hike, Chair Jerome Powell’s somewhat dovish performance at the post-meeting news conference suggests a willingness to skip a hike at the September meeting, provided inflation data continue to be soft.”

On the ECB Rate Decisions Beyond July

Piet Haines Christiansen, economist at Danske Bank

“Some timely indicators as the Indeed Wage Tracker, which tracks listed wages on job postings, has shown some softening during 2023, but the labour market impulse to inflation still appears way too strong on most broad wage measures.”

Anatoli Annenkov, senior European economist at SocGen

“We see little room for an easing of the hawkish bias just yet…We still see mainly upside risks to inflation and expect a final 25 basis point hike in September before the focus shifts to the balance sheet at the end of the year.”

Jan von Gerich, chief strategist for global research at Nordea Markets

“A pause after July would likely require further falls in realised core inflation, downward revisions in staff inflation forecasts and more signs of monetary policy transmission in the real economy.”

On the Attractiveness of Angolan Debt Over Kenyan Debt

Strategists at Morgan Stanley

“It’s now time to turn to a like stance on Angola, given that valuations are screening cheap…We now prefer Angola’s long end relative to the Kenyan long end given the balanced outlook for the former and the downside risks for the latter.”

Oren Barack, managing director of fixed income at Alliance Global Partners

“Angola — with its limited short-term financing needs and oil prices trending higher — is looking like a good alternative…The government is undertaking an unpopular but necessary decision to cut local subsidies for fuel for the domestic market, which will improve their current account balance and shore up finances.”

On Concerns Over Italy’s Debt – IMF

“Growth is expected to enter a slower phase and downside risks dominate the outlook…Policies that slow public debt reduction or prolonged delays in receiving NextGenerationEU (NGEU) disbursements could raise financing concerns…(while) a sharper tightening of monetary policy could transmit asymmetrically to Italy and further raise borrowing costs.”

On the Mexican Government Announcing Support for Pemex’s Debt – Mexican President AMLO

“Pemex’s debt is the country’s debt, they go together. It doesn’t make any sense that Pemex would give away money to big financial companies, to big banks…The president of the republic has determined that now the bond issuances or refinancings be done by the Finance Ministry according to the financial costs of the sovereign, and this will save the country a lot of money.”

Top Gainers & Losers – 27-July-23*

Other News

Go back to Latest bond Market News

Related Posts:

Fed’s Dudley Shakes Up Complacent Markets

June 20, 2017

Fed Survey Results Supportive of Funds Flow into Bonds

September 10, 2017

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.