This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Huarong International Says It Had a Profitable Q1; Bonds Lower as Restructuring Concerns Remain

April 21, 2021

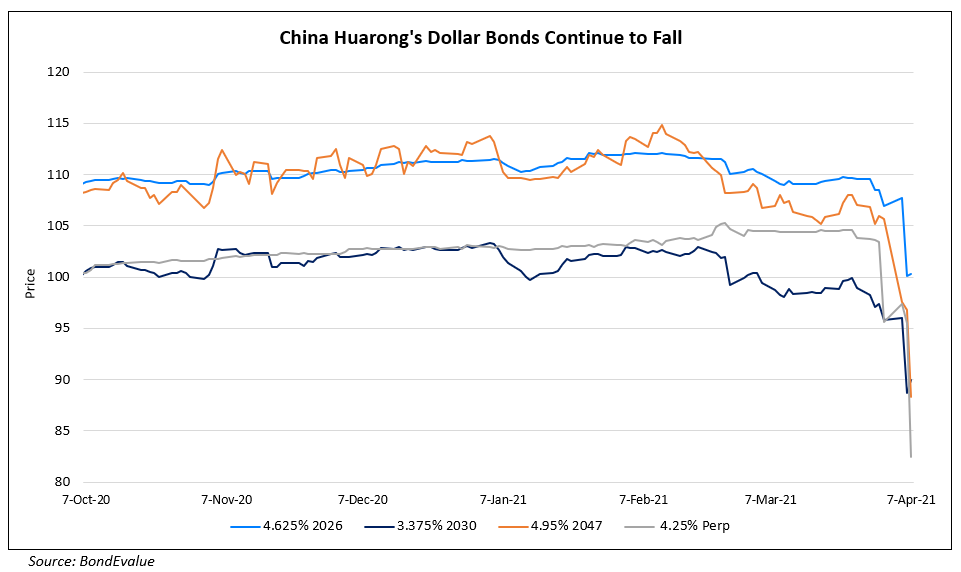

Confusing signals on China Huarong Asset Management Company (CHAMC) continue to plague its bonds days after the regulator CBIRC announced that the company has adequate liquidity. China Huarong International Holdings, its offshore financing arm said it returned to profit in Q1 2021 and laid a “solid” foundation for transformation. The unit said it was focusing on cutting risk exposure and ensuring liquidity. The news comes a few hours after Bloomberg cited credit intelligence provider Reorg Research reporting that regulators were considering options including restructuring debt of Huarong International. Last week, CHAMC said they were focusing on cutting costs and selling non-core assets, but made a special mention that Huarong International would continue to be retained. “There’s very little clarity from China Huarong and regulators over the fate of offshore investors so the bonds are still vulnerable to big swings,” said Owen Gallimore, head of credit strategy at ANZ Singapore.

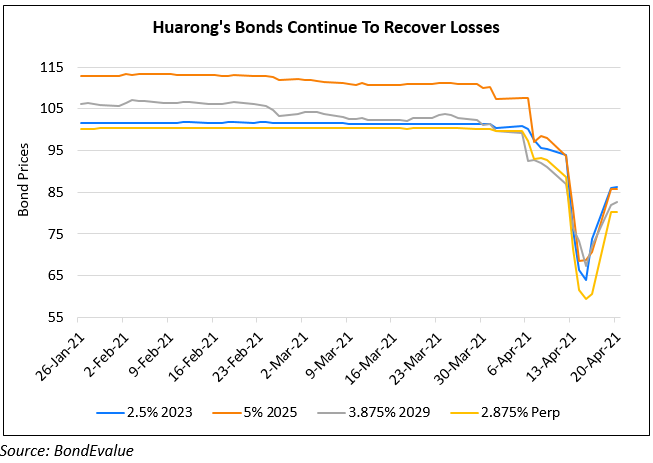

Huarong’s dollar bonds are again weaker today – its 5.5% 2025s are down 5 cents to 82.4 cents on the dollar, yielding 11.4% and its 3.75% 2022s are down 4.5 to 86, yielding 19.7%. Huarong’s 4.25% Perp was the most affected, down 9.2 points to 62.7, yielding 10.4%.

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.