This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

April 11, 2023

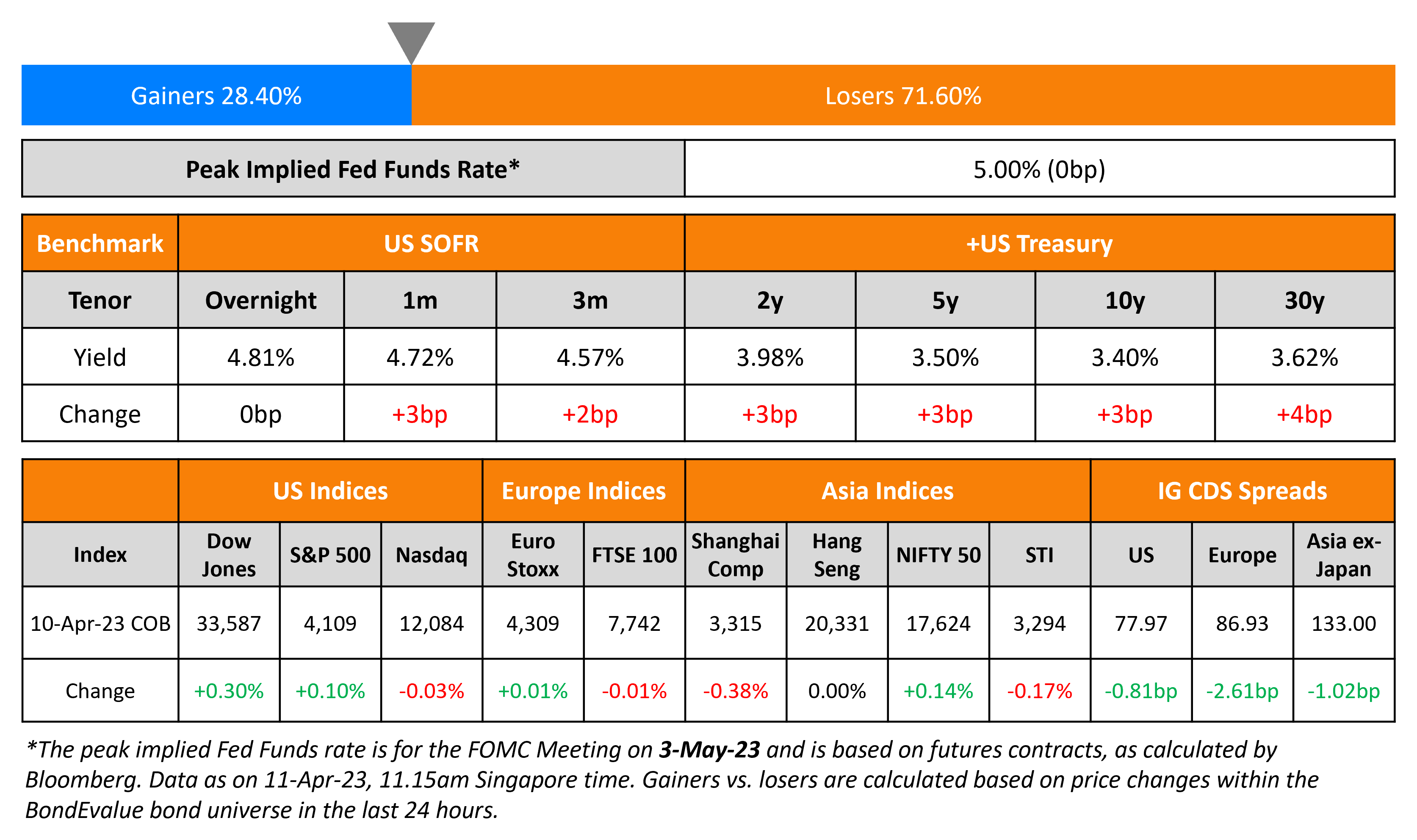

US Treasury yields were slightly higher yesterday by 3-4bp across the curve. The peak fed funds was unchanged at 5%. Meanwhile, the probability of a 25bp rate hike in the May meeting continued to rise, now at 72% as per the CME’s maximum probabilities as compared to 68% yesterday. US IG CDS spreads tightened 0.8bp while HY CDS spreads widened 1.4bp respectively. US equity indices moved sideways as the S&P was just 0.1% higher and Nasdaq ended almost unchanged.

European equity markets ended mixed. European main CDS spreads tightened by 2.3bp and Crossover spreads were 13bp tighter. Asia ex-Japan CDS spreads tightened by 1bp. Asian equity markets have opened higher this morning. The BoJ’s new governor Kazuo Ueda, said that yield curve control (Term of the Day, explained below) and negative interest rates are appropriate amid the current economy, and that any significant changes to its monetary policy framework currently may be unlikely.

.

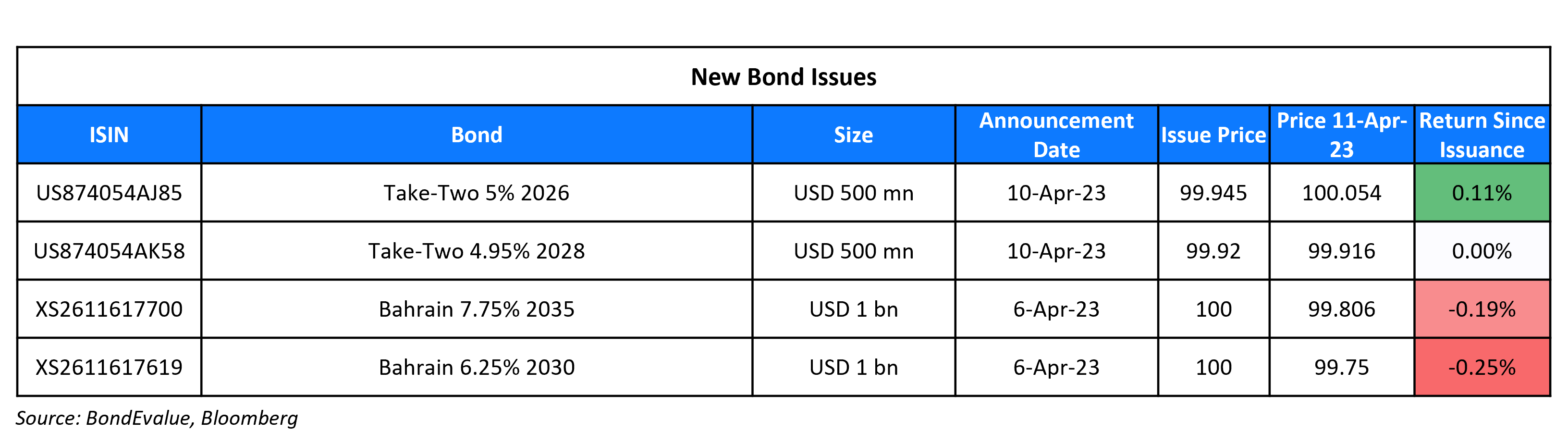

New Bond Issues

New Bonds Pipeline

- Kookmin Bank hires for $ 3Y and/or 5Y bond

Rating Changes

- Fitch Downgrades Lippo Malls Indonesia Retail Trust to ‘CCC-‘

Term of the Day

Yield Curve Control

Yield Curve Control (YCC) is a policy that targets long term interest rates by buying or selling long term bonds to keep the interest rate from rising above it’s target. This is a measure taken to stimulate economic growth. Yield curve controls are also sometimes referred to as Interest Rate Pegs. The Bank of Japan (BOJ) is famous for having a YCC policy in place where they peg the yield on 10-year Japanese Government Bonds (JGB) to fight persistently low inflation.

Talking Heads

On Fed might not need May hike as economy slows – BlackRock CIO Fixed Income, Rick Rieder

“Last Friday’s employment report, while clearly not alarming in any way, allows investors to see more clearly through to what should be a tangibly slower set of economic condition… “Presumably, this will also see a cessation of Fed policy rate hikes after one more possible hike at the May meeting, although it’s also possible the Fed is done already”

On Goldman Seeing ‘High Return’ Potential in Chinese Property Bonds

Salman Niaz, head of Asia fixed income at GSAM

“The high-return opportunity in our view exists today in private developers — both in companies that have not defaulted but also in some companies that have… Our view is that most of the defaults are done. There may be a few more defaults or distressed exchanges, but systemically most of the pain is behind us… We like the China reopening theme and we also think the prospects for the China property sector are positive… have to be pretty selective because not all developers are cut from the same cloth”

On the credit crunch that the Fed fears may already be taking shape

Jeffrey Haley, the CEO of American National Bank and Trust Company

“My rule of thumb was whatever you did last year you will probably do half this year. Based on current events … I now think it gets cut in half again.”

Cleveland Fed President Loretta Mester

“Survey data is going to be very important because it’s going to give us a sense of whether financial institutions are pulling back even more on their credit standards”

On no escape from the zero lower bound for top central banks – IMF

“When inflation is brought back under control, advanced economies’ central banks are likely to ease monetary policy and bring real interest rates back toward pre-pandemic levels… natural rates of interest will remain low in advanced economies or decline further in emerging markets”

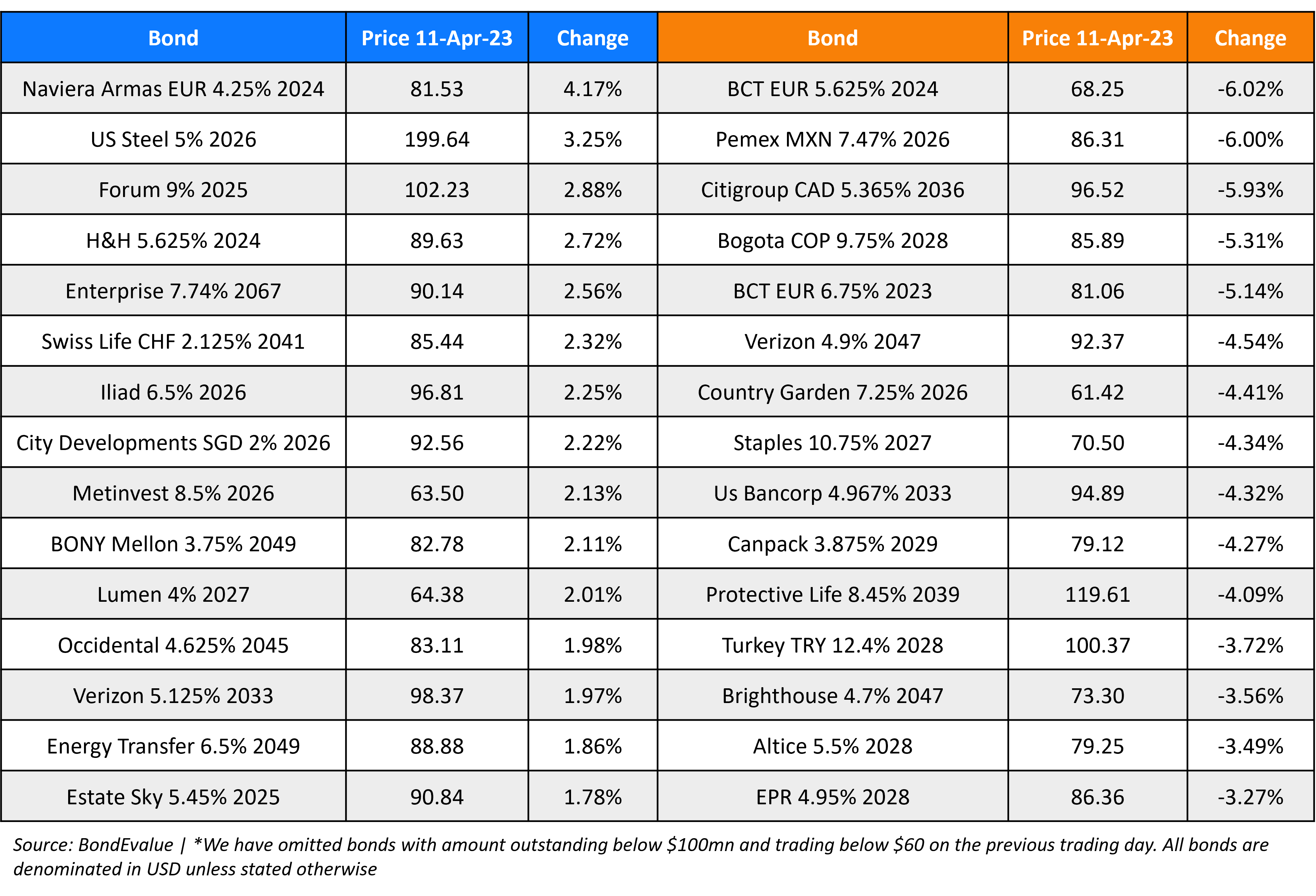

Top Gainers & Losers –11-April-23*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.