This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Philippines, Logan, Mongolia Launch $ Bonds; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers & Losers

June 28, 2021

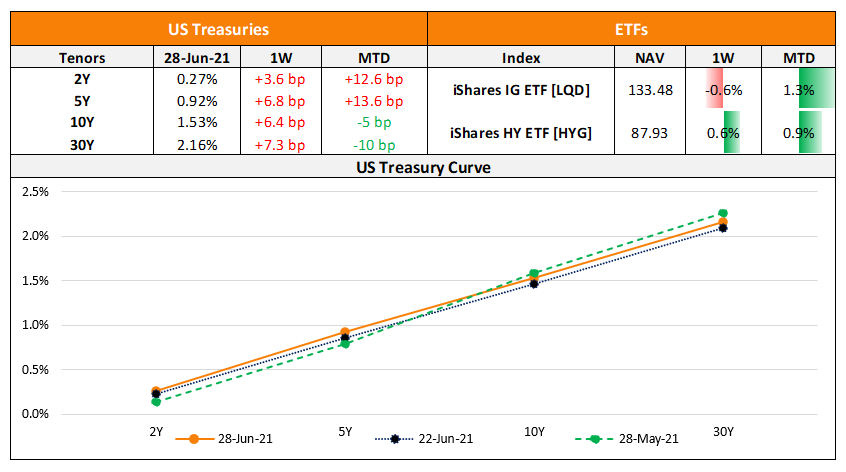

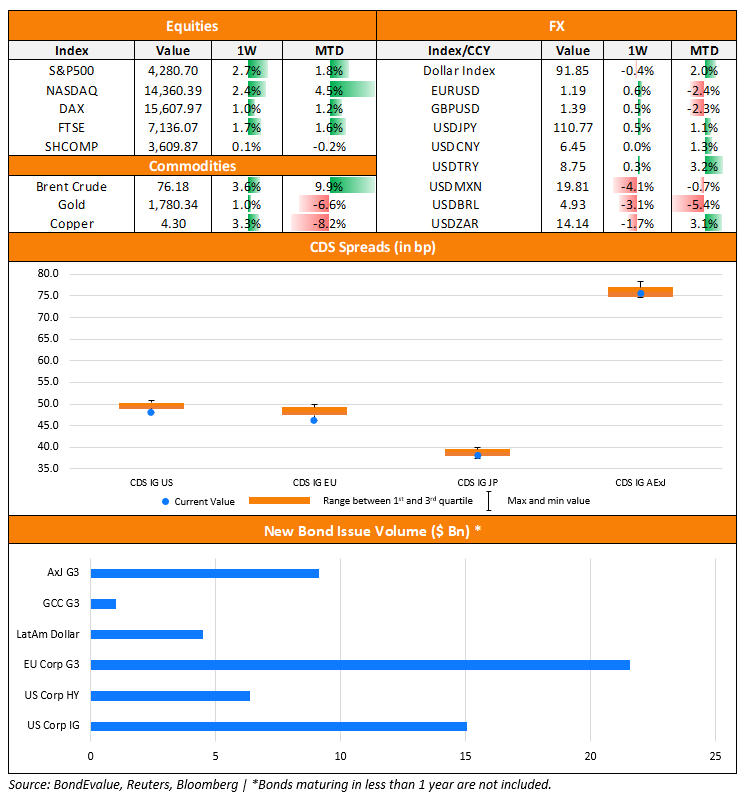

US markets carved out a winning week with the S&P up 0.3% on Friday reaching another record while Nasdaq was broadly flat; they ended the week higher by 2.7% and 2.4% respectively. The gains came on the back of weaker than expected inflation data and President Biden securing an infrastructure agreement with lawmakers. Financials, up 1.3%, once again led on Friday after the Fed indicated that the banking industry could withstand a severe recession. IT, down 0.15%, dragged the markets lower. US 10Y Treasury yields trended higher by 2bp to end the week at 1.52%. The increase came after the Fed’s main inflation reading, Core PCE rose 3.4%, the most since 1992, on supply constraints and increased demand for services in May. Consumer spending remained broadly flat vs. a 0.9% increase in April. European bourses also finished the week slightly higher – FTSE and DAX were up 0.4% and 0.1% while CAC was down 0.1%. US IG and HY CDS spreads tightened 0.8bp and 3.6bp respectively. EU main and crossover CDS tightened 0.5bp and 2bp respectively. Saudi TASI and Abu Dhabi’s ADX were up 0.4% and 2% respectively. Brazil’s Bovespa reversed gains and was 1.7% down. Asian markets opened mixed – Singapore’s STI was up 0.3% and Shanghai up 0.1% and Nikkei was down 0.1%. Asia ex-Japan CDS spreads were 0.5bp tighter. It’s a busy start to the week at the Asian primary markets with six new dollar deals launched.

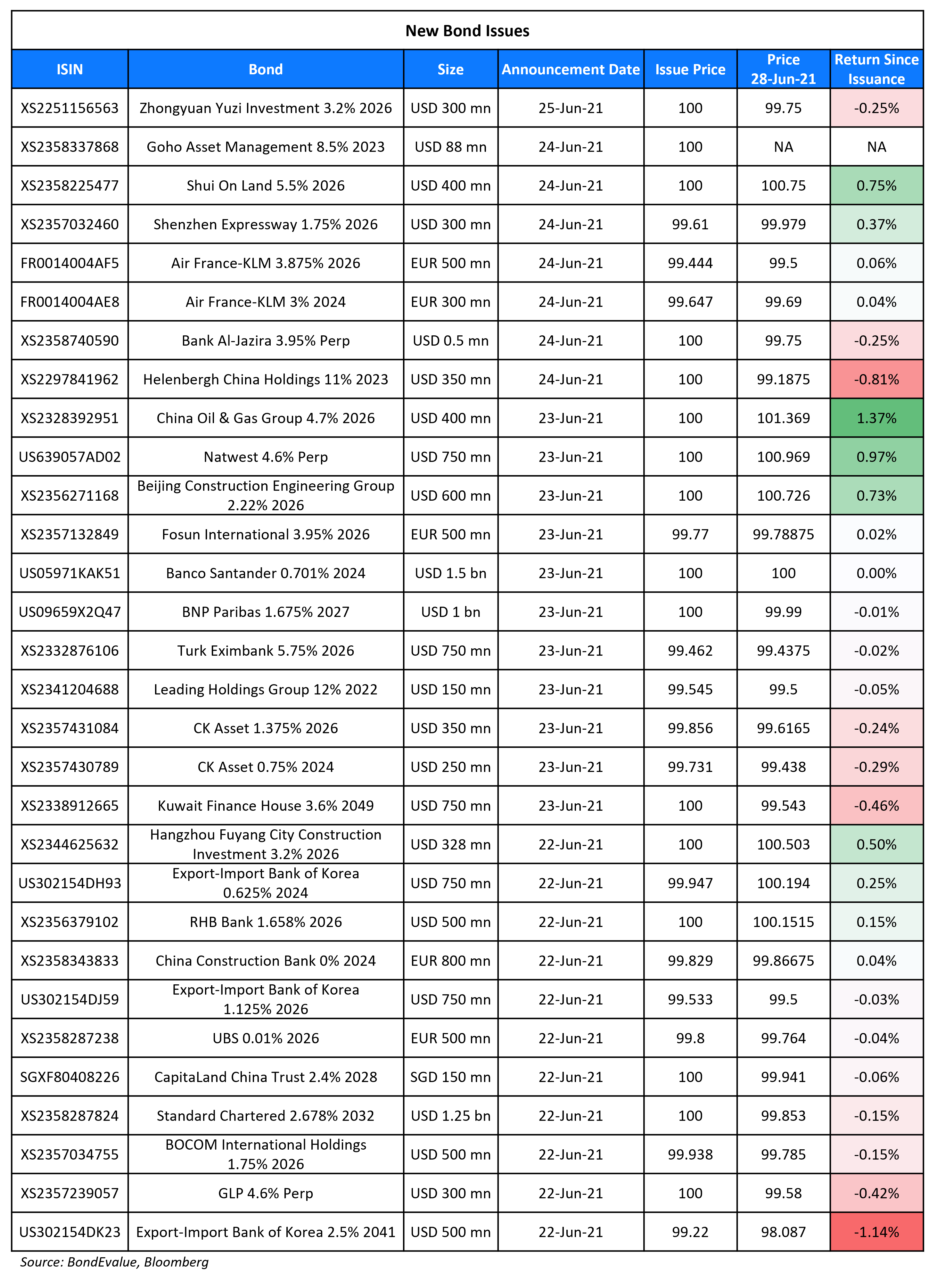

New Bond Issues

- Philippines $ 10.5Y/25Y SEC-registered bond at T+90bp/3.55% areas

- Logan Group $ 5NC3 green bonds at 5.05% area

- Mongolia $ 6Y/10Y Yankee at 4.25%/5.25% areas

- Sumitomo $ 5Y bonds at T5+95bp area

- LG Chem $ green 5yr/10yr Yankee at T+100bp/T+130bp areas

- Linyi City Construction Investment Group $ 3Y at 3% area

Zhongyuan Yuzi Investment raised $300mn via a 5Y bond at a yield of 3.2%, 3bp inside initial guidance of 3.5% area. The bonds are rated A2/A and received orders over $1.1bn, 3.7x issue size. The issuer is Zhongyuan Zhicheng and the bonds are guaranteed by Zhongyuan Yuzi Investment. The Chinese LGFV will use proceeds for offshore debt refinancing and general corporate purposes.

New Bond Pipeline

- SoftBank hires DB, Barclays, HSBC for US$/EUR bonds

- China National Bluestar hires for $ Perp

- Wuhan Urban Construction Group hires for $ sustainability bonds

- Bank of Communications (Hong Kong) hires for US$ 10NC5 T2

- Korea Gas Corp hires for $ 5Y and/or 10Y bond

-

Mirae Asset Securities hires for $ green bond; calls starting today

- Laos plans $ bond offering; to repay 2021s

- Kunming Public Rental Housing Development Construction hires for $ bond

Rating Changes

- Fitch Upgrades Kinross Gold Corporation’s IDR to ‘BBB’; Outlook Revised to Stable

- Moody’s downgrades Televisa’s ratings to Baa2; stable outlook

- Banco BBVA Peru Outlook Revised To Stable From Negative By S&P After Similar Action On Parent

- Dubai-Based Real Estate Developer Emaar Properties Outlook Revised To Stable From Negative By S&P On Stronger Demand

- Fitch Publishes INEOS Enterprises’ 1st-Time IDR ‘BB-‘; Outlook Stable

- Moody’s changes Marfrig’s outlook to positive; Ba3 rating affirmed

The Week That Was

US primary market issuances were marginally higher at $23.1bn vs. $21.8bn in the week prior led by IG. IG issuances rose last week to $15.1bn vs. $13.2bn in the prior week while HY issuances were lower at $6.4bn vs. $8.25bn in the prior week. The largest deals in the IG space were led by JPMorgan’s $2.5bn dual-trancher, HCA’s $2.35 dual-trancher and Centene Corp’s $1.8bn issuance. In the HY space, ITT Holdings’ $1.22bn deal and Ford’s $1bn deals led the table. In North America, there were a total of 62 upgrades and 14 downgrades combined across the three major rating agencies last week. LatAm saw $4.51bn vs. $1.2bn in issuances in the prior week, led by the Panama government’s $2bn dual-trancher and Panama Bonos’ $1.25bn deal. EU Corporate G3 issuances were slightly lower at $21.6bn vs. $24.1bn in the week prior – primarily dominated by financial institutions with Santander’s $1.5bn 3NC2 deal, StanChart’s $1.25bn 11NC10 deal and UniCredit’s €1bn ($1.2bn) deal leading the table. Across the European region, there were 30 upgrades and 771 downgrades across the three major rating agencies – the massive number of downgrades was largely on account of S&P’s downgrade of 7 German banks and their various related entities. GCC and Sukuk G3 issuances were lower at $1bn vs. $2.65bn in the week prior led by Kuwait Finance House’s $750mn AT1 Sukuk and Emirates NBD’s $250mn 5Y deal. Across the Middle East/Africa region, there were no upgrades but 11 downgrades across the three major rating agencies. APAC ex-Japan G3 issuances were at $9.1bn vs. $6.1bn in the prior week – KEXIM’s $1.5bn two-trancher led the table followed by KHFC’s €1bn ($bn) social covered bond and CCB’s (HK Branch) €800mn ($952mn) 3Y bond issuance. Other large issuances included BCEG HK Co’s $600mn, Fosun’s €500mn ($596mn) and BOCOM International’s $500mn new bond deals. In the Asia ex-Japan region, there were 9 upgrades and 6 downgrades combined across the three major rating agencies last week.

Term of the Day

Bad Bank

A bad bank is a bank set-up to buy bad loans and other non-performing assets from banks. While it may help reduce systemic impacts in the financial system, critics note that it may create moral hazard risks. India is set to have a bad bank by month-end called the National Asset Reconstruction Company (NARCL). NARCL will take over the bad loans from banks by paying 15% in cash and 85% as security receipts. The security receipts will be backed by a government guarantee, which is likely to ensure the face value of the security receipts.

Talking Heads

On the possibility that conditions for rate increase could be met next year – Eric Rosengren, Boston Federal Reserve Bank President

“But it wouldn’t surprise me based on the current projections of what we’re seeing in the data that that criteria could be met as soon as the end of next year.” “A lot depends on exactly what happens with the economy over the course of the summer and into the fall.”

“The last three months have been a pretty slow slog for sure, but we are still bearish.” “I suspect tapering would probably be a big trigger for higher yields.” “And inflation helps that too.”

“Companies are using their cash to pay down upcoming maturities, and funding needs are low.”

Charles Chang, a director at rating agency S&P

“We don’t expect it, but if the Huarong situation results in a default, then what does that say about government support for other government-owned entities?” “If it turns out that a default or restructuring occurs, we will need to take a look at all [of them]”.

“We don’t expect it, but if the Huarong situation results in a default, then what does that say about government support for other government-owned entities?” “If it turns out that a default or restructuring occurs, we will need to take a look at all [of them]”.

Jason Tan, analyst at CreditSights

“During the tenure of the former chair, Huarong expanded into many business lines unrelated to its core mandate of distressed debt management.” This “ultimately led to the downfall of the chair and a reckoning for the company.”

“During the tenure of the former chair, Huarong expanded into many business lines unrelated to its core mandate of distressed debt management.” This “ultimately led to the downfall of the chair and a reckoning for the company.”

Ronald Thompson, a managing director of Alvarez & Marsal Asia

“Where [in] the US, we would have high yield lenders, we would have high-yield bonds, we would have private equity players, the asset management companies have partially filled that role in China,” said Thompson. “If you’re a boss of an AMC [asset management company] and your future is to close it down next year as was originally designed,” he added, “it’s probably not good for morale.”

“Where [in] the US, we would have high yield lenders, we would have high-yield bonds, we would have private equity players, the asset management companies have partially filled that role in China,” said Thompson. “If you’re a boss of an AMC [asset management company] and your future is to close it down next year as was originally designed,” he added, “it’s probably not good for morale.”

Raj Kumar Bansal, managing director at Edelweiss Asset Reconstruction Co

“The proposed bad bank is useful as a one-time clean-up exercise of the bad loans that are pending resolution for years now.” “But it’s not a long-term solution in dealing with the stressed assets.”

Nikhil Shah, managing director at Alvarez & Marsal India

“India’s bankruptcy reforms started off well but they have slowed currently.” “Prolonged delays in resolutions, lengthy court battles, and uncertainty of recoveries post-approval of resolution plans are pushing many potential investors away” from the bankruptcy process, he said.

Prashant Kumar, chief executive officer at Yes Bank Ltd

“Stressed loans have taken far too much management time across the industry in the past couple of years.” “This bad bank will help shift focus from resolving soured loans to improving credit growth.”

Using bitcoin for all obligations “may increase the risks that proceeds from illicit activities pass through the Salvadoran financial system,” Fitch said. “Bitcoin’s lack of transparency could increase the risk of money laundering.”

Top Gainers & Losers – 28-Jun-21*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.