This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

REC & Aoyuan Launch $ Bonds; Macro; Rating Changes; New Bond Issues; Talking Heads; Top Gainers & Losers

February 22, 2021

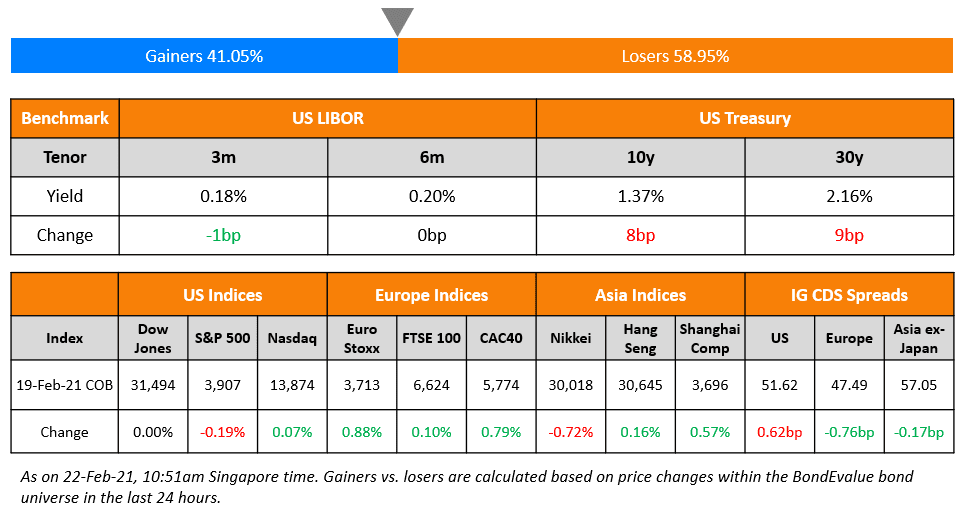

S&P and Nasdaq ended almost flat on Friday after a slight positive start at the open. European indices were higher ~0.8% with FTSE underperforming. US 10Y Treasury and Bund yields climbed further by 8bp and 4bp 1.37% and -0.30% respectively. The US 2s10s curve has steepened ~31bp since end-January led by the sell-off in long-dated bonds. Eurozone’s preliminary PMI numbers came in at 57.7, a three year high as sentiment was upbeat. US IG CDS spreads were 0.6bp wider and HY was 2.8bp wider. EU main CDS spreads tightened 0.8bp and crossover spreads tightened 3.2bp. Asian issuers have slowly returned to the primaries with China Aoyuan and REC launching new deals this morning. Asian equity markets have opened ~0.7% higher while Asia ex-Japan CDS spreads are 0.2bp tighter.

Navigating The Bond Markets by Leveraging the BEV App

New to the BEV App? BondEvalue will be conducting a complimentary session on Navigating The Bond Markets by Leveraging the BEV App this Wednesday, February 24. This session is aimed at helping bond investors in tracking their investments using the BondEvalue App.

New Bond Issues

- China Aoyuan $ 6NC4 at 6.2% area; books over $1.1bn

- REC $ 5.5Y at T+205bp area

French banking major BNP Paribas raised $1.25bn via a Perpetual non-call 10Y (PerpNC10) bond priced last Friday at a yield of 4.625%, a strong 50bp inside initial guidance of 5.125% area. The AT1 bonds have expected ratings of Ba1/BBB-/BBB. The new AT1s were priced in line with its existing curve, given that its older 4.5% perp issued last February and callable in 2030 is currently trading at 99.4 yielding 4.58% currently.

New Bond Pipeline

- NTT multi-trancher $/€ bond

- HCL Tech $ bond

- Microsoft $ bond alongside exchange offer

- JSW Steel $ bond

Rating Changes

- New Zealand Ratings Raised To ‘AA+’ FC And ‘AAA’ LC By S&P As Pandemic Risks Moderate; Outlook Stable

- Fitch Revises Turkey’s Outlook to Stable; Affirms at ‘BB-‘

- Fitch Revises Bulgaria’s Outlook to Positive; Affirms at BBB

- Fitch Upgrades Geo Energy Resources to ‘CCC’

- Brazilian Steel Producer CSN Upgraded To ‘B+’ From ‘B’ As Mining Unit’s IPO Accelerates Deleveraging; Outlook Positive

- Brazilian Steelmaker Usiminas Upgraded To ‘BB-‘ From ‘B+’ On Strong Industry Upswing And Low Leverage; Outlook Stable

- Embraer Downgraded To ‘BB’ From ‘BB+’ As Weak Demand Prospects Cloud Hopes For Stronger Cash Flows, Outlook Negative

- Cape Verde Ratings Lowered To ‘B-‘ On Rising External And Budgetary Imbalances; Outlook Stable

- Moody’s affirms CAR’s Caa1 ratings, changes outlook to positive from negative

The Week That Was

US primary market issuances stood at $17.8bn, down 50% vs. $35.8bn the week prior. The drop in issuance can be attributed to both IG and HY, with the former at $14.3bn, down 31% WoW and the latter down 72% WoW at $3.45bn. Charter Communications’ dual-tranche $2.5bn, Global Payments’ $1.1bn and Expedia’s $1bn issuance were the most prominent deals in otherwise quiet week. In North America, there were a total of 30 upgrades and 21 downgrades combined, across the three major rating agencies last week. LatAm saw lower issuances than the week prior at $650mn, down 24% with Alpek SAB alone raising $600mn. EU Corporate G3 saw a slight increase with $22.6bn in deals vs. $18.4bn the week prior – H&M raised €500mn ($606mn) via a debut issuance, while UBS, BNP Paribas and Intesa lead the largest deals with over $6bn combined. GCC and Sukuk issuances were also lower at just $820mn vs. $4.2bn in the week prior led by NBK’s $700mn issuance, which saw it print the GCC’s second-lowest coupon on a dollar AT1 at 3.625%. APAC ex-Japan G3 issuances saw another slow week in primary markets following the Lunar New Year holidays with a meagre $450mn in deals vs. $1.4bn in the week prior – China Ping An’s $250mn and KDB’s $200mn. In the region, there were 5 upgrades and 2 downgrades combined, across the three major rating agencies last week.

Term of the Day

Moratorium

A moratorium is a temporary suspension on debt wherein the borrower does not have to make any repayments. It is a waiting period with some protections for the borrower before repayments begin. However, the interest is accumulated until the end of the moratorium period and the accrued interest is then added to the principal amount of the debt. Indonesian property developer Modernland applied to extend a debt moratorium, discussing a possible restructuring of its USD bonds following a default last year. A moratorium is due to expire on February 28, but the company has requested an extension to May 31. Modernland has two dollar bonds: a US$150m 10.75% August 30 2021 bond issued through JGC Ventures and a US$240m 6.95% bond due March 13, 2024.

Talking Heads

On the obstacles to higher yields in the world’s biggest debt market slowly melting away

Stephen Stanley, chief economist at Amherst Pierpont Securities

“Before the pandemic, the 10-year yield was trading at about 1.6%, and if we are going to get back to what the economic situation was — give or take — back then, then there’s no reason why yields should be lower than that,” said Stanley.

Chris McReynolds, head of U.S. inflation trading at Barclays Plc

“The reflation trade is going to stay,” said McReynolds. “We’ll of course continue to see volatility around inflation expectations and actual inflation prints themselves. But you have to take the Fed completely at their word, that they are going to be behind the curve” in tightening policy even as the economy and inflation pick up.

On the real yields on US Treasuries rising on hopes for buoyant economy

Collin Martin, fixed-income strategist at Charles Schwab

“On the individual side, the business side and the industrial side, the data continues to be strong,” Martin said.

In a research note by strategists at ING

“Should Treasury yields continue to rise too fast, it will bring everything else down with it,” strategists at ING wrote. “From here, slow and steady extends the party in [the] risk asset space . . . while fast and furious ends it.”

“The two big things right now are waiting for stimulus and this idea of the reflation trade — investors have a keen eye out for signs of inflation,” said Snyder. “You see Treasury yields moving higher, that’s causing a bit of consternation in the markets.”

On Europe’s bruised bond markets signalling more pain in store

Marco Meijer, a senior G-10 rates strategist at BNP Paribas SA

“Investors are more keen to protect against a rise in rates than a fall, suggesting there is more pain,” said Meijer. Dealers taking the other side of these trades “could lead to an amplified move,” he added.

In a note by Adam Kurpiel and his team, Societe Generale SA strategists

“This is consistent with the acceleration in the yield sell-off and increasing rates volatility,” they wrote.

“It’s now the high-yield bond market in name only,” said Eagan. “I don’t like the fact yields are really low but that’s the environment we are working in.” On low spreads resulting in little room to absorb losses, “that’s the big risk,” said Eagan. “There is a leap of faith and you have to make a call as an investor. Our view is the economy is going to come back pretty solidly.”

On the dark side for Emerging Markets caused by reflation euphoria

John Normand, Head of Cross-Asset Fundamental Strategy at JPMorgan

“If a particular allocation across the risky markets spectrum should be low confidence this year, it is the EM overweight,” Normand wrote.

In a note by Kamakshya Trivedi and team, Goldman Sachs strategists

“A sharp move higher in U.S. rates can drive sharp selloffs among highly-positioned high-yielding EM currencies on a tactical horizon,” the strategists wrote. These “moves can retrace once the pace of the rate move moderates,” they added.

Khoon Goh, head of Asia research at Australia & New Zealand Banking Group Ltd

“We remain positive on Asian currencies, and see the positive growth outlook for the region outweighing the move in yield,” he said.

On the tightened online lending rules a fresh blow to Jack Ma’s Ant Group

Michael Pettis, finance professor at Peking University

“This will raise financing costs for consumers and will cripple one of the fastest-growing business segments for Ant, almost certainly forcing a steep drop in its eventual valuation,” said Pettis.

Bruce Pang, head of macro and strategy research at China Renaissance Securities

“Online lending platforms could face more valuation pressure with dampened growth prospects, considering that they would have to raise more capital to fund [themselves] in joint loans with banks,” Pang said.

Top Gainers & Losers – 22-Feb-21*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.