We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Temasek Launches S$ 50Y; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

August 10, 2021

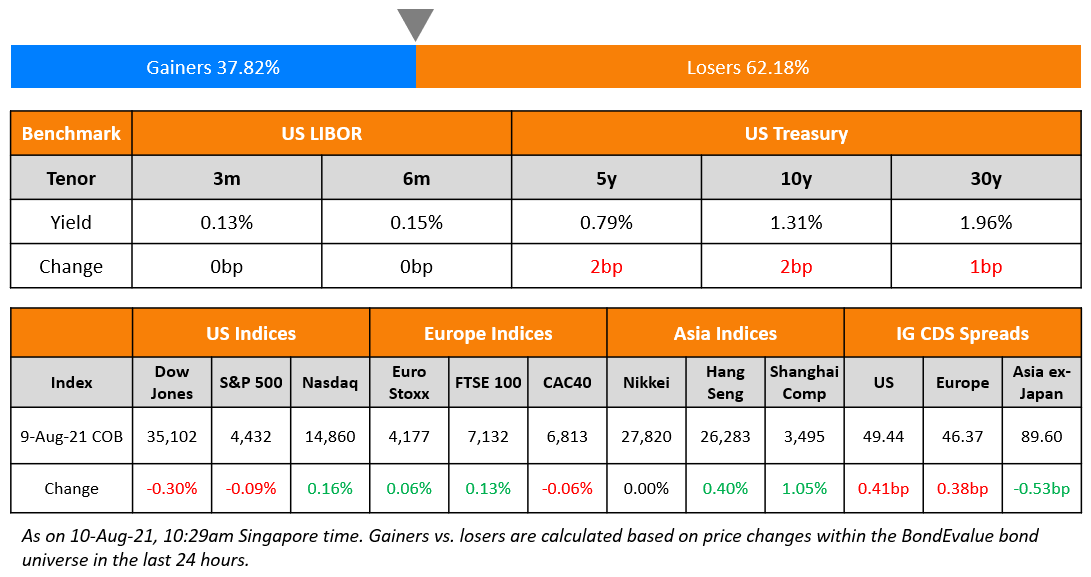

US markets closed mixed even as the number of US job openings expanded – the S&P fell 0.1% from its record while Nasdaq inched up 0.2%. Healthcare, Consumer Staples and Financials, up ~0.3% provided support to the bourses while Energy down 1.5% and Real Estate, Industrials and IT down ~0.4% dragged the indices lower. European markets continued to hover close to records – the FTSE was up 0.1% while CAC and DAX were down ~0.1%. Saudi’s TASI closed 0.2% lower while UAE’s ADX was up 1%. Brazil’s Bovespa gained 0.2%. APAC stocks had a soft start on concerns over the spread of the Delta variant – Singapore’s STI, Nikkei and HSI were 0.2-0.6% while Shanghai is down 0.2%. US 10Y Treasury yields gained 1bp to 1.31%. US IG CDS spreads widened 0.4bp and HY widened 3.3bp. EU Main CDS spreads widened 0.4bp and Crossover spreads tightened bp. Asia ex-Japan CDS spreads were 0.5bp tighter.

The U.S. Bureau of Labor Statistics in its monthly Job Openings and Labor Turnover Survey (JOLTS) reported that the number of job openings increased to a series high of 10.1mn on the last business day of June vs. 9.48mn in the previous month while hires rose to 6.7mn. US Senators also voted 68-29 to set up a final vote for the $1tn infrastructure package. Eurozone Sentix investor confidence was reported at 22.2 against expectation of 29 and vs. 29.8 last month. The UAE Central Bank maintained the base rate at 15bp while Saudi Aramco (details below) beat earning expectation.

%20(1).jpg?width=1400&upscale=true&name=CapbridgeBonds_Newsletter%20(1)%20(1).jpg)

With CapBridge’s fully digital investment platform, it’s fast and easy to get started.

- Hassle-free onboarding in 3 simple steps: SingPass MyInfo onboarding available for Singapore residents

- Curated list of fractional bonds

- Yields of up to 7-9%

- Fully transparent fee structure

- Instant settlement

For a limited time, investors get to enjoy up to 50% rebate off annual fees. Now, enjoy an even lower cost of bond ownership.

New Bond Issues

- Temasek markets S$ 50Y bonds at 2.85% area

- Goho Asset Management tap of $ 8.5% June 2023s final at 8.5%

-

Taiyuan Longcheng Development Investment Group capped $77mn 364-day notes at 2.75% area

- Shangrao Innovation Development $ 35-month credit-enhanced bonds final at 4%

Bombardier raised $750mn via a 6.5 non-call 2.5Y (6.5NC2.5) bond at a yield of 6%, unchanged from initial guidance of 6% area. The bonds have expected ratings of Caa1/CCC. Proceeds will be used to redeem their 6% Senior Notes due 2022 and 6.125% Senior Notes due 2023.

New Bonds Pipeline

- Perusahaan Pengelola Asset hires for $ bond

-

Zhuhai Huafa Group hires for $ senior perp

-

Sichuan Development Holding hires for $ bonds; calls today

-

PCGI Holdings hires for $ 5NC3 bond; calls today

- HDFC Bank hires for $ AT1 Bond

Rating Changes

-

Moody’s upgrades Bombardier’s CFR to Caa1 and assigns Caa1 to new notes; outlook stable

-

Moody’s upgrades ArcelorMittal’s ratings to Baa3; stable outlook

- E-House Downgraded To ‘B+’ By S&P On Expected Negative Operating Cash Flow; Outlook Stable

- CITIC Group And CITIC Ltd. Outlook Revised To Positive By S&P On Bank’s Improving Capitalization; ‘BBB+’ Ratings Affirmed

- Bombardier Inc. Outlook To Stable From Negative By S&P On Lowered Refinancing Risk; ‘CCC+’ ICR Affirmed; US$750M Notes Rated

- CAPEX S.A.’s Stand-Alone Credit Profile Revised Up To ‘b-‘ From ‘ccc+’ By S&P On Stronger Cash Flows, ‘CCC+’ Ratings Affirmed

Term of the Day

Bid-to-Cover

Bid-to-cover is a ratio of the number of bids or orders received for a particular security issuance vs. the amount issued. The bid-to-cover ratio indicates the demand for an issuance – higher the ratio, higher the demand and vice versa. Last week, Ping An Insurance Overseas raised $550mn via a 10Y bond that drew orders over $2.9bn, with a bid-to-cover of 5.3x.

Talking Heads

“I would expect if we continue to have (jobs) reports like we’ve had over the last two, with very substantial payroll employment gains, that by the September meeting, we would, in my view, meet the substantial further progress criteria, and that would imply starting to taper sometime this fall,” Rosengren said. “If you continue to purchase assets, the reaction primarily is in pricing, not so much in employment.” “I don’t think asset purchases are having the desired impact on really promoting employment.”

Raphael Bostic, Federal Reserve Bank of Atlanta President

“We are well on the road to substantial progress toward our goal,” Bostic said. “My sense is if we are able to continue this for the next month or two I think we would have made the ‘substantial progress’ toward the goal and should be thinking about what our new policy position should be.” “I am in favor of going relatively fast,” Bostic said. “The economy is in a much different place today” and “I am pretty confident these markets are going to continue to function even with a more rapid withdrawal, and I would be willing to lean into that to try to get us to complete the taper in a shorter period than what we have done in previous rounds.” “The 10-year has been somewhat volatile over the last several months and it would not surprise me if those numbers return to some of the levels that they were at earlier in the summer.”

Thomas Barkin, Richmond Fed President

“I think it is fair to say on the price side we made substantial progress, maybe more than substantial progress,” Barkin said. “I believe there is still more room to run in the labor market.”

“I think the tailwinds to euro zone government bonds are still pretty strong … So we should get another week or two of rally before supply kicks in in September.”

On limited contagion risk from Evergrande – According to Goldman Sachs analysts led by Kenneth Ho

“Whilst there are considerable amounts of uncertainty, our analysis suggest that it is possible for recovery in a potential restructuring scenario to be close to current market pricing. And if the onshore operations for Hengda Real Estate can continue, we believe that a more negative outcome can be avoided. Therefore, despite our expectation that market conditions will continue to be volatile, we believe that contagion risk may be contained.”

Top Gainers & Losers – 10-Aug-21*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.