This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Debt Ceiling Impasse Continues; Macro; Rating Changes; New Issues; Gainers and Losers

May 25, 2023

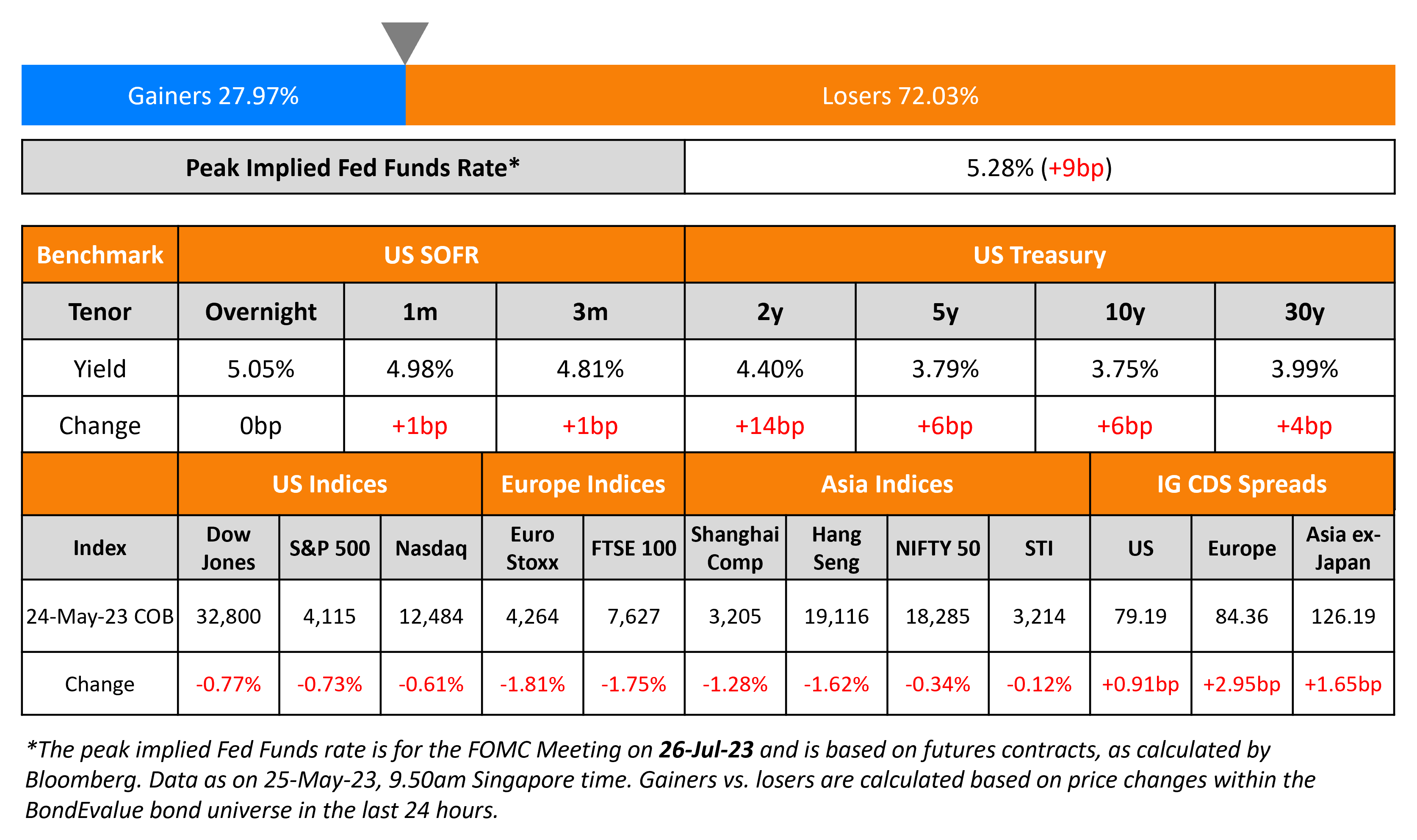

US Treasury yields jumped across the board led by the 2Y up the most, by 11bp. With a lack of clear progress in US debt ceiling talks, uncertainty on the ability to reach a deal within the June deadline has only increased. Short-dated T-Bills mainly maturing June 1 and June 6 were extremely volatile, having topped 7% at one point yesterday. These bills were about 400bp higher than the T-bills maturing on May 30. Fitch has now placed USA’s sovereign AAA ratings on ‘Rating Watch Negative’.

The FOMC’s May meeting minutes came out yesterday and were considered to be relatively dovish – policymakers believed the case for further tightening had become “less certain”. However, the minutes also suggested they are not yet ready to call an end to their battle against stubborn inflation. The peak Fed Funds Rate moved 9bp higher to 5.28% with markets expecting a 67% chance of a status quo and thereby a 33% chance of a 25bp hike at the Fed’s next meeting in June. Equity indices closed lower with the S&P and Nasdaq down 0.6-0.7%. US IG CDS spreads widened by 0.9bp and HY CDS spreads widened by 7.6bp.

European equity markets ended lower too. European main CDS spreads were 3bp wider and crossover CDS spreads were 13.5bp wider. Asia ex-Japan CDS spreads also widened by 1.7bp. Asian equity markets have opened lower today.

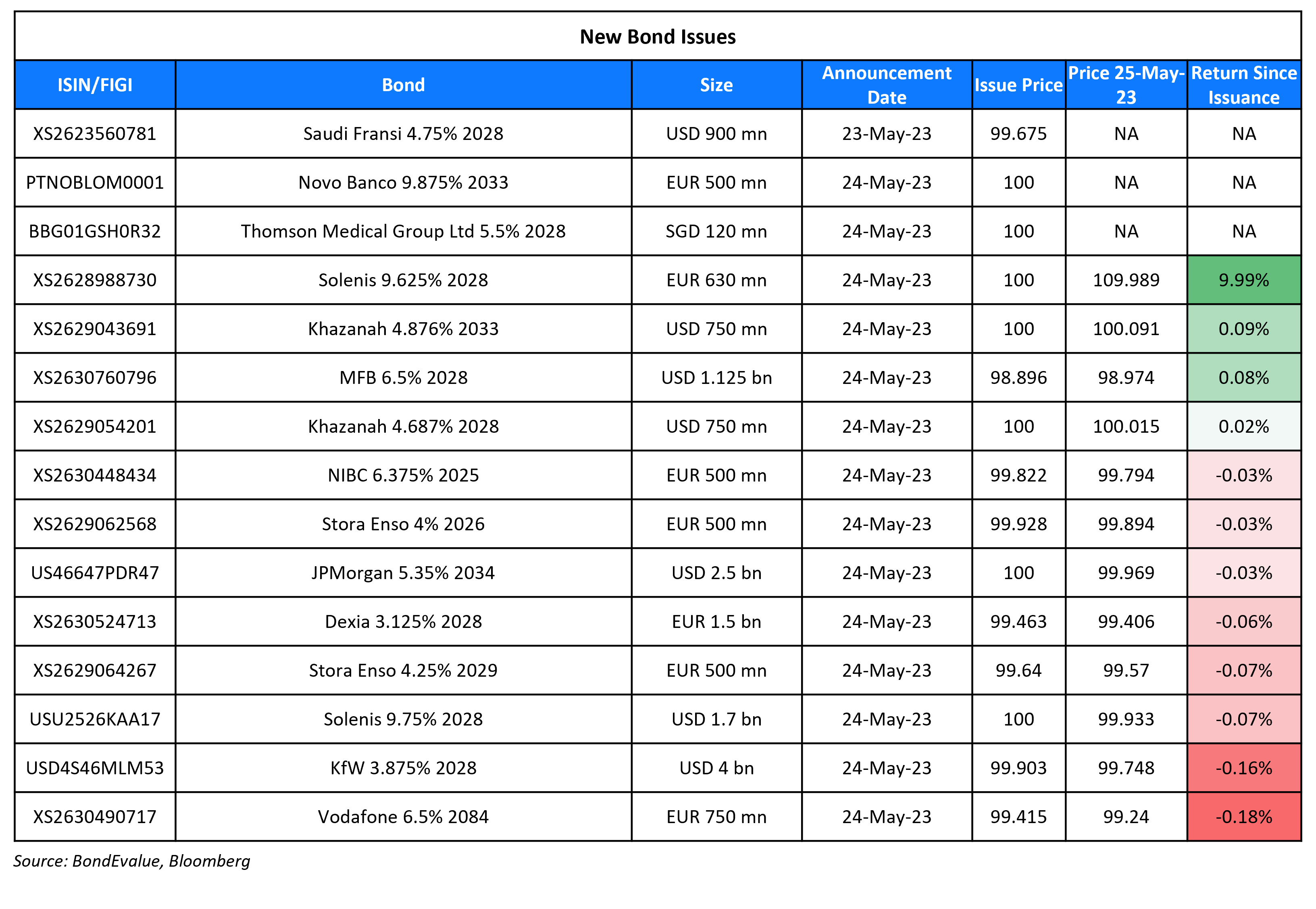

New Bond Issues

Vodafone raised €750mn via a 61.25NC6.25 Hybrid bond at a yield of 6.625%, 25bp inside initial guidance of 6.875%. The bonds have expected ratings of Ba1/BB+/BB+, and received orders over €1.7bn, 2.3x issue size. Proceeds will be used for general corporate purposes, including the refinancing of existing indebtedness, which may include the repurchase via tender offer of Vodafone’s €2bn 3.1% 2079s with first call date on 3 October 2023 and $1.3bn 6.25% 2078s with first call date on 3 July 2024. The bonds have a change of control put (CoC 101), a 75% clean-up call and a make whole call at the benchmark rate i.e., Germany 0% 2029s plus 50bp (MWC B+50).

Thomson Medical Group raised S$120mn via a 5NC1 bond at a yield of 5.5%, 25bp inside initial guidance of 5.75% area. The senior unsecured bonds are unrated. Proceeds will be used for general corporate purposes, including refinancing of borrowings, financing potential acquisitions, strategic expansions, general working capital, capex expenditure and other investments of the group. Private banks received a 20-cent concession.

Khazanah raised $1.5bn via a two-part deal. It raised $750mn via a 5Y sukuk at a yield of 4.687%, 42bp inside initial guidance of T+135bp area. It also raised $750mn via a 10Y bond at a yield of 4.876%, 42bp inside initial guidance of T+160bp area. Proceeds from the 5Y sukuk will be used to fund Shariah-compliant general investments and/or refinancing of borrowings. Proceeds from the 10Y bond will be used for general investments, refinancing of borrowings and working capital requirements. The senior unsecured notes have expected ratings of A3/A-. The 5Y sukuk received orders over $4.9bn, 6.5x issue size and the 10Y notes received orders over $5.9bn, 7.9x issue size. For the 5Y sukuk, fund managers were allocated 74%, insurers and public institutions 11%, banks 9% and others 6%. For the 10Y bonds, fund managers were allocated 76%, insurers, pension funds and sovereign wealth funds 10%, banks 8% and others 6%. Investors from APAC took more than 73% of the deal, followed by EMEA taking approximately 25% and offshore US taking the remainder.

JP Morgan raised $2.5bn via a 11NC10 bond at a yield of 5.35%, 27.5bp inside initial guidance of T+190bp area. The senior unsecured bonds have yet to be rated.

Saudi Fransi raised $900mn via a 5Y Sukuk bond at a yield of 4.824%, 25bp inside initial guidance of T+130bp area. The bonds have expected ratings of A-/A- (S&P/Fitch).

New Bonds Pipeline

- BGK hires for $ 10Y bond

- GS Caltex hires for bond

Rating Changes

- Bed Bath & Beyond Inc. Ratings Discontinued

- Pitney Bowes Inc. Downgraded To ‘BB-‘ From ‘BB’ On Persistent Profit Shortfalls In Ecommerce Business; Outlook Stable

- Fitch Places United States’ ‘AAA’ on Rating Watch Negative

Term of the Day

On-the-run Bonds

On-the-run bonds refer to the most recently issued Treasury bonds while off-the-run bonds refer to older Treasury bonds of the same issuer. On-the-run bonds are generally more liquid and therefore trade at a slight premium in price to off-the-run bonds, known as the ‘liquidity premium’. Hence, in volatile markets where liquidity becomes key, on-the-run bonds are preferred.

Talking Heads

On Flexibility Being Key in Interest-Rate Calls – Fed’s Bostic

“We’re going to let the data guide us, and we don’t want to be locked into any particular movement…. Don’t get locked into anything; let the data come in, and then make a judgment after that… The policies that we’ve done, the tightening that we’ve done, is just starting to show up into the economy”

On Fed agreeing need for more hikes after May meeting being ‘less certain’

“Several participants noted that if the economy evolved along the lines of their current outlooks, then further policy firming after this meeting may not be necessary… many participants focused on the need to retain optionality

Fed Governor Christopher Waller

“Whether we should hike or skip at the June meeting will depend on how the data come in over the next three weeks… we need to maintain flexibility on the best decision to take in June”

On Debt-Ceiling Drama Has Some T-Bills Trading Like Junk Bonds – CreditSights analysts

“The least-loved T-bills have discount yields that resemble the effective yields of several short-dated high-yield bonds.. negotiations appear to be at another impasse at present as discussions have been stop-and-start for several weeks now… difficult historically to predict exactly when there will be a breakthrough in negotiations… likelihood of an additional ratings downgrade [if there is no resolution by end of the week]”

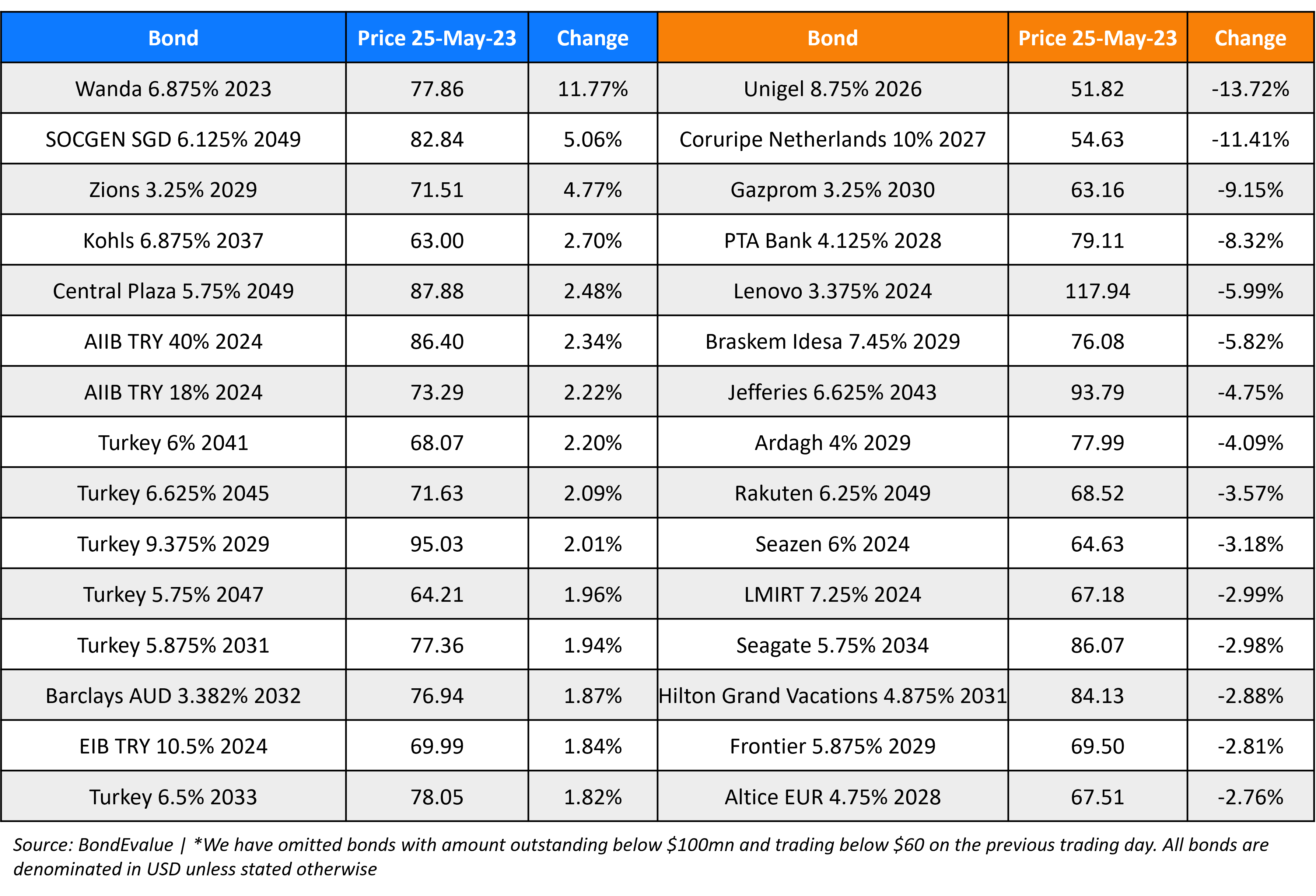

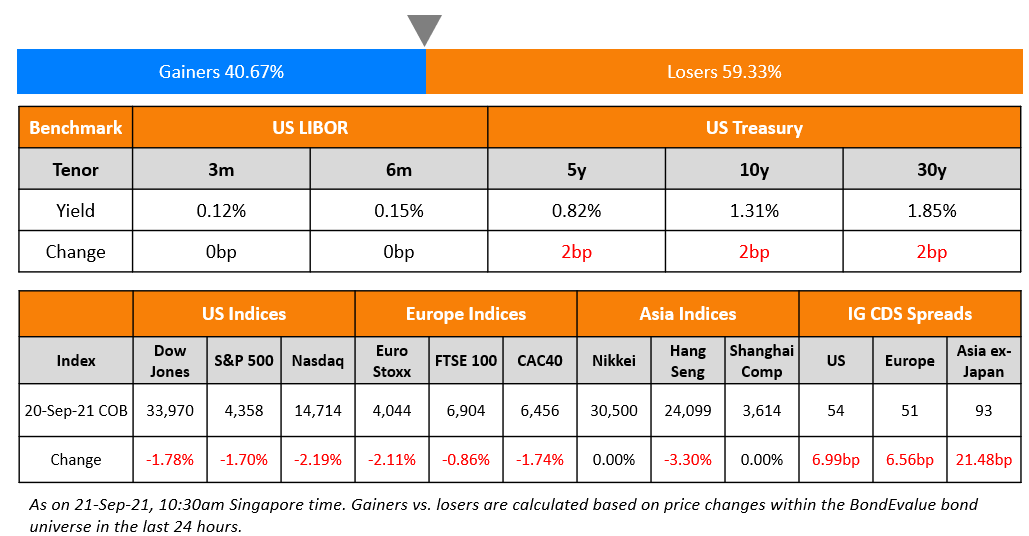

Top Gainers & Losers – 25-May-23*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.