This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Xerox Downgraded to Caa2 by Moody’s

March 16, 2026

Xerox Holdings Corporation was downgraded by three notches to Caa2 from B2 by Moody’s. The downgrade reflects Xerox’s weak performance following last year’s Lexmark acquisition and high leverage. The rating agency also highlighted that Xerox may need to restructure its debt if it struggles to refinance maturities before 2028 amid declining demand in the printer market. Despite potential cost synergies from the Lexmark deal and diversification benefits from acquisitions such as ITsavvy, Xerox faces pressure from larger competitors including Canon, FUJIFILM, and HP. Xerox’s pro forma leverage (debt-to-EBITDA) stood at ~6x at end-2025, while cash flow remained weak despite modest free cash flow. Moody’s noted that Xerox had adequate liquidity, supported by $512mn in cash, proceeds from a joint venture transaction, and an asset-based lending facility. However, it warned that sustained revenue declines and negative underlying cash flow could pressure Xerox’s ability to manage its capital structure.

It’s 13.5% 2031s traded at distressed levels of 47.1 cents on the dollar.

Go back to Latest bond Market News

Related Posts:

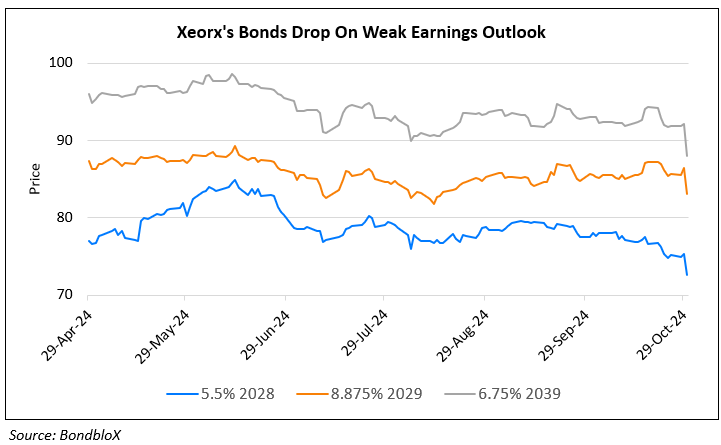

Xerox Bonds Drop on Weak Earnings and Lowered Guidance

October 30, 2024

Xerox Downgraded to B- by S&P

October 14, 2025

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.