We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

May 2023: Bond Rally Stalls With 79% of Dollar Bonds in the Red

June 1, 2023

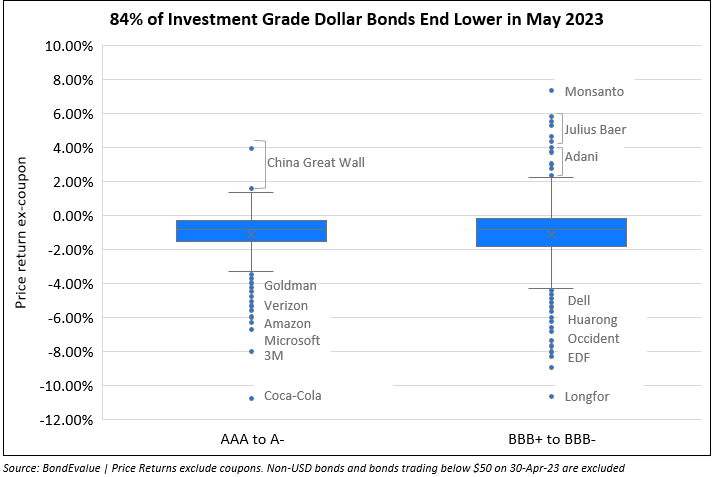

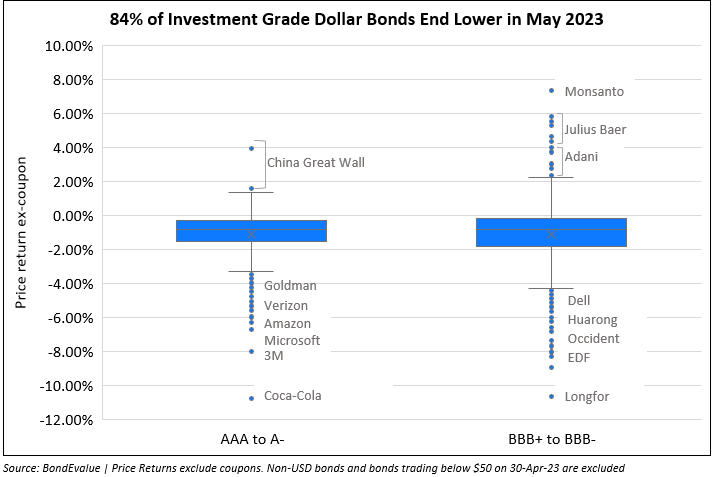

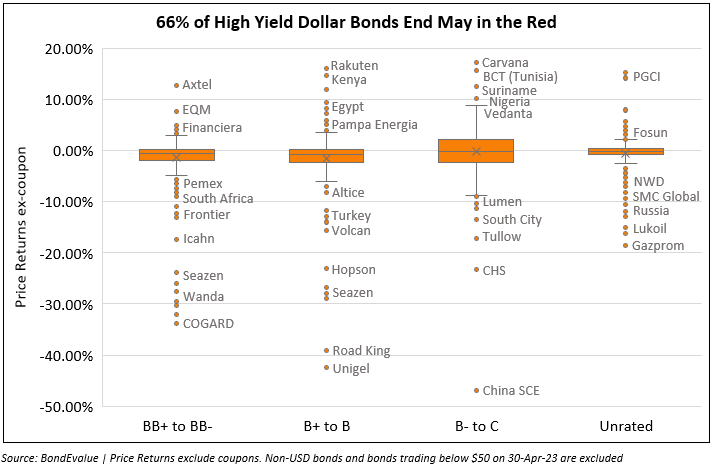

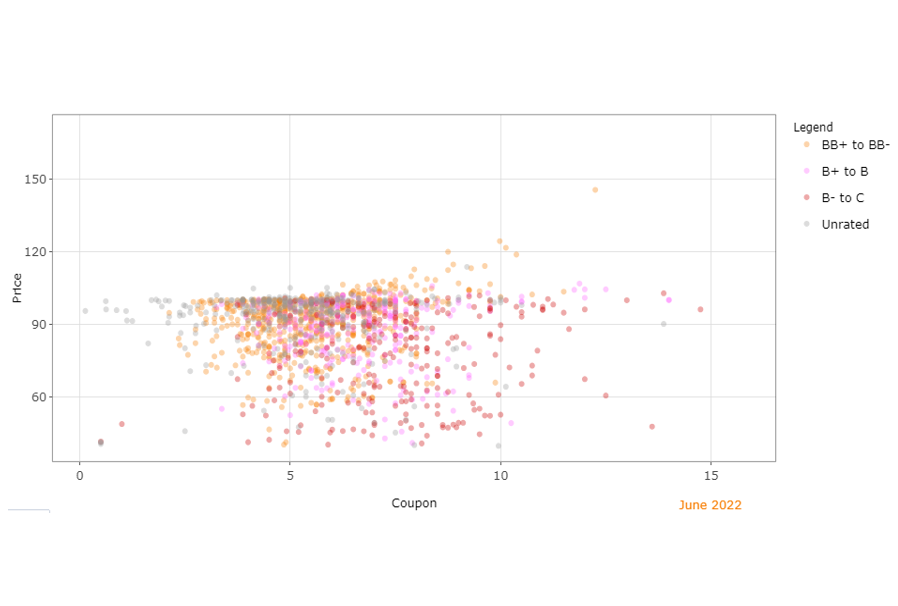

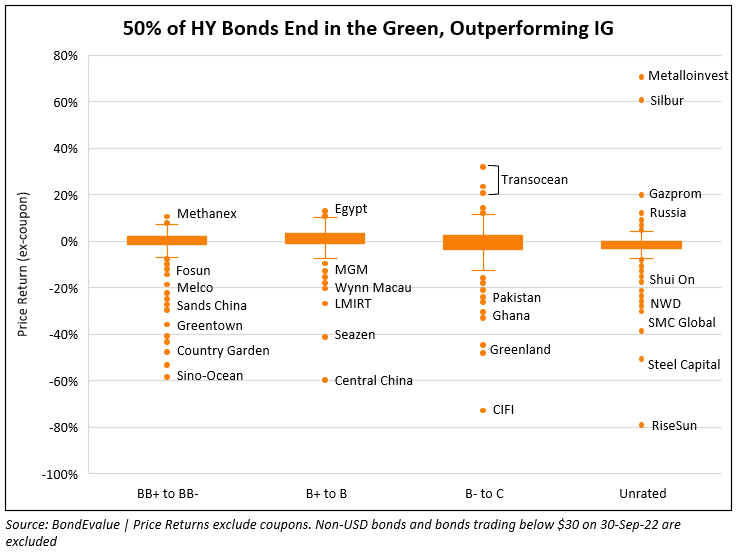

The month of May saw a reversal in fortunes for bond markets after a cheerful first quarter and its extended run in April. 79% of dollar bonds in our universe ended May in the red (ex-coupon) as compared to 81% that ended April in the green. Of this, Investment Grade (IG) bonds underperformed High Yield (HY) as seen in the table below with 84% of bonds ending lower in the former and 66% in the latter. The underperformance in IG-rated bonds primarily comes on the back of its duration sensitivity following the massive sell-off in US Treasuries over the course of the month.

The month was plagued with debt ceiling concerns and the possibility of the US government defaulting on its debts coming due in June. Besides, continued fears of a banking contagion possibly spilling over to more regional banks also contributed to the move. This initially led to a sharp rally across Treasuries with the 2Y and 10Y yield touching 3.80% and 3.33% on May 4. However, strong economic data provided a floor to benchmark yields. NFP came at 253k for April, higher than the surveyed 185k and Average Hourly Earnings YoY was at 4.4%, higher than the surveyed 4.2%. Also, inflation continued to inch slightly lower albeit still sticky. CPI came at 4.9% for April 2023, below expectations of 5% while Core CPI came at 5.5%, in-line with the expectations. Underlying data provided an impetus for a 25bp Fed rate hike in June - the probability rose from 0% at the start of the month to 65% in late-May. Treasury yields steadily climbed higher over the course of the month with the 2Y and 10Y yield ending May at 4.4% and 3.64% respectively. In the latest update (as of 1 June) however, Fed Governor and Vice-Chair Philip Jefferson hinted that the Fed may skip a rate hike at the June meeting and his remarks were also echoed by Philadelphia Fed President Patrick Harker. This led to a big shift in CME probabilities. Markets are now pricing in a 60% chance of a status quo in June vs. a 60% probability of a 25bp hike just yesterday.

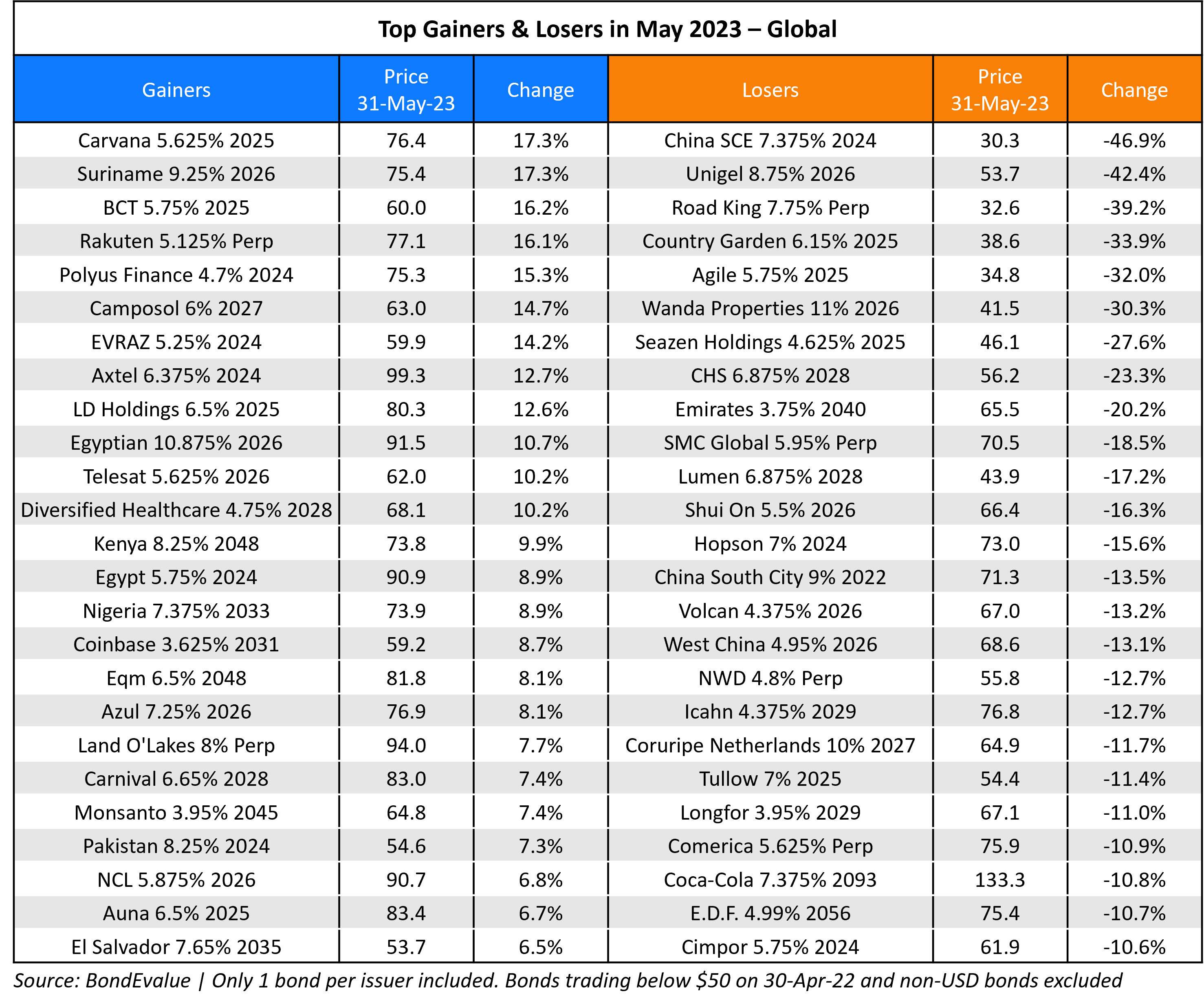

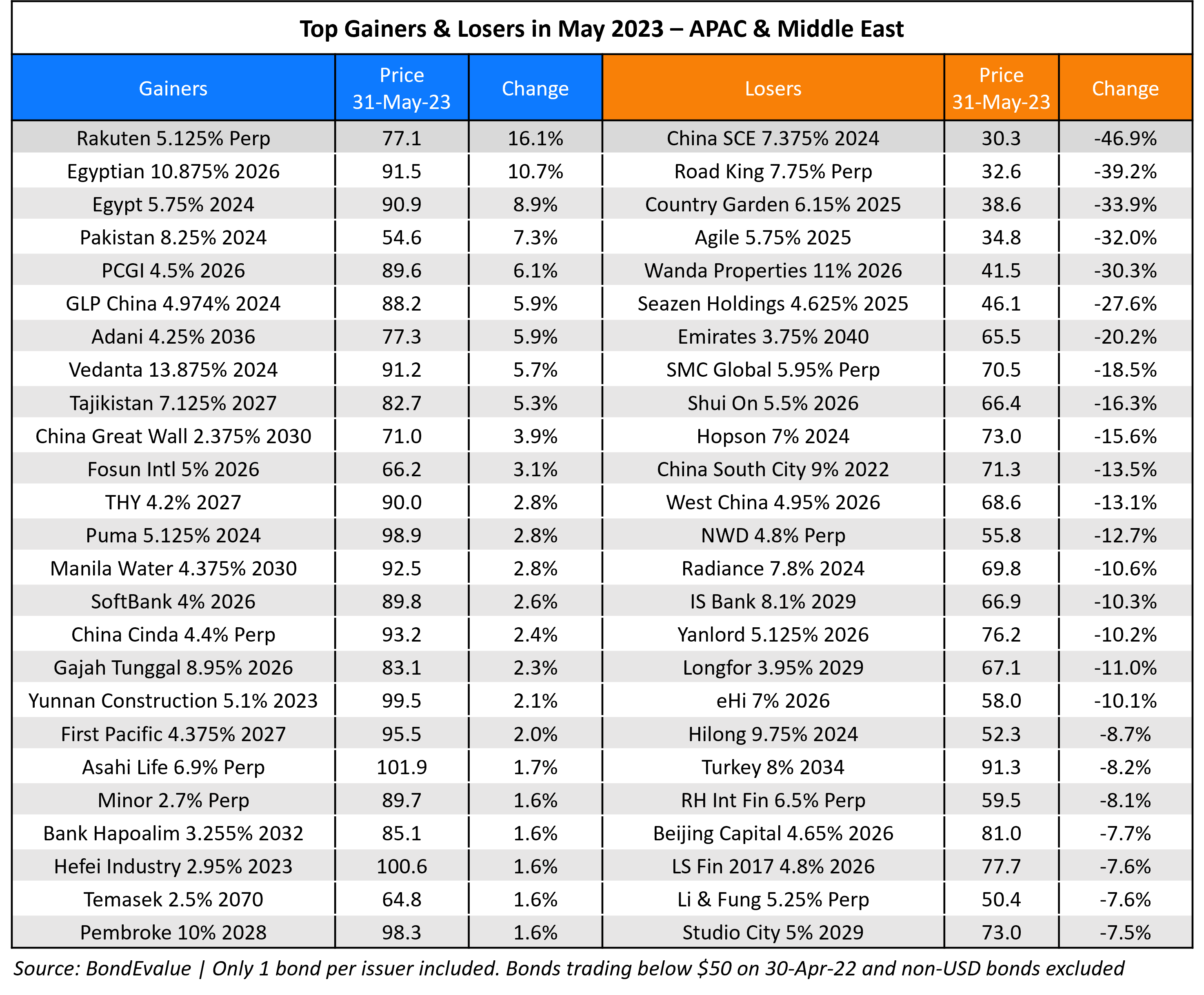

The biggest gainers in the IG-space were led by Monsanto after a five-week trial on a judicial claim saw them win. Julius Baer's bonds also were among the gainers, followed by Adani Group's dollar bonds that saw some positive news. Adani Group companies' were said to be planning to raise $3-5bn. China Great Wall AMC's dollar bonds were also among the handful of gainers in this space. Within the AAA to A- space, the biggest losers were long-dated, duration sensitive bonds of top-rated issuers like Coca-Cola, 3M, Microsoft, Amazon etc. The losers in the BBB+ to BBB- space were led by Longfor Group's dollar bonds that were hit by worries about the Chinese property bond market spreading over to the company and other IG-rated names like GLP China. Other losers included long-dated bonds of EDF, Occidental, Huarong and Dell amongst others.

In the High Yield space, the most prominent gainers were bonds of Carvana where the company is trying to stop its cash burn and said it expects to return to profitability this quarter. Several African nations' dollar bonds also made the top gainers list, led by BCT whose bonds rallied over 15% as the IMF signaled they were “almost there” towards completing a $1.9bn rescue package for the nation. Nigeria's dollar bonds were also among the top gainers recording their biggest gain in a month after their President said he will end its $10bn fuel-subsidy program and also try adopting a uniform exchange rate. Similarly, Kenya's bonds also rose with the IMF and World Bank providing support to the nation. Vedanta's dollar bonds also inched higher after the Anil Agarwal-led company secured sufficient loans to repay its dollar bonds and loans due in May and June. Among the losers, Chinese property developers like China SCE, Road King, Seazen, Wanda, COGARD and others trended lower as fresh concerns emerged on the state of the sector. Brazilian nitrogen fertilizer producer Unigel's bonds saw a massive drop of over 40% after an 82% EBITDA drop triggered concerns over covenant breaches. Other losers included Icahn Group's bonds following Hindenburg's report on the company. Turkey's dollar bonds dropped on the back of the incumbent President Erdogan winning the elections and extending his tenure.

Issuance Volumes

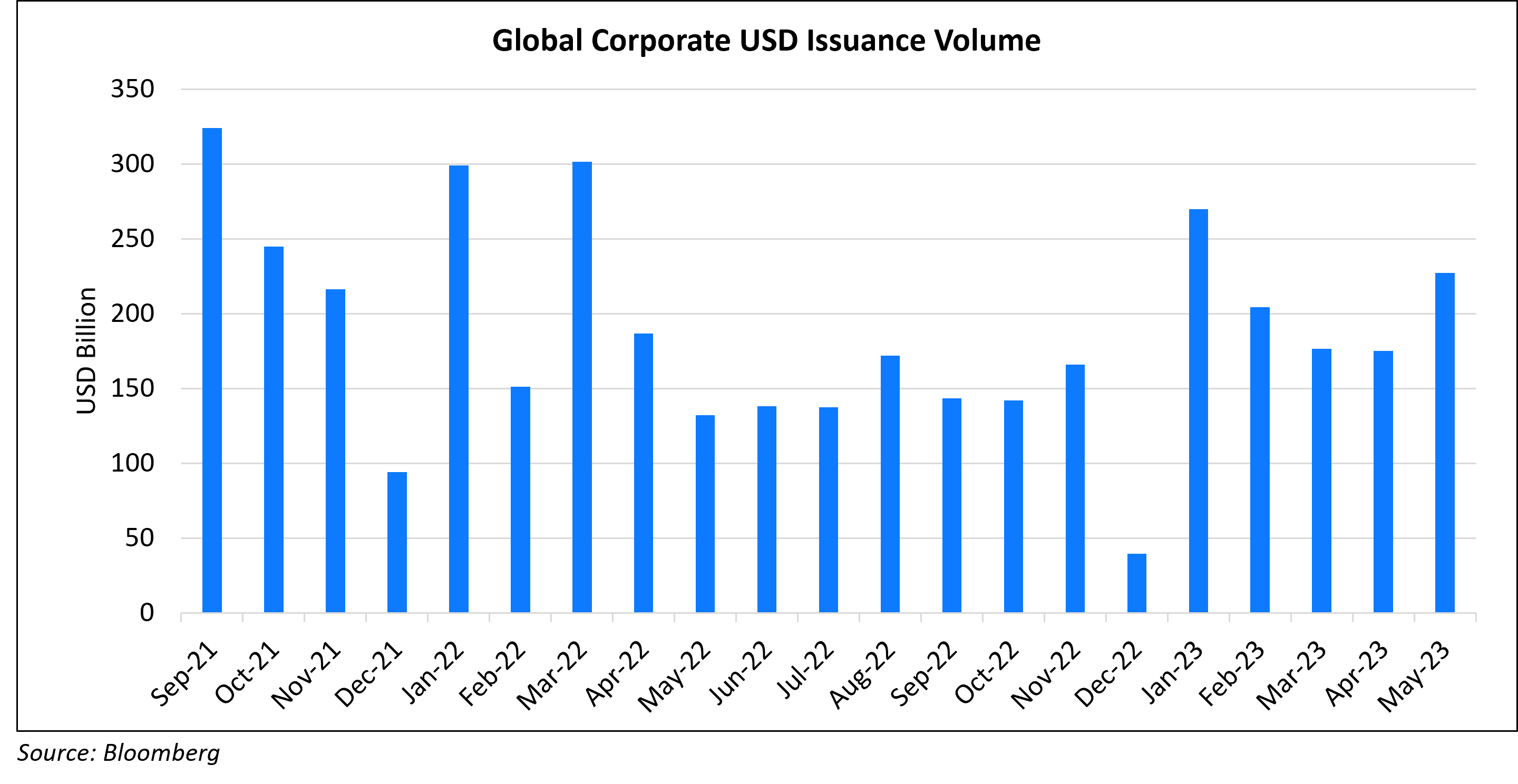

Global corporate dollar bond issuances stood at $227bn in May, 30% higher than April's $175bn. As compared to May 2022, issuance volumes were up over 72% YoY. 89% of the issuance volumes came from IG issuers with HY issuers taking the remainder.

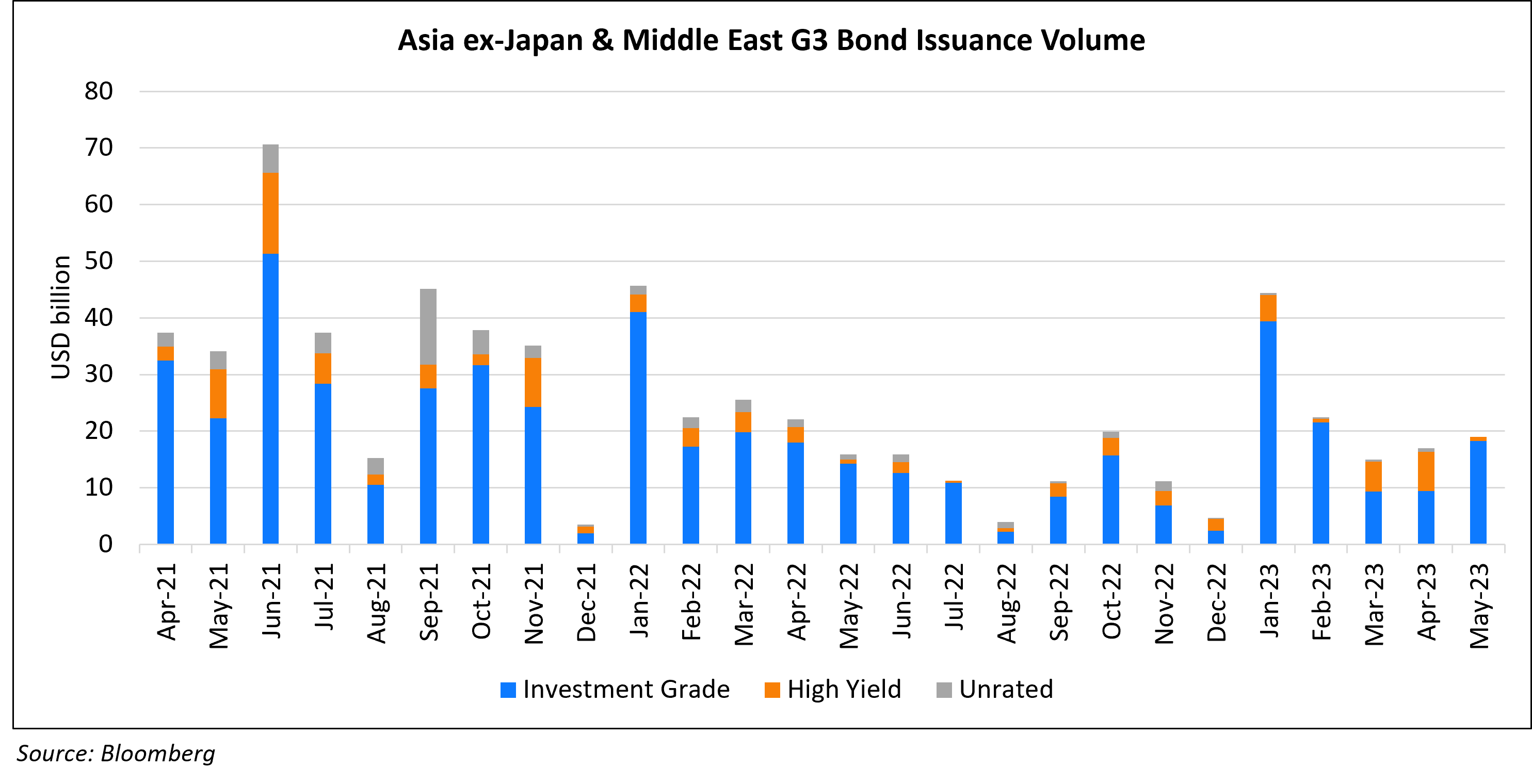

Asia ex-Japan & Middle East G3 issuance stood at $19bn, up 12% MoM and 20% YoY. 96% of the volumes came from IG issuers with HY issuers comprised the remaining 4%.

Largest Deals

The largest deal globally was led by Pfizer’s jumbo $31bn eight-tranche issuance, the fourth largest bond deal ever, to finance a portion of its Seagen merger. This was followed by Meta’s $8.5bn five-trancher earlier this month. Following these were Merck's and Saudi Government’s $6bn six-trancher and dual-tranche sukuk each. Other large deals included Apple’s $5.5bn five-trancher and Comcast's $5bn four-trancher, and Barclays' $4bn two-part issuance.

In the APAC and Middle East region, besides Saudi's $6bn sukuk deal, the largest deals included Westpac’s $1.75bn covered bond issuance, Khazanah’s $1.5bn dual-trancher and Eximbank China’s $1.5bn issuances.

Top Gainers and Losers

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.