We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

NFP at 187k, ISM Manufacturing PMI Continues to Show Contraction

September 4, 2023

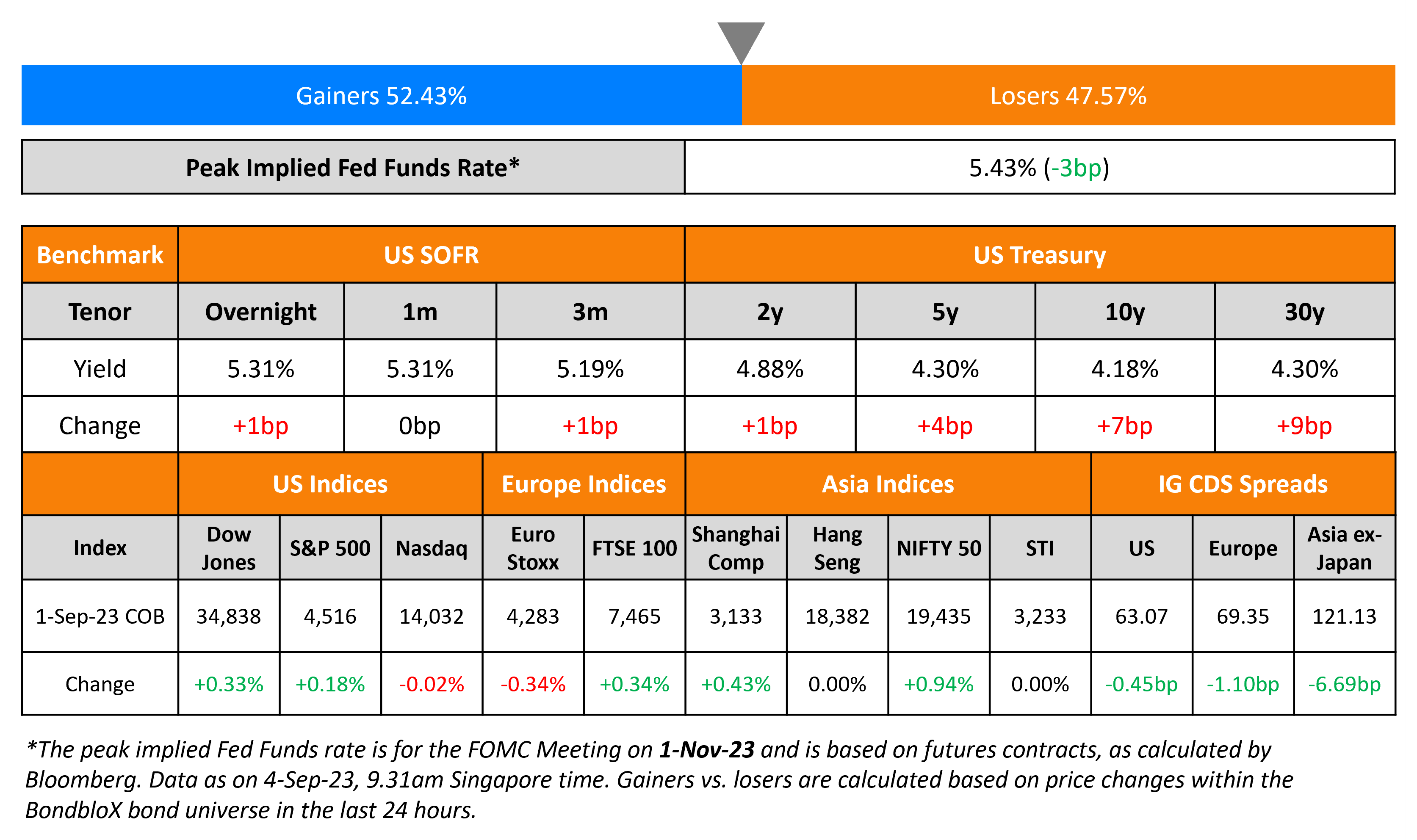

The US Treasury yield curve bear steepened with long end yields moving higher – the 10Y and 30Y yields were up 7-9bp while the 2Y and 5Y yields were up 1-4bp. US NFP for August came at 187k, higher than the surveyed 170k and at the same level as last month’s 187k. The unemployment rate was at 3.8%, higher than the surveyed 3.5%. Average Hourly Earnings YoY came at 4.3%, in-line with the surveyed 4.3%. The US manufacturing sector continued to show a slowdown with ISM Manufacturing PMI at 47.6 last month, slightly higher than 46.4 in July and estimates of 47, still indicating a contraction. New Orders slipped to 46.8 last month from 47.3 in July and the Prices Paid index rose to 48.4 last month from 42.6 in July. CME probabilities for a 25bp rate hike at the November meeting have dipped further to 35% from 45% last week. US IG credit spreads were tighter by 0.5bp while HY CDS spreads tightened 3.3bp. The S&P inched 0.2% higher while Nasdaq were ended flat.

European equity markets were mixed. In credit markets, European main CDS spreads were tighter by 1.1bp with crossover spreads tightening 0.6bp. Asian equity markets have opened mixed this morning and Asia ex-Japan CDS spreads have tightened by 6.7bp.

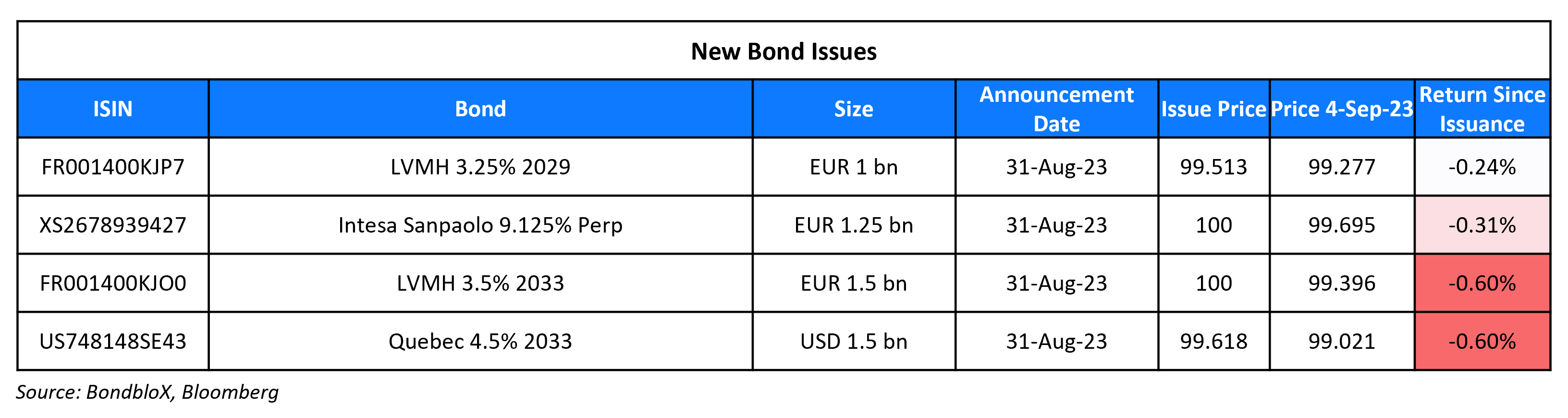

New Bond Issues

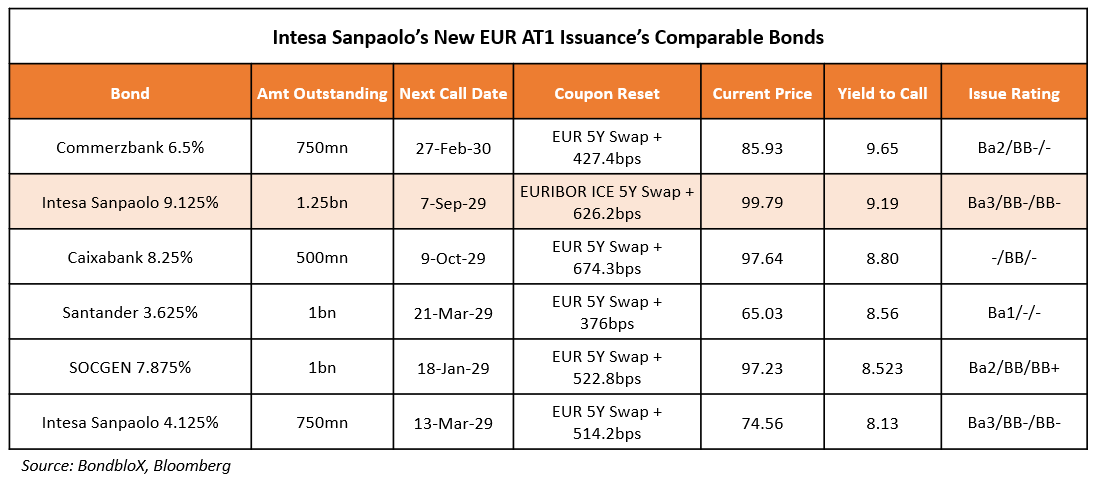

Intesa Sanpaolo raised €1.25bn via a PerpNC6.5 AT1 bond at a yield of 9.333%, 29.2bp inside initial guidance of 9.625% area. If uncalled after 5 years, the coupon will reset on the first reset date and every 5 years thereafter at the EURIBOR ICE 5Y Swap rate plus a spread of 626.2bps. The bonds have expected ratings of Ba3/BB-/BB-, and received orders over €4.6bn, 3.7x issue size. The notes have a 75% clean-up call. Proceeds will be used for general funding purposes and to improve the regulatory capital structure of the issuer. The table below compares Intesa Sanpaolo’s new AT1s with other similarly rated EUR-denominated AT1s.

Rating Changes

- Moody’s downgrades VNET’s CFR to Caa1; outlook remains negative

- Carvana Co. Downgraded To ‘D’ From ‘CC’ On Completion Of Distressed Exchange; Senior Notes Rating Lowered To ‘D’

- Fitch Downgrades China Great Wall to ‘BBB+’; Maintains RWN

New Bond Pipeline

- AIA hires for S$ Perp NC5.5 Tier 2 bond

- Hong Kong Mortgage Corp hires for $ Social bond

- ADCB hires for $ Long 5Y Green bond

- LG Energy hires for $ 3Y and/or 5Y Green bond

- Mongolian Mining hires for $ bond

Recently, French lender Credit Agricole tapped on the Singapore dollar bond market for the second time this year, raising S$350mn by issuing a 10NC5 Tier 2 bond (scroll down for a refresher on bank capital) at 5.25%. This is the second European bank that has issued a Tier 2 note in Singapore since the Credit Suisse AT1 wipeout in March 2023, signaling early signs of recovery in the bank capital bond market in Singapore. Aside from Credit Agricole, Lloyds forayed into the SGD market for the first time two weeks ago, issuing a similar 10NC5 Tier 2 that priced at the same level of 5.25%. The Singapore dollar bond market for bank Tier2 notes thus seems to be witnessing a comeback to the primary markets. In this piece, we compare different SGD bank Tier 2 bonds and also put them against its USD comparables.

Term of the Day

EURIBOR

Euribor is an average unsecured inter-bank rate complied from a panel of 20 large European banks that lend money on an overnight basis to one another in Euros. Maturities on loans used to calculate Euribor often range from one week to one year. Euribor is generally considered as a reference rate for pricing bonds denominated in Euros. The equivalent of Euribor in the US is the USD Libor rate.

Talking Heads

On Investors from BlackRock to Pimco, Betting that Fed Hikes Are Over

Michael Cudzil, a portfolio manager at PIMCO

“The bond market comfortable with the view that the Fed is on hold for now and maybe done for the cycle… If they are done for the hiking cycle, it’s then about looking at the first cut that leads to steeper curves”

George Goncalves, head of US macro strategy at MUFG

“(Jobs report) will favor the front-end versus the back-end”

Subadra Rajappa, head of US rates strategy at SocGen

“The trade to be in is steepeners. Either the market starts to price in more Fed cuts and the curve bull-steepens, or the Fed stays on hold with strong data and long-end sells off in that case”

On ‘Put Your Shoulder’ Into Bonds as Fed Rate Risk Recedes – BlackRock’s FI CIO, Rick Rieder

“The Fed should be done. You can put your shoulder behind a bit more of interest-rate exposure than has been the case certainly over the last few months… We like holding the front end… you get paid if you buy commercial paper, etc at about 6%. It’s been incredible. But I think now you can actually extend that a bit further out the curve” and “we’ve been adding some out to the belly of the curve”

On Wall of Corporate Debt to Spark Recession in 2024 – Fidelity International

“The end point of the cycle is recession, because the transmission channel will kick in. If the Fed doesn’t back off at some point, everybody has to pay these higher real rates… Borrowers are not feeling the full pressure of the interest rate because they are sitting on locked rates, which is not a permanent phenomenon”

On Higher-for-Longer Mantra Starting to Weigh on Emerging-Market Debt

Jon Harrison, MD for EM macro strategy, GlobalData TS Lombard

“The inflation outlook for emerging markets is becoming less certain, in contrast to the broad-based disinflation of the past four-to-five months”

Duncan Tan, currency and rates strategist at DBS Bank

“Across regional Asian swap markets, the front-end of curves have gone from unwinding the pricing of rate cuts to now pricing up to a 25-basis-point increase by year-end… widening term premium suggests that participants see non-negligible risks of rate hikes starting again”

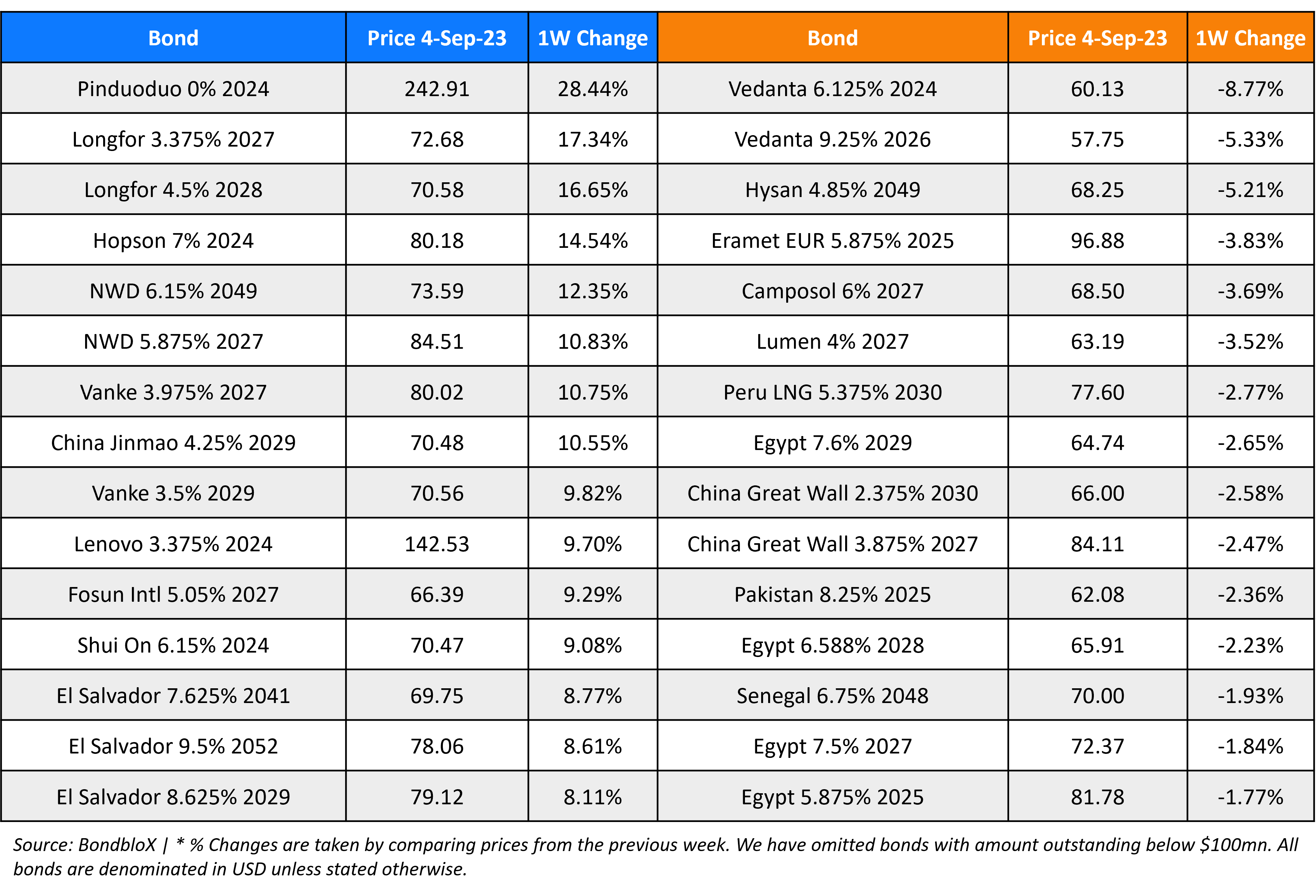

Top Gainers & Losers- 04-September-23*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.