This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Santander Prices $2.5bn Dollar AT1 Bonds at 9.625%

November 17, 2023

Santander raised $2.5bn via a two-tranche AT1 deal.

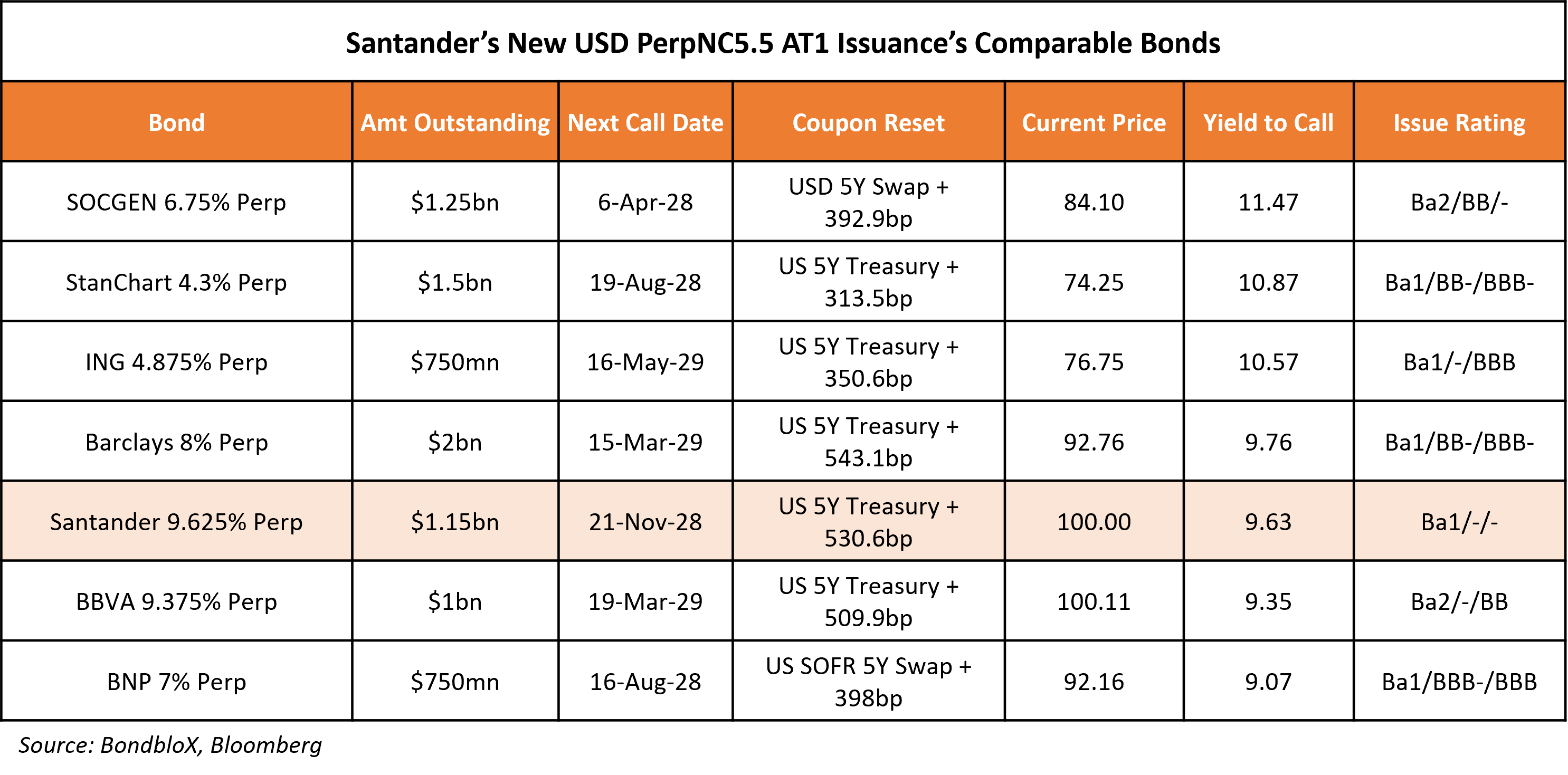

– It raised $1.15bn via a PerpNC5.5 bond at a yield of 9.625%, 37.5bp inside initial guidance of 10% area. If uncalled between the first call date of November 2028 and the reset date of May 2029, the coupons will reset on May 2029 and every five years thereafter at the US 5Y Treasury yield plus a spread of 530.6bps. The table below compares Santander’s new AT1s with other similarly rated dollar denominated European bank AT1s.

– It also raised $1.35bn via a PerpNC10 AT1 bond at a yield of 9.625%, 37.5bp inside initial guidance of 10% area. If uncalled on the first call date of November 2033, it will reset then and every five years thereafter at the US 5Y Treasury yield plus a spread of 529.8bps. The new notes are priced 100.5bp wider to UBS’ recently issued and slightly higher rated (Baa3/BB/BBB-) 9.25% Perps, callable in 2033, that yield 8.62%.

The subordinated bonds have expected ratings of Ba1 (Moody’s). For the newly issued AT1s, a trigger event would occur when the CET1 ratio of the issuer falls below 5.125%. Santander’s current CET1 ratio stands at 12.3%. If a trigger event occurs, the bonds may be converted into common shares of the issuer at the higher of (i) the current market price of the common share, converted into USD (ii) the floor price set at $2.57/share, or (iii) the nominal value of a common share at the time of conversion, converted into USD. The bonds have a 75% clean-up call. Proceeds will be used for general corporate purposes, including managing the potential refinancing of existing capital securities.

Go back to Latest bond Market News

Related Posts:

Banco Santander and UBS Report Solid Results

February 3, 2022

Bank AT1 Perps Slip Following SVB Collapse

March 14, 2023

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.