This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

The Week That Was

July 12, 2021

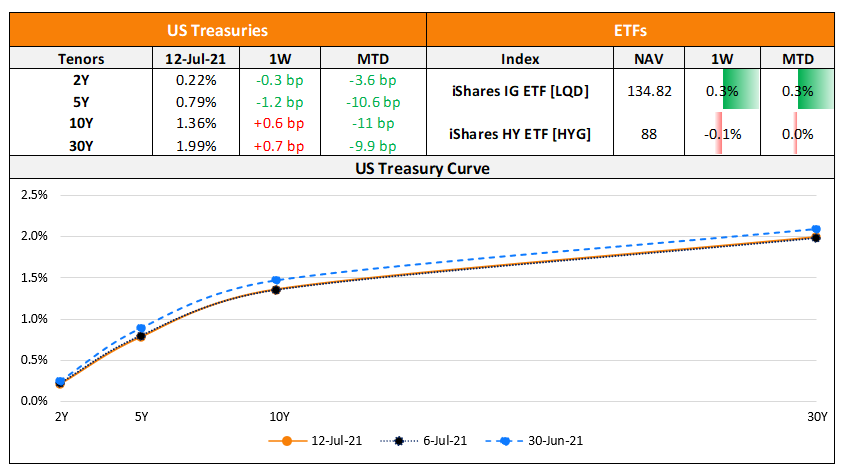

US primary market issuances dropped to just $2.3bn vs. $13.2bn in the week prior on the back of the July 4th holiday and an overall risk-off sentiment. This is the lowest issuance for the same weekly period since 2009. IG issuances fell last week to a mere $1.7bn vs. $9.6bn in the prior week and HY issuances were also lower to just $375mn vs. $3.1bn in the prior week. The IG space saw only three deals – PacificCorp’s $1bn deal followed by Equitable Financial Life’s $500mn and Affiliated Managers’ $200mn issuances. In the HY space, there was only one deal, Masonite International’s $375mn issuance. In North America, there were a total of 24 upgrades and 12 downgrades combined across the three major rating agencies last week. LatAm saw $711mn vs. $3.5bn in issuances in the prior week. Issuances were led by Minerva’s $400mn and Pan American Energy’s $280mn issuances. EU Corporate G3 issuances were slightly higher at $23.2bn vs. $17.3bn in the week prior – KfW’s $4.24bn issuance led the table followed by Cie de Financement Foncier’s €1.5bn ($1.8bn) and Enel’s $900mn issuances. Across the European region, there were 20 upgrades and 11 downgrades across the three major rating agencies. Overall, GCC and Sukuk G3 issuances fell to $1.7bn vs. $13.6bn in the week prior led by Sharjah’s $740mn and Dukhan Bank’s $500mn Sukuk issuances besides QNB’s $400mn issuance. Across the Middle East/Africa region, there were no upgrades and 4 downgrades across the three major rating agencies. APAC ex-Japan G3 issuances rose ~40% to $14bn vs. $10.25bn in the prior week – Prosus NV’s ~$3.7bn multi-currency issuance led the table, followed by Xiaomi’s $1.2bn dual-trancher, Pakistan’s $1bn three-trancher tap and Westpac NZ’s €750mn ($886mn) deal. In the Asia ex-Japan region, there was 1 upgrade and 4 downgrades combined across the three major rating agencies last week.

Go back to Latest bond Market News

Related Posts:

1, 2, 3, 4th Fed Hike!

June 14, 2017

Fed’s Dudley Shakes Up Complacent Markets

June 20, 2017

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.