This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

October 6, 2023

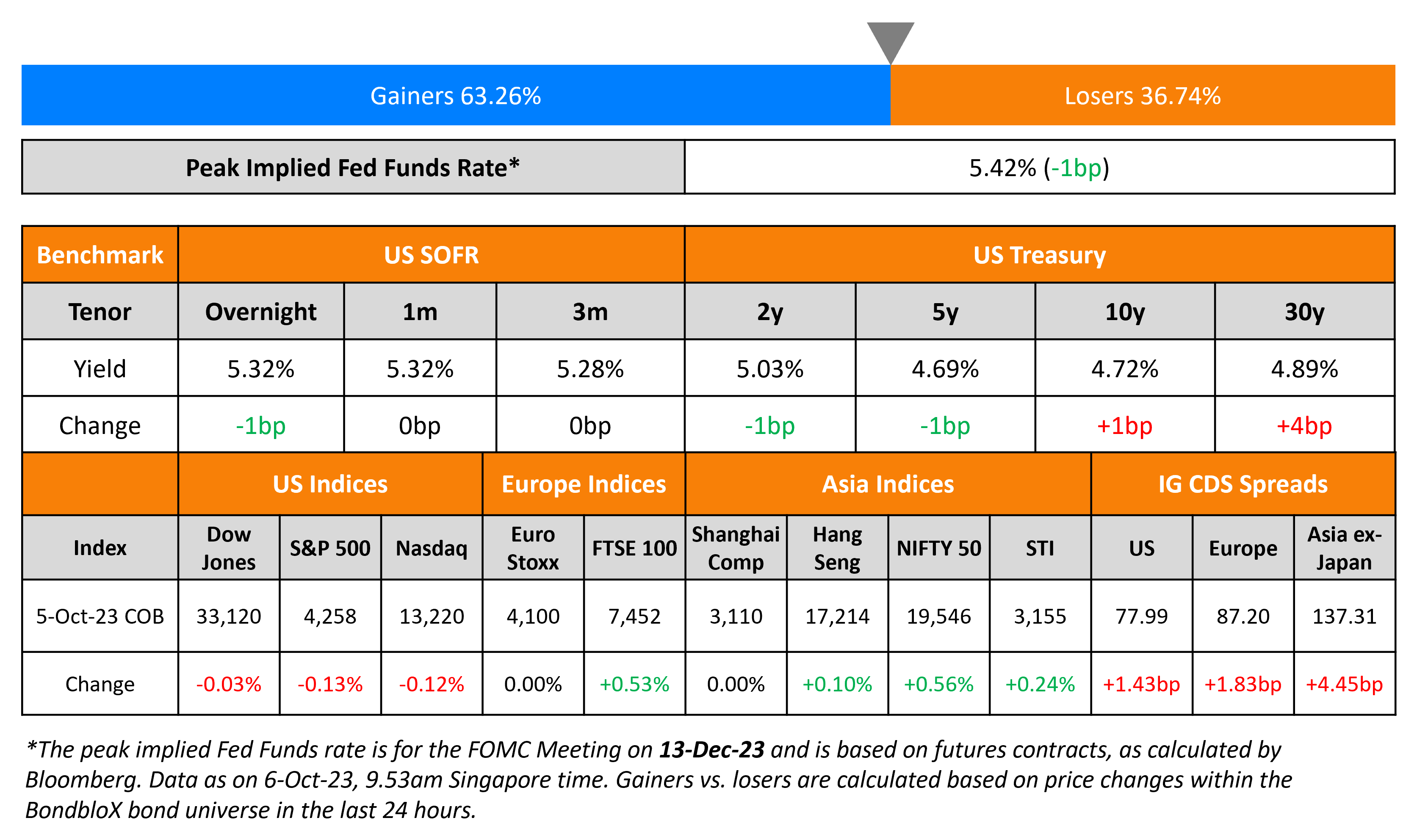

US Treasuries traded stable on Thursday with markets now awaiting the Non Farm Payrolls (NFP) print later today. NFP is expected at 170k and the Average Hourly Earnings (AHE) YoY print is expected to stay unchanged at 4.3%. In credit markets, US IG CDS spreads were 1.4bp wider while HY spreads widened 6.6bp. US equities were marginally lower as S&P and Nasdaq were down ~0.1%.

European equity markets ended mixed. In credit markets, European main CDS spreads were wider by 1.8bp and crossover spreads widened 7.3bp. Asian equity markets have opened higher this morning. Asia ex-Japan IG CDS spreads widened 0.6bp.

New Bond Issues

.png)

Damac raised $300mn via a 3.5Y sukuk at a yield of 8.375%, 12.5bp inside initial guidance of 8.5% area. The bonds have expected ratings of Ba2/BB-, and received orders over $650mn, 2.2x issue size. The new bonds offer a new issue premium of 71.5bp over its existing 7.75% 2026s that yield 7.66%.

Uzbekistan raised $660mn via a 5Y bond at a yield of 8.125%, 50bp inside initial guidance of 8.625% area. The bonds have expected ratings of BB-/BB- (S&P/Fitch), and received orders over $2bn, 3x issue size.

New Bond Pipeline

- Damac Real Estate hires for $ 3.5Y sukuk bond

- Oman Telecom hires for $ 7Y sukuk bond

- Uzbekistan hires for $ 5Y/10Y bond

- Philippines hires for $1bn Retail bond

Rating Changes

- Fitch Upgrades Energy Development Oman to ‘BB+’; Outlook Stable

- BankMuscat Ratings Raised To ‘BB+’ Following Sovereign Upgrade; Outlook Stable

- Moody’s downgrades Egypt’s ratings to Caa1 with a stable outlook, concluding its review

- Fitch Downgrades WeWork’s IDR to ‘C’

- Moody’s downgrades China SCE’s ratings to Ca/C, outlook remains negative

- Fitch Downgrades Petkim to ‘B-‘; Outlook Stable

Term of the Day

Barbell Strategy

A barbell strategy is a fixed income strategy that involves investors buying short-term and long-term bonds, but not medium-term bonds. Thus, the distribution among the two extreme ends of the maturity curve resembles a barbell and thus the name. Investors may choose a barbell strategy given it gives access to higher yield long-term bonds whilst also decreasing risk by holding short-term bonds. This strategy is an active portfolio management approach. Typically, the barbell approach is employed if the yield curve is expected to flatten.

Talking Heads

On Traders Piling on Strong Dollar Bets While Bond Yields March Higher

Jane Foley, head of forex strategy at Rabobank

“Higher for longer, the resilience of the economy, pushing back on rate cuts. The dollar is one that everyone really understands”

Lord Abbett & Co., PM Leah Traub

“It’s not like we’re in 2007. It’s not going to be easy for the Fed to cut given where inflation is. It’s one thing for inflation to go from 4% to 3%, but it’s another to go to 2%”

On Seeing ‘Puzzle’ In Recent Rate Spike – Chicago Fed’s Austan Goolsbee

“I think the puzzle that people are trying to put together is, well, why did it happen in the last three weeks?… if you take a six-month perspective, in a way, I don’t think it’s that much of a puzzle… If there is a credit crunch — if those things materially deteriorate in a way that we haven’t seen, but feared seeing, over the last six months — we will adjust”

On Wild Week for Bond Market Spurring Record Trading in ETFs

Lara Crigger, editor-in-chief at VettaFi

You “have something like TLT, which is hoovering in assets. Investors are trying to set themselves up for whenever rates do start to change and the environment starts to change. They want to have that barbelled approach”

Winnie Cisar, global head of strategy at CreditSights

“The main message is that investors got a bit more worried about the outlook for economic fundamentals and risk assets amid this move in long-end yields. HY spreads had been trading in a tight range for a few months… considering where we started the year”

Chris Gaffney, president of world markets at EverBank

“There is no consensus view right now, put it that way. You see some people taking the stance that the Fed’s done”

On 6% Yield Within Reach – JPMorgan Cash-Hoarding Bond Manager, William Eigen

“Every week that passes by without a recession is really bad news for fixed-income folks”… To abandon cash, which yields above 5%, he wants to see longer-term yields exceeding their short-term counterparts… it’s possible that 10Y yields may reach 6%, last seen in 2000”

Top Gainers & Losers- 06-October-23*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.