This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

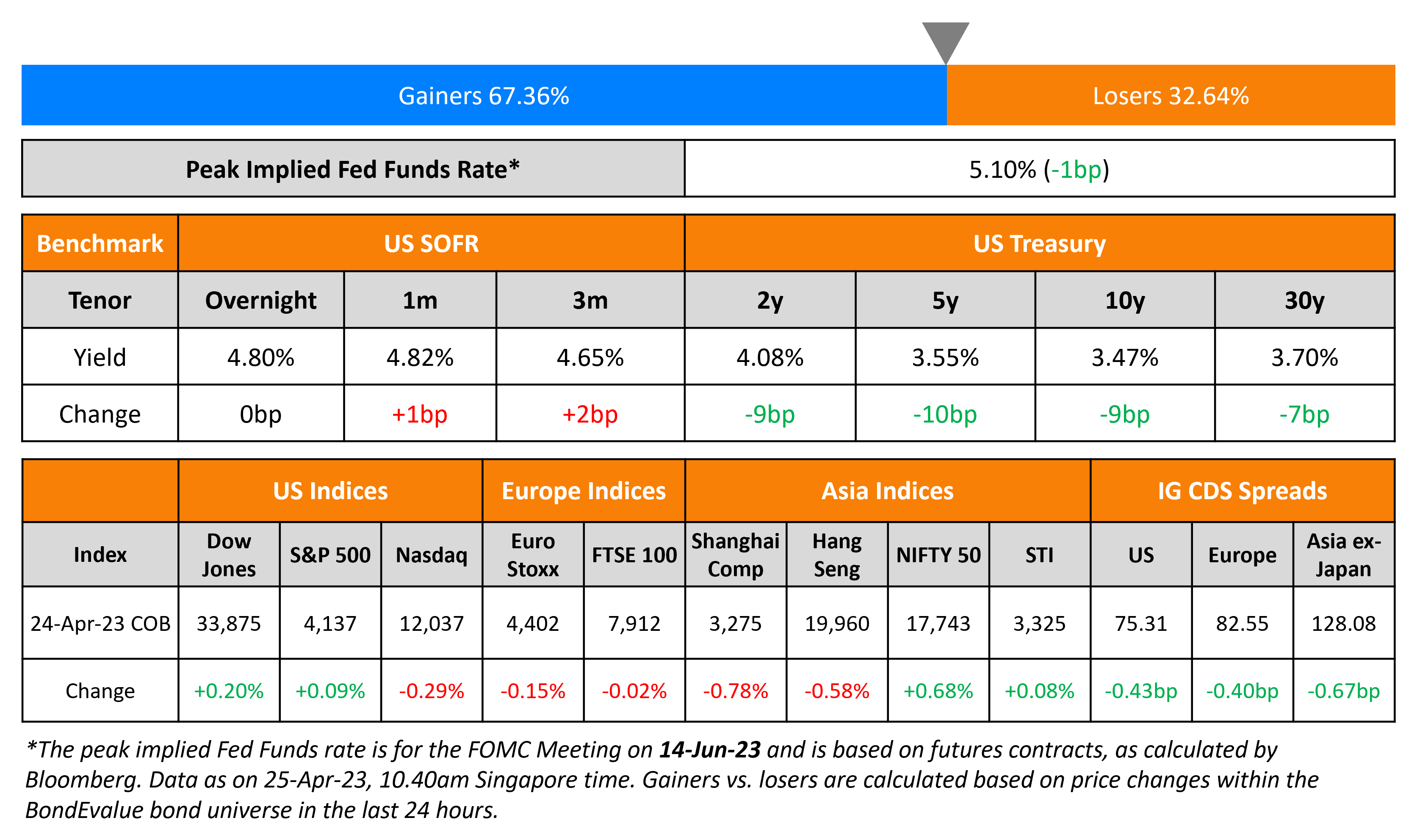

American Airlines Upgraded to B+

July 20, 2023

American Airlines was upgraded to B+ from B- by Fitch. The primary reasons cited were significant deleveraging progress, healthy demand outlook and improved profitability. American Airlines is expected to reduce its total adjusted debt to $43bn by end-2023 from a peak of over $48bn in 2021, with this number forecasted to go even lower to the low-to-mid $30bn range by end-2025, thanks to its de-leveraging goal of reducing total debt by $15bn by end-2025. American Airlines’ leverage is also expected to go down from 5.3x in end-March to 4.7x by the end of the year. Furthermore, demand is expected to remain strong for 2023, with a healthy level of forward bookings pointing towards sustained traffic growth for this year. Consumer resilience is also likely to be observed even if a mild recession occurs due to an increased priority in consumers spending on experiences rather than goods coming out of the pandemic. Finally, American Airlines is expected to improve its profitability as normal operations resume against the backdrop of a post-pandemic era, with margins for the year possibly reaching pre-pandemic levels. Its profits are also amplified by a more than 40% reduction in jet fuel prices as compared to a year ago.

American Airlines’ 3.375% 2027s have trended 1.8% higher since the start of the month and are currently trading at 89.8 cents on the dollar, yielding 9.21%.

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.