This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

November 4, 2022

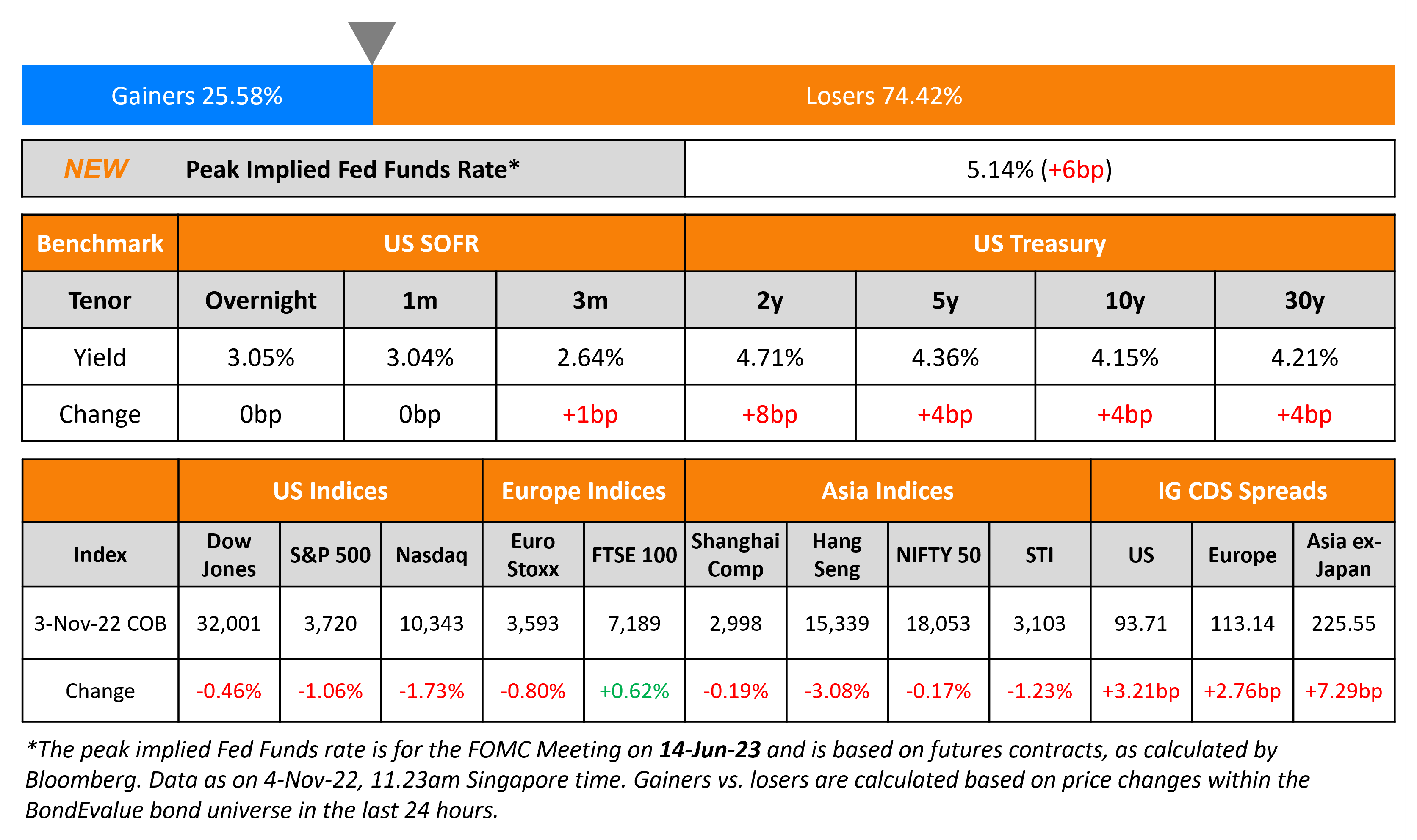

The peak Fed Funds rate moved 6bp higher to touch 5.14% for the June 2023 meeting, as Fed Chairman Powell indicated a possible higher rate in the FOMC meeting on Wednesday. Current probabilities of a 50bp hike in its December meeting stand at 45% and that of a 75bp at 55%. This compares to yesterday’s post-FOMC probabilities of 66% and 34% for a 50bp and 75bp hike respectively. US Treasury yields climbed 6-10bp higher across the curve, led by the short-end. The 2s10s yield curve currently stands at -51bp, after having briefly gone below -58bp yesterday, a four decade low. In the credit markets, US IG CDS spreads widened 3.2bp and HY CDS spreads saw a 17.9bp widening. US equity markets fell on Thursday, with the S&P and Nasdaq down 1.1% and 1.7% respectively.

European equity markets ended broadly lower. EU Main CDS spreads widened 2.8bp and Crossover spreads widened 1bp. The Bank of England hiked its policy rate by 75bp to 3%, its largest rate hike in 33 years. Asian equity markets have opened weaker today. Asia ex-Japan CDS spreads saw an 7.3bp widening with Korean credit markets witnessing some stress. Korean bank perps dropped after an insurer skipped the call option on its dollar perp, the first by a Korean issuer since 2009 (scroll below for details).

%20x%20311px%20(h).jpg)

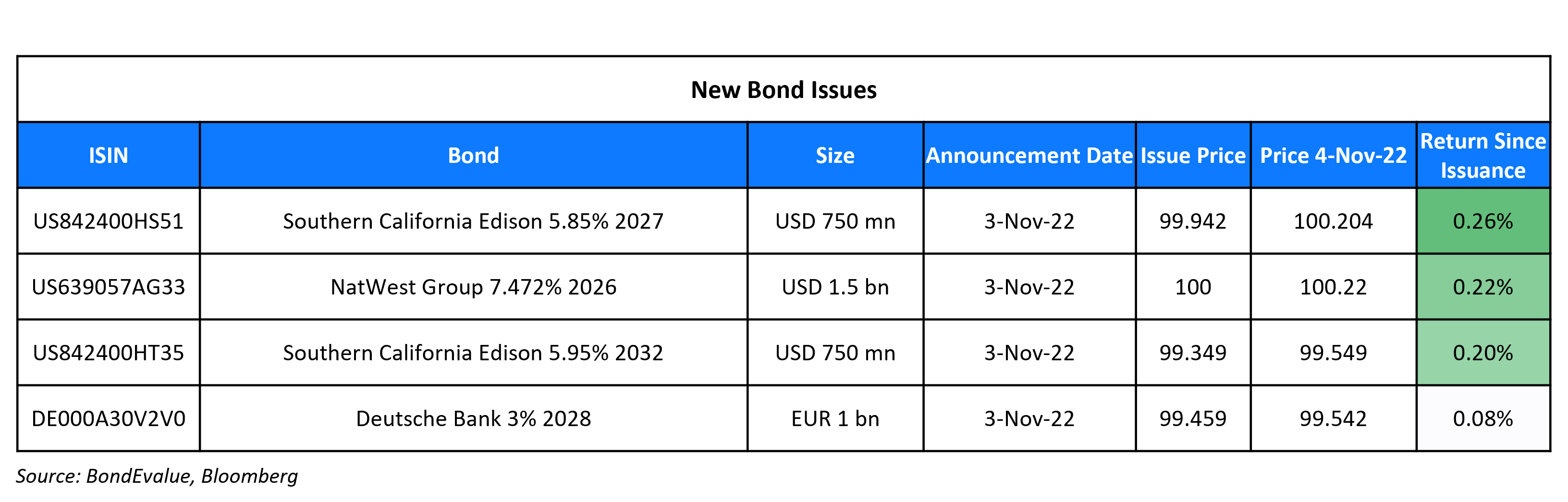

New Bond Issues

NatWest raised $1.5bn via a 4NC3 bond at a yield of 7.472%, 25bp inside initial guidance of T+310bp area. The senior unsecured bonds have expected ratings of A3/BBB/A. Proceeds will be used for general corporate purposes. If not redeemed on the optional call date of 10 November 2025, the coupon resets to the 1Y US Treasury yield plus a spread of 285bp. The new bonds are priced at a new issue premium of 81.2bp vs. its existing 4.8% 2026s (non-callable bonds) that yield 6.66%.

Deutsche Bank raised €1bn via a Long 5Y bond at a yield of 3.113%, 2bp inside initial guidance of MS+10bp area. The mortgage-covered bonds have expected ratings of Aaa, and received orders over €1.6bn, 1.6x issue size.

New Bonds Pipeline

- Korea Investment & Securities hires for $ Green bond

Rating Changes

- Sri Lanka Bonds Downgraded To ‘D’ After Missed Payments; Sovereign Ratings Affirmed

- Diamond Sports Holdings LLC And Subsidiary Downgraded To ‘CCC-‘ On Increased Recession Risks; Outlook Negative

- Moody’s changes the outlook on Qatar to positive, affirms Aa3 rating

Term of the Day

Call Option

A call option gives the buyer of the option the right but not the obligation to buy the underlying instrument at a particular price known as the strike price at expiration. Call options in bonds are in the hands of the issuer where the issuer has an option to redeem the bond before its maturity leading to a cash outflow. Particularly in the case of perpetual bonds, call options are considered important as there is a general assumption that an issuer will call back their perps. However, this need not be the case always as issuer consider factors including their financial position and the revised coupon rate.

Talking Heads

On Wall Street Saying Treasury Buybacks Are a Long Way Off, If at All

Bank of America

Market appeared somewhat disappointed with the lack of clear buyback commitment as the 20-year cheapened 3 basis points on the 10-20-30 fly

Wrightson ICAP

Buybacks are under active consideration, “but not an on active timeline”

RBC Capital Markets

Treasury’s announcement did little to “disabuse us” of the view that any meaningful buyback program is imminent and the dealer survey was likely “more of an exploratory exercise”

On Treasury Yield-Curve Inversion at a Four-Decade Extreme

Priya Misra, global head of rates strategy at TD Securities

“We think that the curve can keep inverting for now since the Fed is likely to keep raising rates and will tolerate some slowing in the economy. This more aggressive than expected hiking path has an unfortunate consequence. The amount of real tightening that we expect now to happen will likely lead the economy to a recession in the second half of 2023.”

On Pound, Long Bonds Tumble as BOE Pushes Back on Peak Rate

Valentin Marinov, head of G-10 currency strategy at Credit Agricole

“The BOE hiked by 75 basis points but revised down its growth and inflation projections, sending a clear signal that the bank rate path expected by the markets ahead of the policy meeting is too high. The outcome contrasts sharply with the hawkish message from Fed Chair Powell yesterday and could trigger a further drop of the pound-dollar rate spread”

Hugh Gimber, global market strategist at JPMorgan Asset Management

“The Bank of England had little choice but to deliver on the market’s expectations of a 75 basis-point hike at today’s meeting… Such a large hike may appear unwarranted given signs that UK activity is already contracting”

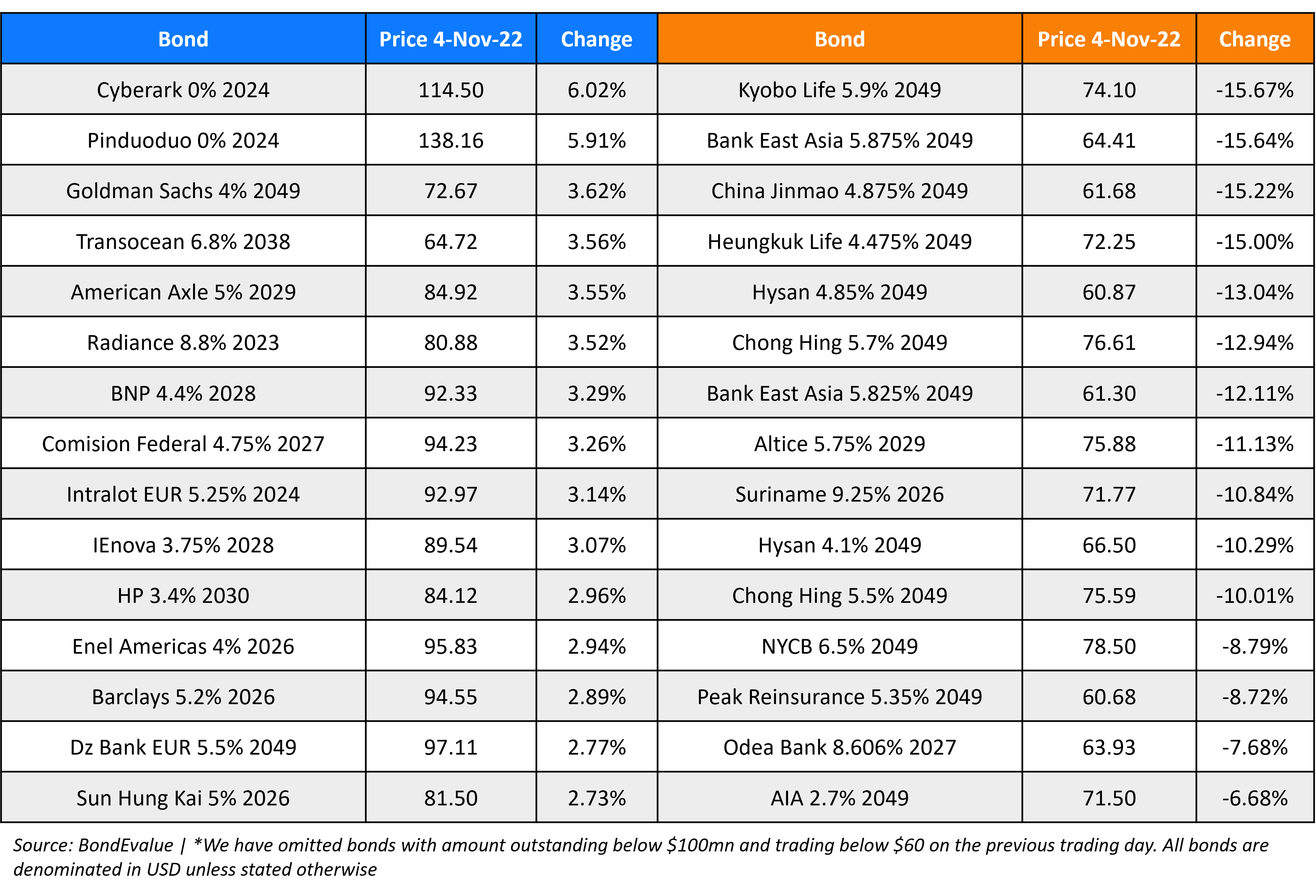

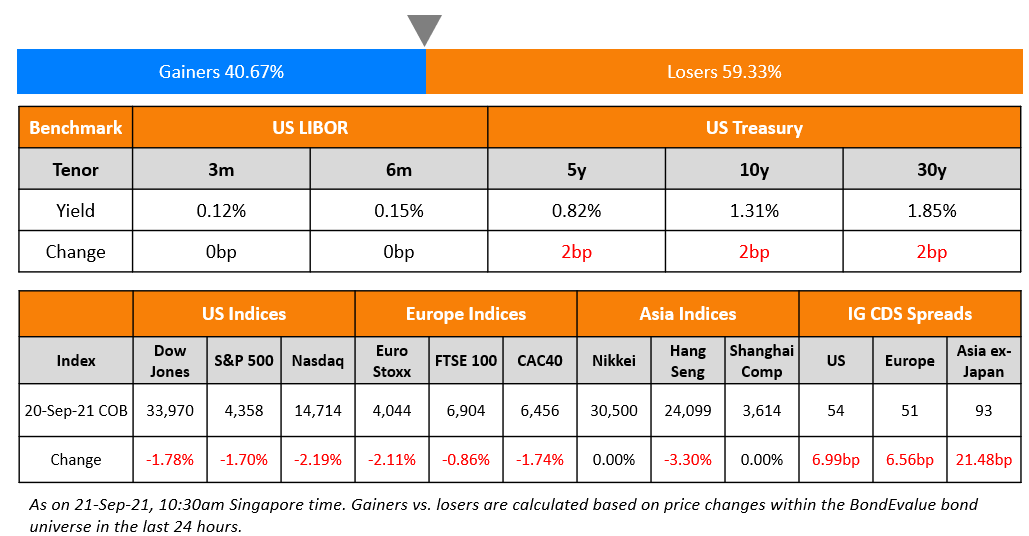

Top Gainers & Losers – 04-November-22*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.