This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Times, Powerlong, Wens Food Launch $ Bonds; Oman Raises $2bn via Bonds; Tesla Reports Record Operating Income

October 22, 2020

S&P ended marginally lower by 0.2%. Energy and industrials were down over 1% while communication services were up 1%. Intel, American Airlines and Coca Cola are scheduled to report earnings amongst others. US stimulus hopes are mixed for a last minute deal by the end of the week with US 10Y and 30Y Treasury yields near four-month highs of 0.81% and 1.61%. US IG CDS spreads were tighter by 0.7bp while HY was flat. European equities were down by ~1.5% attributing to increased Covid cases, though European IG CDS spreads were flat and Crossover CDS spreads narrowed 3bp. Asian equities are down over 1% today while Asia ex-Japan CDS spreads were flat. New deals continue to flood the primary markets with six new deals launched today.

New Bond Issues

- Times China $ tap 6.75% 2025 @ 6.35% area

- Powerlong Real Estate $ 200 mn 4.5NC2.5 @ 6.5% area

- Straits Trading S$ 5yr @ 4% area

- Wens Foodstuff $ 5/10yr @ T+225/270bp area

- Wuhan Dangdai Science and Technology $ tap 10.5% 2023 final @ 8.75%

- Jiaxing City Investment $ 3yr @ 3% area

.png?width=1200&upscale=true&name=New%20Bond%20Issues%2022%20Oct%20(1).png)

Meituan, the Chinese online food delivery services provider listed in Hong Kong (market cap of $201.5bn) raised $2bn from a debut dollar bond offering. It raised $750mn via a 5Y bond at a yield of 2.151%, 180bp over Treasuries and 50bp inside guidance of T+230bp area. It also raised $1.25bn via a 10Y bond to yield 3.066%, 225bp over Treasuries and 50bp inside initial guidance of T+275bp area. The bonds were rated Baa3/BBB-/BBB. The proceeds from the bond issue will primarily be used for general corporate purposes and refinancing.

Sinochem raised $1bn from a dual tranche bond. It raised $500mn via a 5Y bond to yield 1.647%, 130bp above Treasuries and 40bp inside guidance of T + 170bp area. It also raised $500mn via a Perpetual non-call 3Y (PerpNC3) bond at a yield of 3%, 30bp inside guidance of 3.3% area. The 5Y bonds have ratings of A3/A-/A while the perpetual has ratings of Baa1/BBB+. The perpetual has a coupon reset on the first call date and every three years thereafter at the then prevailing Treasury yield plus the initial spread with a 300bp step-up. It also has a dividend pusher and a stopper. The bonds received orders of over $2.5bn, 2.5x issue size. Sinochem Offshore Capital Co is the issuer of both bonds with Sinochem Hong Kong (Group) Co as the guarantor. Sinochem Group is providing a letter of support for the dual-trancher. The company plans to use proceeds for offshore debt refinancing.

Arab National Bank raised 750mn via 10Y non-call 5Y (10NC5) tier 2 sukuk to yield 3.326%, 290bp over Mid-Swaps and 35bp inside initial guidance of MS+325bp area. The bonds have expected ratings of Baa3/BBB–. ANB Sukuk is the issuer of the bonds and Arab National Bank is the obligor.

Investment Corporation of Dubai (ICD) raised $600mn via 5Y bonds to yield 3.223%, 275bp over Mid-Swaps and 25bp inside initial guidance of MS+300bp area. ICD Funding is the issuer and Investment Corporation of Dubai is the guarantor.

KB Capital, a consumer finance subsidiary of Korea’s KB Financial Group raised $300mn via 5Y bonds to yield 1.557%, 120bp over Treasuries and 30bp inside initial guidance of T+150bp area. The bonds received final orders over $1.125bn, 3.75x issue size.

China SCE Group Holdings raised $500mn via a 4.5Y non-call 2.5Y (4.5NC2.5) bond at a yield of 7%, 40bp inside guidance of 7.4% area. The bond has a rating of B2 by Moody’s and received orders over $2.2bn, 4.4x issue size. The company plans to use proceeds for offshore debt refinancing.

Greentown China Holdings raised $300mn via a 4.5Y non-call 2.5Y bond at a yield of 4.7%, 50bp inside initial guidance of 5.2% area. The bonds are expected to be rated Ba3 and received strong demand from investors with orders of over $2.8bn, 9.3x issue size. Proceeds will be used to refinance debt due within 12 months. The new 2025s rose 0.25 points on the secondary markets, now yielding 7bp tighter than its older 5.65% bonds due July 2025.

China’s Zhongliang Holdings Group raised $200mn via a 1.75Y bond at a yield of 10.125%, 37.5bp inside initial guidance of 10.5% area. The bonds, rated B+ received total orders of $1.4bn, 7x issue size. Proceeds from the issuance will be used for refinancing purposes.

New Bonds Pipeline

- Lenovo rated $ Bond

- Korea Land & Housing $ Bond

- Gansu Provinial Highway Aviation Tourism Investment Group $ Bond

Rating Changes

Fitch Upgrades Solocal to ‘CCC+’ on Completion of Debt Exchange

Moody’s upgrades Garfunkelux’s senior secured debt rating to B2, outlook stable

Fitch Downgrades Findep’s Ratings to ‘BB-‘; Removes Negative Watch; Assigns Negative Outlook

Fitch Downgrades Metro’s and EFE’s Foreign Currency IDR to ‘A-‘

Moody’s downgrades the long-term deposit and debt ratings of ICICI Bank UK PLC

Concho Resources Inc. Ratings Placed On CreditWatch Positive By S&P On Acquisition By ConocoPhillips

Moody’s affirms Banco Nacional de Panama’s ratings; changes outlook to negative

Moody’s places Crown Resort’s ratings on review for downgrade

Fitch Affirms Beijing Capital Group at ‘BBB’; Keepwell Bond on RWN

Oman Raises $2 Billion via Dual-Tranche Bond

Oman raised $2bn via a dual-tranche bond priced on Wednesday. It raised:

- $1.25bn via 7Y bonds to yield 6.75%, 25bp inside initial guidance of 7% area

- $750mn via 12Y bonds to yield 7.375%, 25bp inside initial guidance of 7.625% area

The new bonds are rated Ba3/B+/BB-. The bond offering drew combined final orders of over $3.4bn, 1.7x issue size. Earlier, sources mentioned that Oman was also planning to issue a 3Y tranche with a combined triple-tranche size of $3bn-$4bn but scrapped the plan. The new 2027s offer a new issue premium of 15bp over the older 5.625% bond due January 2028, which are currently yielding 6.6% on the secondary markets. This is Oman’s first dollar bond issue since July 2019 as the gulf nation faces a challenging economic environment given low oil prices and the economic impact of the pandemic. As per a bond prospectus seen by Reuters, the country has begun talks with other gulf nations for financial support, similar to Bahrain’s $10bn bailout by its wealthy Gulf neighbors in 2018. “If Oman had the kind of explicit Gulf support that Bahrain has, it may have saved 35 bps in new issuance premium on the seven-year tranche,” a fixed income strategist said after the initial price guidance of 7% area. was announced.

In the graph below, we have plotted all of Oman’s (Ba3/B+/BB-) and Bahrain’s (B2/B+/B+) outstanding dollar bonds to compare yields of the two GCC sovereigns.

For the full story, click here

Gulf Debt Issuance Volumes at a Record High

Debt issuance from GCC countries and corporates have hit an annual record with issuance volume of $103.5bn thus far, with two months remaining in the year. This includes the recent $2bn Oman bond, $750mn Qatar Islamic Bank sukuk and $600mn Investment Corporation of Dubai (ICD) issuance. Lower oil prices coupled with the economic impact of the pandemic has hurt many sovereigns. The IMF is forecasting Oman’s economy to de-grow by 10% in 2020, the most hit among GCC countries. “The last window of opportunity before the presidential contest between Donald Trump and Joe Biden is galvanizing issuers”, said Sergey Dergachev, a money manager. Some analysts say that a Biden led government would see better relations overall for UAE and Saudi Arabia. The chart below shows the annual debt issuance volume from GCC issuers since 2009.

For the full story, click here

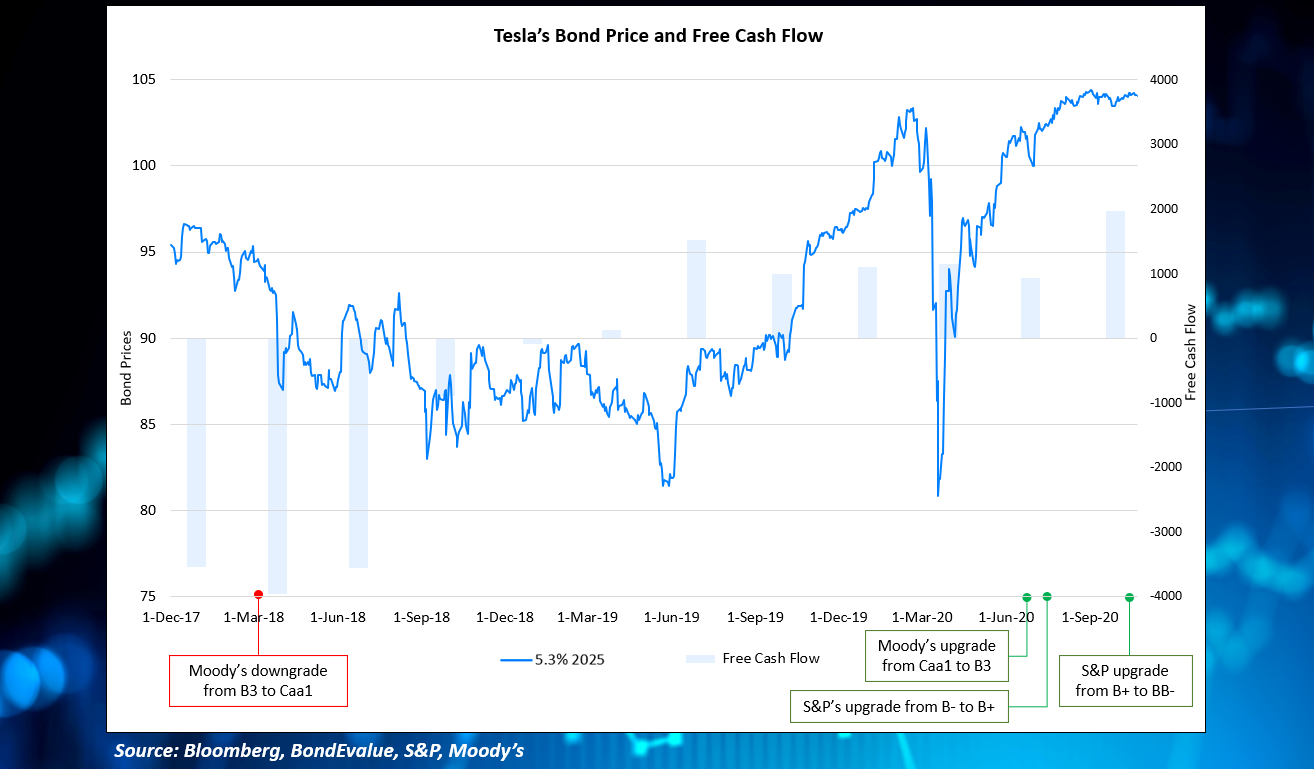

Tesla Records Its Highest Operating Income Despite Pandemic Slowdown

Tesla reported strengthening of its sales despite a pandemic-driven slowdown in the automotive sector. In its Q3 earnings report, the electric car company reported a total revenue growth of 39% YoY and 45% QoQ to ~$8.77bn on the back of robust demand for its vehicles. The automotive revenues grew at 42%YoY and 47% QoQ to $7.61 bn. The company reported a YoY growth of 51% in its total production of Model S/X and 3/Y at 145,036 while deliveries increased 44% YoY to 139,593. Profits soared due to increased vehicle deliveries despite a slight decline in the average selling price (ASP). The company’s operating income improved to a record level of $809mn, resulting in a 9.2% operating margin in Q3.

Tesla continues to expand and is on track to have three new factories on three continents. The company already has an installed capacity to produce and deliver 500,000 vehicles this year and aims to deliver that number of vehicles in 2020. The product mix is seen shifting from Model S and Model X to the more affordable Model 3 and Model Y. The company is also targeting the premium segment aggressively, which was evident in its pricing of Model 3 at RMB 249,900 (~$37,500) after incentives, making it the lowest-price premium mid-sized sedan in China, as per the company. The company has been growing even during the pandemic. It was upgraded by Moody’s to B2 and by S&P to B+ in July. S&P had again upgraded the car maker to BB- earlier this month.

Tesla’s 5.3% bonds due 2024 have been trending higher since March lows of ~81 and are currently stable at 104, given that the bonds are callable on November 18 at 104. Given its strong operational and financial performance. Tesla is likely to redeem the bonds and refinance at a lower cost. The chart below shows how Tesla’s bond price has trended relative to the free cash flows of the company.

For the full story, click here

Fitch Places Beijing Capital’s Keepwell Bond on Negative Watch

Beijing Capital Group’s (BCG) issuer rating was affirmed at BBB by Fitch while the $250mn keepwell bond due September 2021 was kept on RWN (Rating Watch Negative). The issuer of the keepwell bond was Capital Environment Holdings Ltd. (CEHL) with BCG as the parent. The stance on the keepwell comes after administrators did not recognize Peking University Founder Group’s (PUFG) keepwell dollar bonds. This led PUFG’s bondholders to take legal action for more protection on their keepwell bonds. Fitch noted that CEHL’s issuer default rating may be derived from their change in approach of parent-subsidiary linkages, which may potentially lead to a downgrade of the bond. They added that a downgrade would not be due to deterioration of the issuer or the keepwell provider’s credit profile. CEHL’s 5.625% bonds due September 2021 were flat at 102.21, yielding 3.07% and Beijing Capital’s 4.25% dollar bonds due March 2021 were 2 cents lower at 100.88, yielding 2.1% on the secondary markets.

For the full story, click here

Court Orders Argentina’s YPF to Pay $231 Million For Breach of Export Contract

An Argentine court has ordered Argentina’s state oil company YPF to pay $231mn in addition to the interest and the legal costs to Transportadora de Gas del Norte (TGN) in a breach of an export contract lawsuit. TGN operates a pipeline network of more than 6,000 kilometers and had filed a lawsuit against the oil major accusing it of non-compliance to the export contract. The court partially accepted the allegations by TGN and ruled that YPF needs to pay bills for services provided between February 2007 and December 2010. YPF defended itself by stating the “impossibility of compliance” under the terms of the agreement due to emergency regulations issued under the Cristina Fernández de Kirchner administration that made it impossible to continue exporting gas.

Meanwhile, Belgium’s Exmar has also settled a dispute with YPF over the floating liquefaction vessel Tango FLNG and has received $22mn out of a total of $150mn to be paid over next 18 months. YPF had declared force majeure on the contract in June due to the Covid-19 pandemic that had hindered its ability to perform its obligations under the agreements.

YPF’s bonds were in the red on Wednesday. Its 6.95% bonds due 2027 and 8.5% bonds due 2029 were down 1.13 and 0.5 points respectively and were trading at 62.4 and 60.8 cents on the dollar respectively.

For the full story, click here

Term of the Day

Orphan SPV

An orphan special purpose vehicle (SPV) is a type of corporate structure commonly used for securitization transactions. In an orphan structure, the equity of the SPV is held in a trust that is not legally related to the main sponsor or its subsidiaries.

This can be explained with India Green Energy’s new dollar bond priced on Wednesday. In this structure, India Green Energy is the orphan SPV, whose equity is held by a trust that is not linked to ReNew Power (the sponsor) or its subsidiaries. Here, India Green Energy will use proceeds from the dollar bond to subscribe to senior local currency (INR) debt issued by a pool of 11 ReNew Power subsidiaries.

Talking Heads

On China likely to see positive economic growth for 2020 – Yi Gang, PBOC Governor

The macro leverage ratio — the percentage of debt in households, non-financial enterprises and governments to total gross domestic product — “has increased this year due to the fight against the pandemic,” said Yi. “It will become more stable after GDP growth picks up next year.” The ratio needed to be maintained on “a reasonable track,” he added.

Monetary policy should “neither let the market be short of liquidity nor lead to excessive supply,” he said. The governor also repeated recent comments that China wants to implement “normal monetary policy” for as long as possible.

On Federal Reserve standing by to control interest rates amid Treasury debt sale

Esty Dwek, head of global market strategy, Natixis Investment Managers.

“Yields are almost behaving as if we have yield-curve control already,” said Dwek.“The yield rise will probably remain contained because the Fed is more important than anything else and they will limit it.”

Jim Caron, head of global macro strategies at Morgan Stanley Investment Management

“Interest rates are going to be low for an extended time, so that means a limited backup in rates,” he said. “We still own Treasuries and would be happy to buy more if rates rise and overshoot our upside expectations.”

Alex Etra, a senior strategist Exante Data who formerly worked at the New York Fed

“If the U.S. recovers more quickly on the back of robust fiscal stimulus, and presumably a vaccine, we could see a move up in yields,” said Etra. “But if you got a really rapid ramp-up that was at risk of derailing the recovery, that’s certainly a case where the Fed would step in,” he said. “That’s not exactly yield-curve control, but it clearly is intended to reduce the probability that long-term yields rise,” he said.

Zoltan Pozsar, Credit Suisse Group AG.

“There are two policeman that will keep long-end Treasury yields from moving too high: the Fed and the foreign buyers, which can obtain cheap currency hedges through the Fed’s swap lines,” Pozsar said. “It’s Fed policing ultimately, either way.”

“This is an inflection point in the sense that stimulus is coming. It’s not if, it’s when, and we’re getting closer to the point of I think no matter who wins the presidency you’re going to get fiscal stimulus,” said Caron. “It’s just a matter of how much and what the process is. It would not be unreasonable to think the 10-year yield could get between 1% and 1.25% over the next few quarters,” said Caron.

“2021 was supposed to be a turn around year from 2020,” Caron said. “We already have a lot of stimulus in the system. To add more to it at a time when we are already expecting a recovery is, in the future, something that could push yields higher. There’s also a limit as to how high yields can go. I don’t think this is the start of a ‘taper tantrum.’”

On China’s US dollar debt market showing cracks from US sanctions and prospect of more

Vivien Gui, who is in charge of fixed income investment at Wu Capital

“If the US decides to block top Chinese corporates from dollar financings, then everyone will simply have to stop trading their bonds the very next day,” said Gui. “China hasn’t reached this kind of stage yet, but some traders are already asking what would be the point of buying some corporate bonds now?”

Hua Cheng, research analyst for corporate credit at AllianceBernstein

“Because US-China tensions may escalate in the run-up to the US elections on November 3, we think caution is warranted,” Hua said. “The US regards China’s [state firms] with suspicion because of apparent links some have to the Chinese military.”

Johanna Chua, head of Asia-Pacific economics and market analysis at Citigroup Global Markets Asia

“The question is whether central bank intervention is delaying loan losses and balance sheet pressures on the private sector,” Chua said. “Restructuring may, at some point, have to be part of the solution, once debt continues to go to a point of no return,” she said.

Sophia Xia, co-head of China restructuring at Houlihan Lokey

“I think the government realises that it is no longer able to sustain economic growth by issuing more debt,” Xia said. “If you think your company’s fundamentals can no longer withstand a high leverage ratio, then that is like a tumour. If the tumour expands, then you should have surgery. Actually, a default is not that scary.”

On ECB’s calls for tougher action on climate change and more accountability

Wolfgang Kuhn, Shareaction

“We believe the ECB’s credibility is at stake,” he said. “Not from the people who watch 5-year forward inflation swaps or bet on harmonised consumer price indexes, but from the people who see the value of their money erode from years of inflation-fighting.”

Philip Lane, ECB Chief economist

“We know the absence of price stability is damaging,” Mr Lane said. “The sweet spot we think is low inflation, but with a significant enough buffer above zero that we do make sure we don’t fall into deflation.”

Top Gainers & Losers – 22-Oct-20*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.