We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

August 1, 2022

US equity markets continued its climb on Friday with the S&P and Nasdaq up 1.4% and 1.9% respectively. Sectoral gains were led by Energy up 4.5% and Utilities up 4.3%. US 10Y Treasury yields eased a further 3bp to 2.66%. European markets also ended higher – the DAX, CAC and FTSE were up 1.5%, 1.7% and 1% respectively. Brazil’s Bovespa was up by 0.6%. In the Middle East, UAE’s ADX rose 1% on Friday, and Saudi TASI ended 0.4% higher on Sunday. Asian markets have opened mixed – STI, Shanghai and Nikkei were up 0.9%, 0.2% and 0.6% respectively while HSI was down 0.3%. US IG CDS spreads narrowed 0.8bp and US HY spreads also tightened 0.9bp. EU Main CDS spreads were 4bp tighter and Crossover spreads were tightened by 16.2bp. Asia ex-Japan IG CDS spreads tightened 8.6bp.

Oman’s central bank raised its repo rate by 75bp to 3%, given the OMR’s peg to the dollar. Saudi Arabia’s GDP grew by 11.8% YoY in Q2 on higher energy prices and production. GDP growth was the fastest since 2011. Eurozone inflation in July rose to an all-time high of 8.9% against expectations of 8.7%, and June’s print of 8.6%, on higher food and energy prices.

IBF-STS Course on Digital Assets | 11 Aug 2022 (In-person in Singapore) | 70/90% Funding

%20no%20logo-1.png)

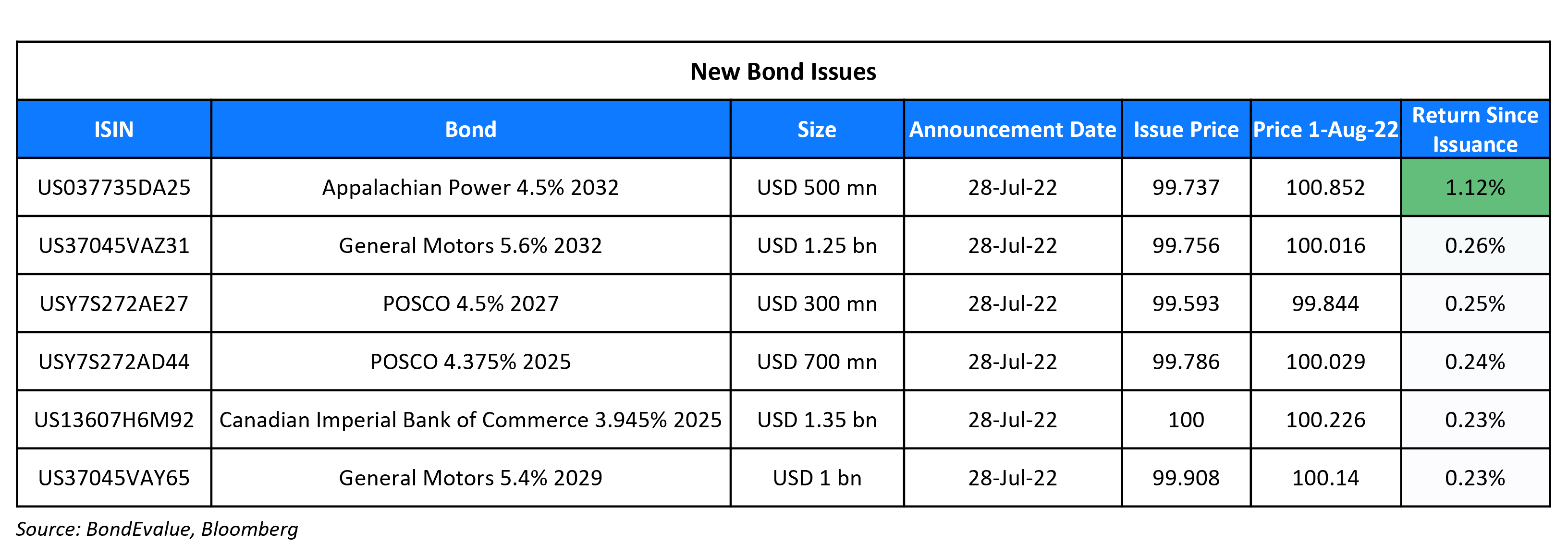

New Bond Issues

- KT Corp $ 3Y @ T+155bp area

- Mianyang Investment $ 3Y @ 6.7%

New Bonds Pipeline

- Johnson Electric hires for $ Senior bond

- NH Investment hires for $ 3Y and/or 5Y Green bond

- Busan Bank hires for $ Social bond

Rating Changes

- Fitch Downgrades Hong Yang and Redsun to ‘CC’ on Increasing Refinancing Risks

- Teva Pharmaceutical Industries Ltd. Outlook Revised To Positive From Stable On Opioid Settlement, Rating Affirmed

- Italian Insurer Allianz SpA Outlook Revised To Stable From Positive On Similar Sovereign Action; ‘A’ Ratings Affirmed

- Outlook On 11 Italian Banks Revised To Stable From Positive Following Similar Action On Sovereign; Ratings Affirmed

Term of the Day

Bear Flattening

Bear flattening refers to a change in the yield curve where short-term rates move up faster than long-term rates, so that the two begin to converge. This phenomenon is widely regarded as a leading indicator for an economic contraction. If the yield curve moves lower and bond prices move lower, it is considered a bear move, while the opposite is a bull move. Typically, short-term rates rise when the market anticipates the central bank to embark on a tight monetary policy, often with the aim of bringing inflation down.

Over the course of H1 2022, the Treasury yield curve initially saw this kind of bear flattening as the Fed Funds rate was hiked 3 times by a total of 150bp. In July, the short term interest rates continued to rise at a faster rate compared to long-term rates, leading to an inversion of the yield curve. This was likely a result of market expectations that the Fed would raise interest rates again amid higher-than-anticipated inflation rates. The Feds ultimately delivered another 75bp rate hike at the FOMC meeting last Thursday. Currently, the yield curve remains inverted with the 2s10s at negative 25bp.

Talking Heads

On Chinese Banks Facing $350 Billion in Losses From Property Crisis

Zhiwu Chen, a professor of finance at the University of Hong Kong Business School.

“Banks are caught in the middle, If they don’t help the developers finish the projects, they would end up losing much more. If they do, that of course would make the government happy, but they add more to their exposure to delayed real estate projects.”

On Powell’s Assessment that the Fed Rate had reached a “neutral setting”

Former US Treasury Secretary Lawrence Summers

“There is no conceivable way that a 2.5% interest rate, in an economy inflating like this, is anywhere near neutral…I don’t see any basis for thinking that either of those statements is a reasonable prediction given what we know…just to get to a neutral posture with respect to inflation we’re going to take unemployment up towards 5, and to help bring down inflation, joblessness would need to climb past that level”

On the Euro Feeling Pressure as the Risk of Recession Increases

Themos Fiotakis, global head of FX & EM Macro Strategy at Barclays Plc.

“In some ways the situation is more dire than 10 years ago, and in others, more benign…It’s less of a deleterious problem for the integrity of the euro as a currency. But economically, growth could prove to be a bigger issue than back then.”

Nicolas Forest, head of global fixed income at Candriam

“Today, the main risk is inflation risk, The most important message was how the ECB can normalize the situation, without creating a debt crisis. The idea now is to avoid something, not to fix something.”

On Australia Hiking Key Interest Rate by 50 Basis Points to 1.85%

Nicolas Forest, head of global fixed income at Candriam

“The RBA is behind the pack…The current cash rate is not appropriate for an economy with an unemployment rate at around a 50-year low and with core inflation running at a 6% annualized pace.”

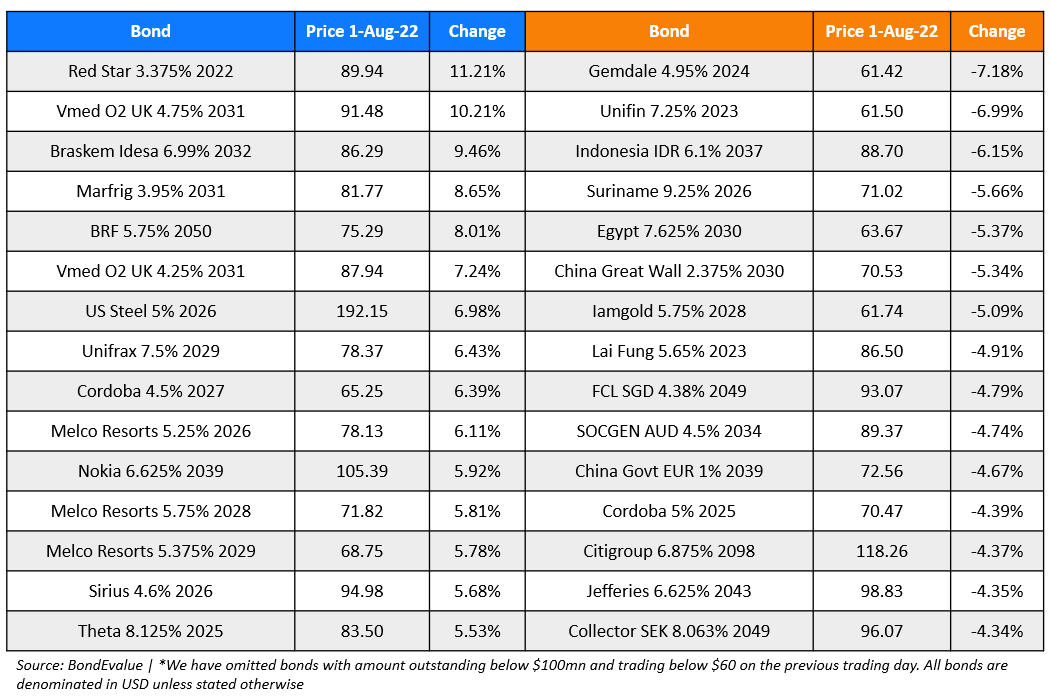

Top Gainers & Losers – 1-August-22*

Other Stories

- Sumitomo Mitsui Profit Jumps 24% on Loan Growth, Weaker Yen

- Aston Martin’s Most Powerful SUV Underpins Second-Half Optimism

- NatWest Shares Rally After Earnings Beat, Special Dividend

- Zambia debt relief pledge clears way for $1.4 billion program, says IMF

- Argentina ‘superministry’ launch lifts bonds, but uncertainty lingers

- Alibaba Added to SEC List of Chinese Firms Facing Delisting

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.