This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Moody’s Says Indebted Chinese SOEs Remain Key Risk Despite some Deleveraging

December 9, 2021

Moody’s in a new report said that further deleveraging progress in Chinese state-owned enterprises (SOEs) will be difficult despite the Chinese government’s efforts to reduce leverage. The rating agency noted that China’s most indebted listed SOEs saw their liabilities-to-equity fall from a peak in 2018, indicating lower risk to the government’s balance sheet, although they note that it is still higher than that in 2015. On average, the most leveraged SOEs in 2020 were larger than those in the 2015 highly indebted grouping, suggesting potentially higher costs in the event of collapse. They added that while profitability fell, leverage at local government-owned SOEs was still climbing despite deleveraging efforts at central government-owned SOEs. “Increases in liabilities and lower profitability at local SOEs will continue to create pockets of risk in provincial and local systems, raising the risk of a crystallization of some of these contingent liabilities,” said Moody’s VP Martin Petch. Given China’s declining medium-term GDP growth rate, SOE leverage is expected to rise if productivity growth remains modest. Additionally, reforming local SOEs is harder than that of central government SOEs as control is more diluted with a wider range of entities to manage. Besides, regional and local governments are also limited by their financial resources as compared to the central government when implementing deleveraging.

For the full story, click here.

Go back to Latest bond Market News

Related Posts:

Opposing Views on Chinese Real Estate Dollar Bonds

October 2, 2017

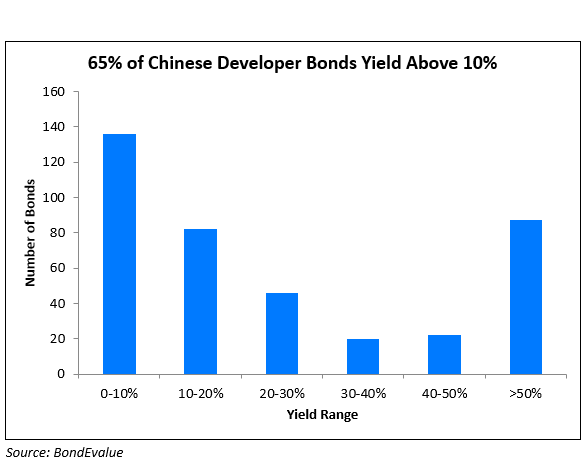

65% of Chinese Developers’ Dollar Bonds Now Yield > 10%

October 13, 2021

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.