This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

US 2Y Yield Drops 27bp on News of Banking Stress

March 10, 2023

US 2Y and 5Y Treasury yields dropped by a massive 23-27bp yesterday as risk-off (Term of the Day, explained below) sentiment caused a sharp rally in front-end Treasuries. This happened after Silicon Valley Bank (SVB) shares dropped 60% after it announced a $2.25bn stock offering, stoking concerns about eroding balance sheets in US banks and thereby the need for capital raises. Shares across the US banking sector dropped over 5% due to the impact of this. However bonds were relatively stable across the banking sector. US 10Y and 30Y Treasury yields were lower by 13bp and 8bp respectively.

Due to the above risk-off move, markets are now pricing in a 63% chance of a 50bp rate hike in March vs. 79% a day ago. Prior to yesterday’s incident, markets were pricing-in three more hikes of 25bp each at the subsequent FOMC meetings in May, June and July. However currently, markets have priced out a 25bp hike in July whilst maintaining two 25bp hikes in May and June. Besides, US weekly jobless claims rose to 211k, its highest in ten weeks, with a 21k increase over the prior week. This was the largest increase since October 2022.

On the back of the above news, the peak Fed Funds rate dropped by 20bp to 5.48% for the September 2023 meeting. All eyes are on the NFP and AHE YoY data points today which are expected to come at 225k and 4.7% respectively. US IG and HY CDS spreads widened by 4.4bp and 24bp respectively. The S&P and Nasdaq dropped sharply by 1.9% and 2.1% respectively.

European equity markets ended slightly lower. European main CDS spreads were flat while crossover CDS spread widened 0.9bp. Asian equity markets have opened in the red today, taking cues from global equities. Asia ex-Japan CDS spreads widened by 3.1bp.

-1.png)

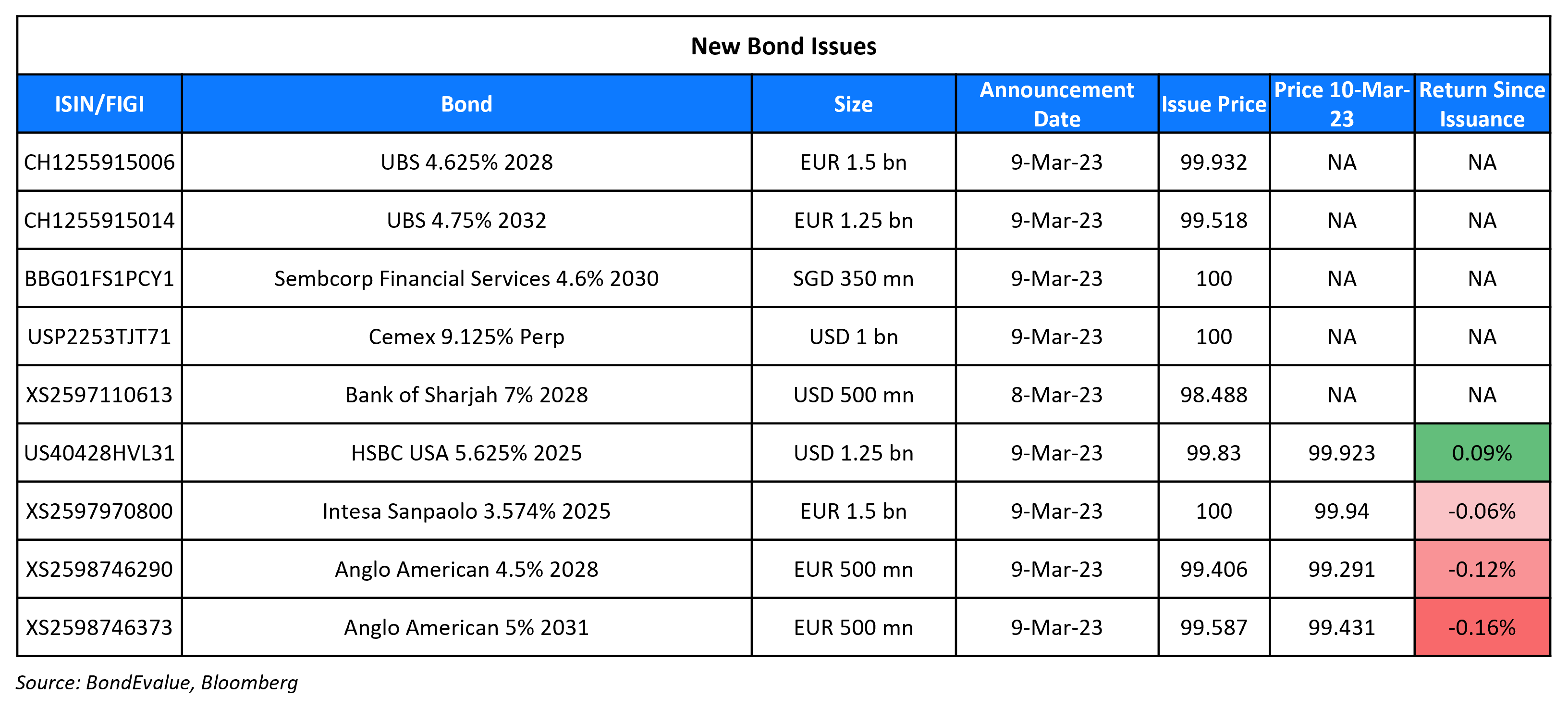

New Bond Issues

HSBC USA raised $1.25bn via a 2Y bond at a yield of 5.716%, 20bp inside initial guidance of T+100bp area. The senior unsecured bonds have expected ratings of A1/A-/A+. Proceeds will be used for general corporate purposes. The new bonds are priced in-line with its existing 4.25% 2025s that yield 5.74%. With this deal, HSBC has issued a combined ~$15bn across 3 currencies in under two weeks.

Cemex raised $1bn via a PerpNC5.25 green bond at a yield of 9.125%, in-line with initial guidance of low-mid 9% area. The senior subordinated bonds have expected ratings of B+/BB-. Proceeds will be used to (re)finance eligible new and existing green projects. The new bonds are priced a massive 95.5bp wider to its existing 5.125% Perps (callable in 2026) that yield 8.17%.

UBS raised €2.75bn via a two-tranche deal. It raised

- €1.5bn via a 5NC4 bond at a yield of 4.644%, 25bp inside initial guidance of MS+140bp area. The bonds received orders over €3.6bn, 2.4x issue size. If not called on 17 March 2027, the current fixed coupon of 4.625% will be reset to 1Y MS+115bp.

- €1.25bn via a 9NC8 bond at a yield of 4.824%, 20bp inside initial guidance of MS+180bp area. The bonds received orders over €3.4bn, 2.7x issue size. If not called on 17 March 2031, the current fixed coupon of 4.75% will be reset to 1Y MS+160bp. The new bonds are priced 18.4bp wider to its existing 4.375% 2031s (callable in 2030) that yield 4.64%.

The senior unsecured bonds have expected ratings of A-/A+.

Sembcorp raised S$350mn via a 7Y Green bond at a yield of 4.6%, 20bp inside initial guidance of 4.8% area. As is the case with many SGD bond issuances, both the senior unsecured bonds and their issuer are unrated. While no distribution data was released, the issuer said in an SGX statement that Clifford Capital had subscribed to a portion of the notes. Proceeds will be used to (re)finance eligible new and existing green projects. The bonds are issued by Sembcorp Financial Services Pte Ltd and guaranteed by Sembcorp Industries Ltd. The new bonds are priced 25bp wider to its existing 3.735% 2029 SLBs that yield 4.35%.

Bank of Sharjah raised $500mn via a 5Y bond at a yield of 7.367%, in-line with initial guidance of T+Low 300bp area. The senior unsecured bonds have expected ratings of BBB+, and received orders over $1bn, 2x issue size. The bonds are issued by BoS Funding Limited and guaranteed by Bank of Sharjah. The deal is the second issuance from the gulf in two weeks, following Islamic Development Bank’s $2bn 5Y Sukuk that was priced on Tuesday.

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

Term of the Day: Risk-off

Risk-off is an indication of global market sentiment wherein investors switch out from risky assets (i.e. risk-off) into safer assets on the back of increased uncertainty. This can be due to geopolitical risk, poor economic data or a crisis. Most typically, during a risk-off environment, US Treasuries and gold tend to perform better as they are considered safe haven assets. On the other hand, risk-on indicates positive investor sentiment wherein investors switch into risky assets (i.e. risk-on) from safer assets on improved prospects of economic growth. This can be due to improved political environment, strong economic data, strong corporate earnings, or a recovery from a crisis.

Talking Heads

On Frontier countries to suffer most if Fed rate gets to 6% – analysts

Satyam Panday, chief emerging markets economist at S&P

“The current repricing risk in the Fed’s terminal fed funds rate to perhaps 6% in a short period of time is in the context of (the) response to inflation running stubbornly well-above target in a weakening global GDP growth environment… This mix is generally a net negative for emerging markets”

UBS strategist Manik Narain

“Fed tightening towards 6% would firmly test historical ‘pain thresholds’ for emerging market assets”

Barclays

A 50bp Fed rate hike would increase interest rate volatility, which “would be more destabilizing initially, as it typically comes with EM FX underperformance, which could trigger a further leg up in EM rates.”

On Treasuries Surging as Bond Bulls Seize on Bank Fears, Jobless Data

Kellie Wood, a fixed-income money manager at Schroders

“The jump in jobless claims was just what bond bulls were looking for because it’s got a long track record of being the best leading indicator for the labor market… I would much rather be buying high quality assets at 5-5.5% than equities at about 6%”

On Bank stocks cratering as SVB’s woes send warning sign

Keefe, Bruyette & Woods

“The Silicon Valley raise got everybody nervous about people’s capital levels and what deposits are doing. A lot of institutional investors don’t feel great about owning certain banks right now”

Morgan Stanley analysts

“Higher-for-longer rates also mean that these sweep accounts will be a bigger drag on NIM… Additionally, the $15 bil increase in long-term debt will also push funding costs higher”

Arnold Kakuda, Bloomberg Intelligence bank debt analyst

“The question is who is next. That is the fear”.

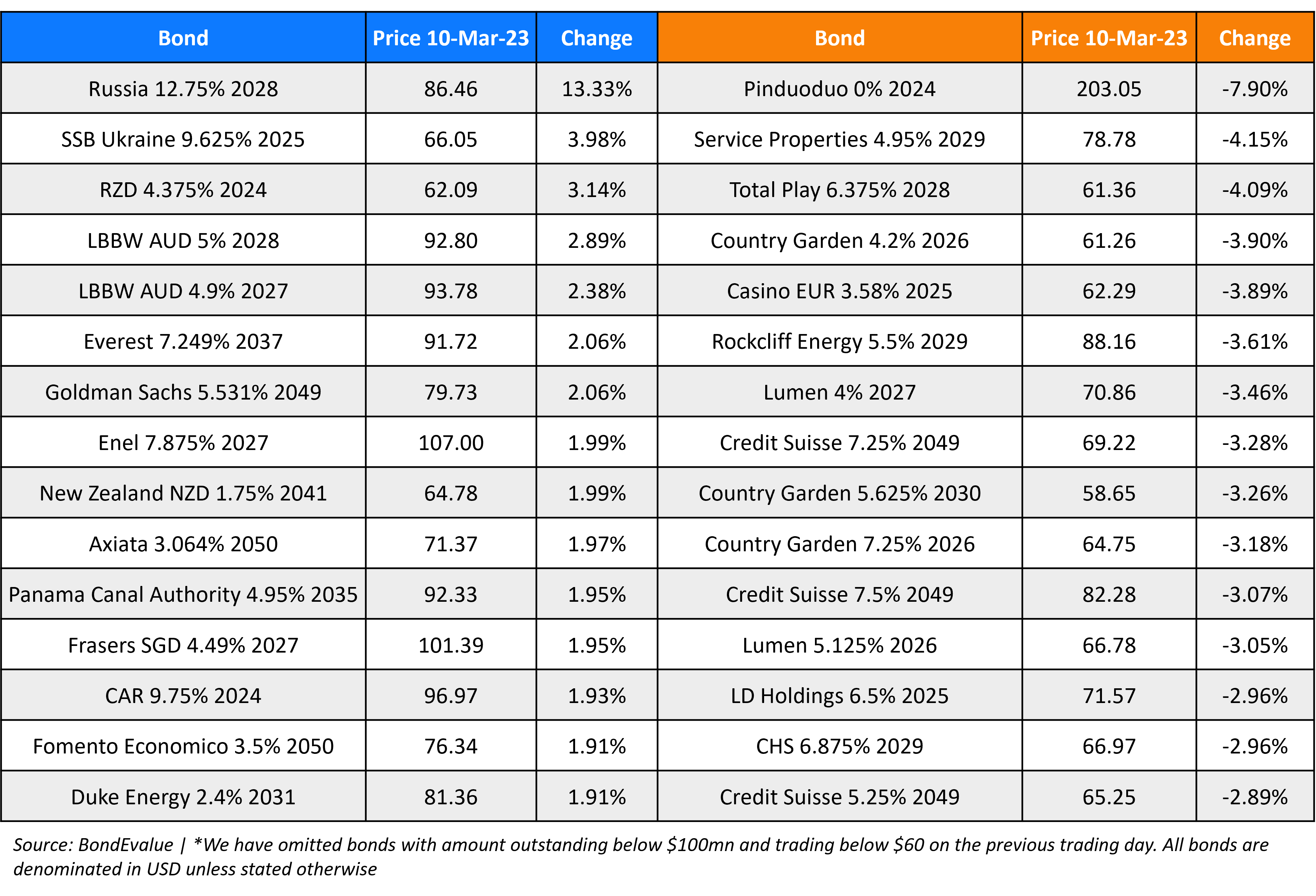

Top Gainers & Losers – 10-March-23*

Go back to Latest bond Market News

Related Posts:

NWD’s China Unit Planning $732mn Project in Guangzhou

August 26, 2021

SBI Reports 62% Quarterly Profit Jump

February 7, 2022

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.