We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

April 25, 2022

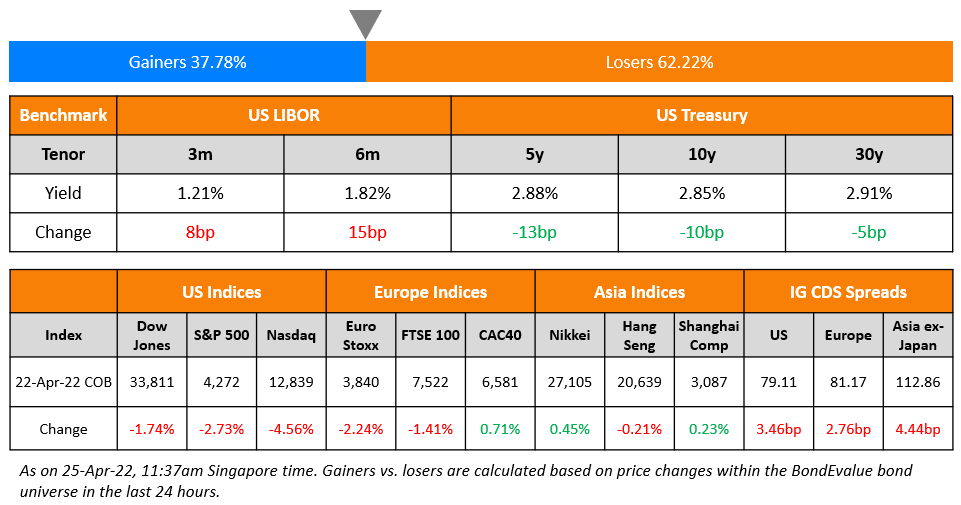

The S&P and Nasdaq ended sharply lower for a second straight day on Friday, down 2.8% and 2.6% respectively with all sectors in the red, led by Energy, down over 3.1%. US 10Y Treasury yields eased 10bp to 2.85% after a 9bp spike on Thursday with an overall risk-off sentiment being observed. European markets closed lower too with the DAX, CAC, FTSE down 2.5% 2% and 1.4%. Brazil’s Bovespa closed 2.9% lower. In the Middle East, UAE’s ADX was up 0.2% on Friday while Saudi TASI was down 0.5% on Sunday. Asian markets have opened sharply lower – Shanghai, HSI and Nikkei were down 2.4%, 2.6% and 1.7% while STI was down 0.2%. US IG and HY CDS spreads widened 3.5bp and 17bp respectively. EU Main spreads were 2.8bp wider and Crossover spreads were 11.4bp wider. Asia ex-Japan CDS spreads were 4.4bp wider.

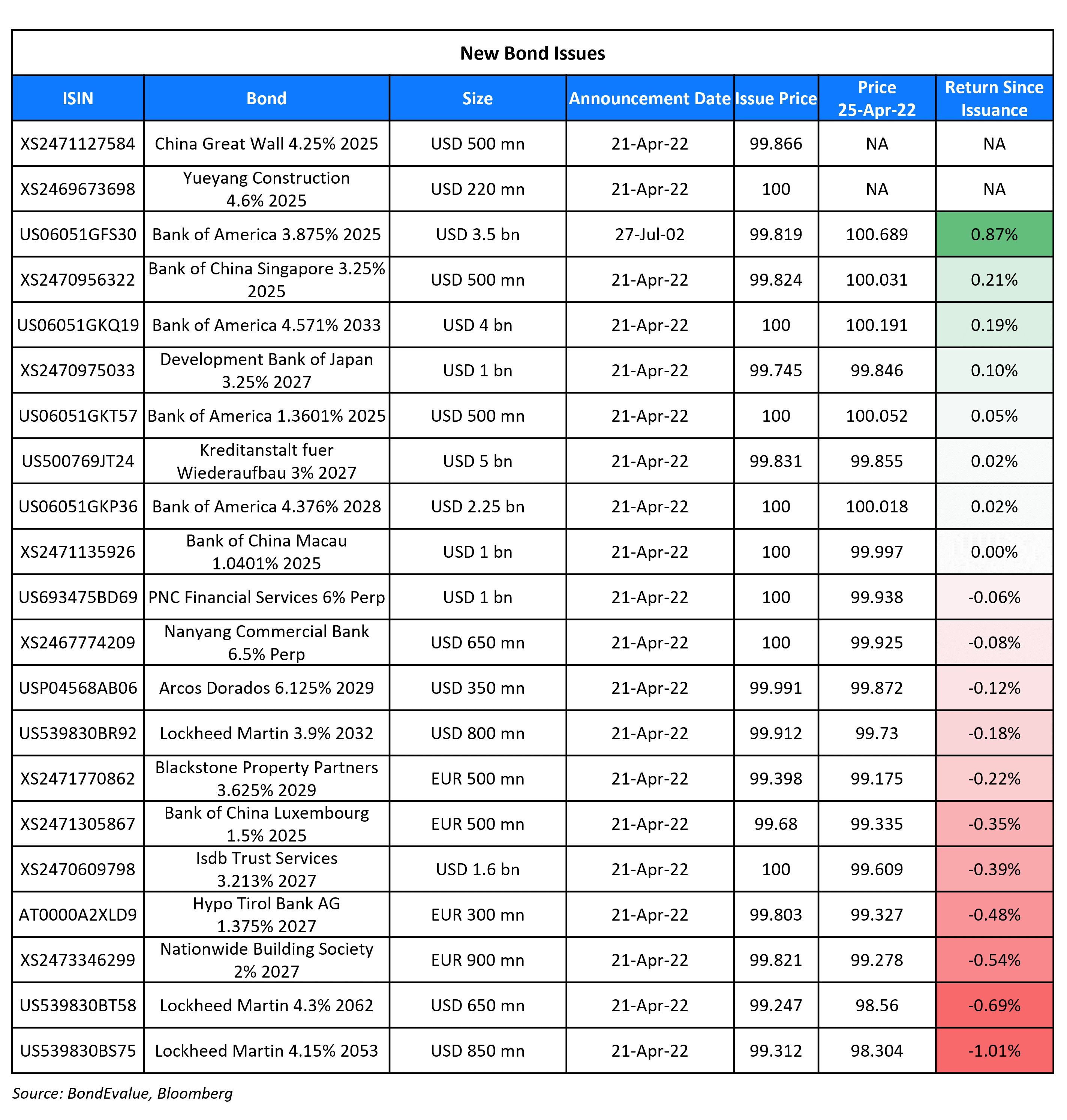

New Bond Issues

-

OUE Commercial REIT S$ 5Y at 4.5% area

Haitong Unitrust International Financial Leasing raised $200mn via a 3Y bond at a yield of 4.2%. The bonds are unrated and are issued by Haitong UT Brilliant and guaranteed by Haitong Unitrust. Proceeds will be used for offshore debt refinancing and the interest payments.

New Bonds Pipeline

- Orient Securities hires for € bond

- Korea East-West Power hires for $ 5Y Green bond

- Busan Bank hires for $ Social bond

- Kookmin Card hires for $ Sustainability bond

- ST Engineering hires for $ 5Y and/or 10Y

- Continuum Energy Aura hires for $ Green Bond

- Jubilant Pharma hires for $ bond

- Sael Limited hires for $ 7Y Green bond

Rating Changes

- Fitch Downgrades KWG to ‘B’; Maintains Rating Watch Negative

- Fitch Downgrades Redco to ‘RD’ from ‘C’, then Upgrades to ‘CCC-‘, After Exchange Offer

- Emirate of Sharjah Outlook Revised To Negative On Rising Fiscal Risks; ‘BBB-/A-3’ Ratings Affirmed

- Deutsche Telekom AG Outlook Revised To Positive On Strong Operating Performance; ‘BBB/A-2’ Ratings Affirmed

- Moody’s changes Bahrain’s outlook to stable, affirms B2 ratings

Term of the Day

Eurobond

A Eurobond is a bond denominated in any currency other than the home currency of the country or market in which it is issued. Eurobonds are a way for companies to raise funds by issuing bonds in a foreign currency and generally come with the issuing currency suffixed. For example, a Chinese company raising money in USD will issue a euro-dollar bond and if it raises money in Yen, it would be called a euro-yen bond.

Euro-dollar bonds, for example, should not be confused with euro denominated bonds since the former is denominated in USD. The word ‘Euro’ here implies any currency other than the issuer’s home currency. These bonds are issued to entice investors to the currency in which the bond is issued but from a foreign market.

Talking Heads

On Fed’s Mester Backing ‘Methodical’ Rate Hikes, Not a 75 Basis-Point Move

“It’s always good to remember that monetary policy transmits to the economy via expectations and movements in financial markets. So that’s why I kind of favor this methodical approach rather than, you know, a shock of 75 basis points. I don’t think it’s needed for what we’re trying to do with our policy…. When we get to that neutral rate, where policy goes after that is going to really depend on how that policy has affected the economy. So let’s be on this methodical– rather than overly-aggressive path — and then see how policy transmits to the economy.”

On ECB Bond Buys Will Likely End Early in Third Quarter – ECB President Christine Lagarde

The end of bond buying “is very likely to happen in the course of the third quarter with a high probability that it will be early in the quarter if numbers continue to be the way we have seen them”… “If the situation continues as predicated at the moment there is a strong likelihood that rates will be hiked before the end of the year. How much, how many times, remains to be seen”

On the Fed May Not Hike as Much as Market Priced In – ARK’s Cathie Wood

There could be “a surprise in terms of interest rates not going up as much as the market has priced in… We do believe that the Fed is getting lots of messages right now that it should not tighten too much”

On Trillions of Negative-Yielding Bonds Vanish

Rishi Mishra, an analyst at Futures First

“The hawks appear to have more credibility now. So if the ECB is to let the idea float of a July rate hike being alive, that gives markets a license to price closer to 100 basis points of hikes by December.

Frederik Ducrozet, global strategist at Banque Pictet & Cie SA

“The rise in breakeven inflation rates is a key driver of that hawkish talk… Financial conditions never really tightened enough, so the hawks had to become more aggressive for that to be reflected in the rate hike pricing.”

Louis Harreau, rates strategist at Credit Agricole SA

“The hawks are trying to push the ‘July or September or December’ rate hike, so that they are sure to get September”

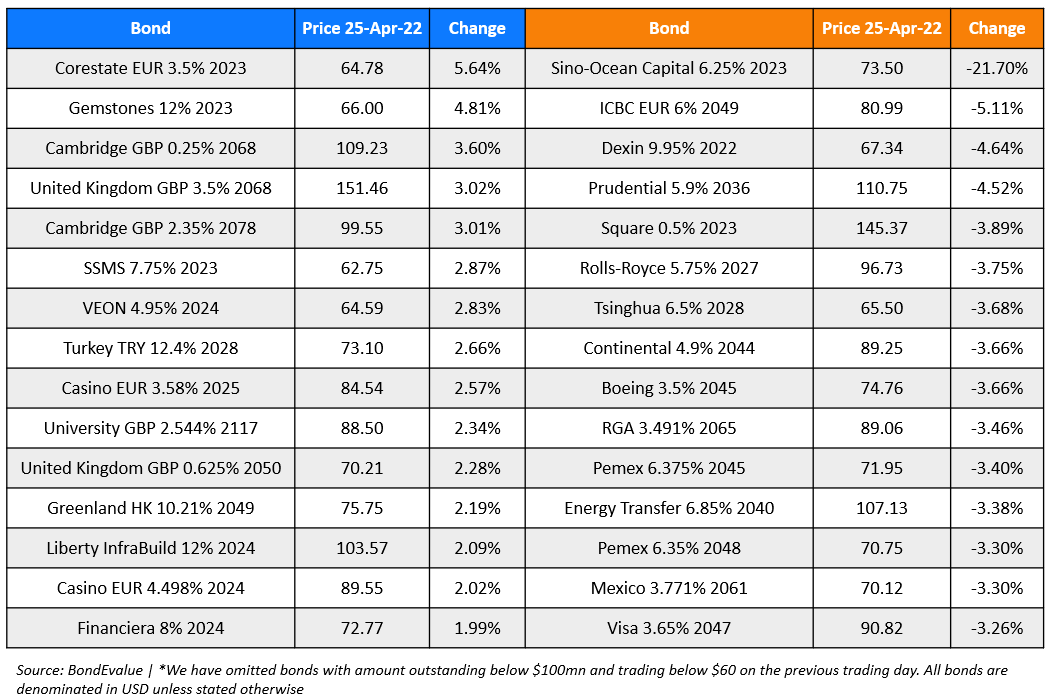

Top Gainers & Losers – 25-Apr-22*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.