This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

China Launches $ Bond; Macro; Rating Changes; New Issues; Talking Heads; Top Gainers and Losers

October 19, 2021

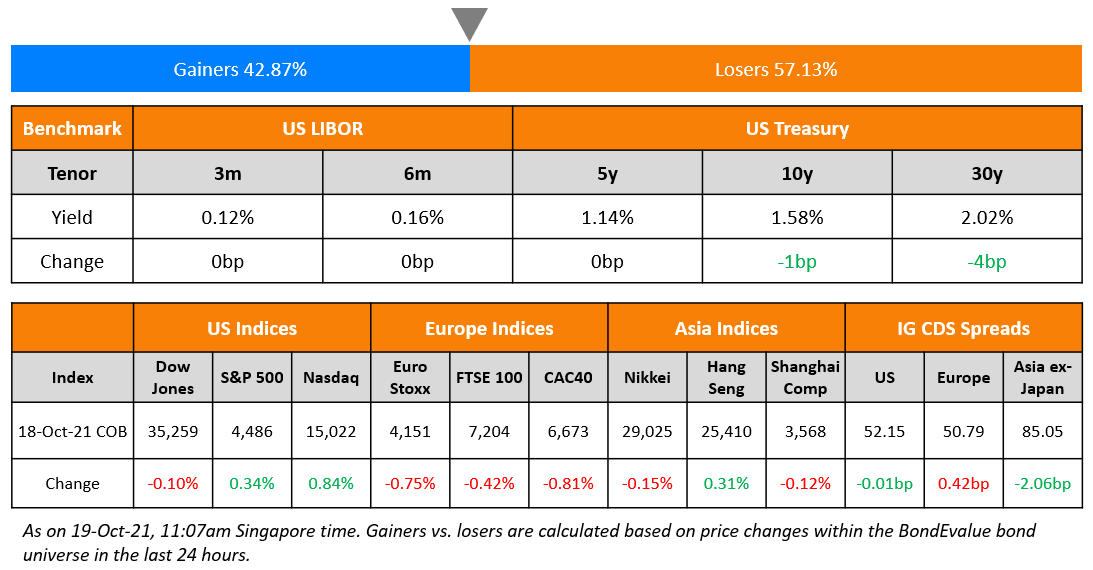

Wall Street saw another move higher with the S&P and Nasdaq up 0.3% and 0.8% as the risk-on sentiment continued. Most sectors ended in the green led by Consumer Discretionary and IT, up 1.2% and 0.9% respectively. US 10Y Treasury yields were flat at 1.58%. European stocks meanwhile moved lower with the DAX, CAC and FTSE down 0.7%, 0.8% and 0.4% respectively. Brazil’s Bovespa ended 0.2% lower. In the Middle East, UAE’s ADX was 0.7% higher and Saudi TASI was down 0.1%. Asian markets have started strongly – Shanghai, HSI, Nikkei and STI are up 0.6%, 1.5%, 0.5% and 0.7% respectively. US IG and CDS spreads were flat and HY CDS spreads were 0.7bp wider. EU Main CDS spreads were 0.4bp wider and Crossover CDS spreads were 2.1bp wider. Asia ex-Japan CDS spreads tightened by 6.4bp.

US Industrial Production for September dropped 1.3% MoM vs. forecasts of a 0.2% rise. Similarly, Manufacturing Production also fell in September, down 0.7% MoM vs. forecasts of a 0.1% rise.

Exclusive Webinar on The Future of Bond Trading | 27 October at 5pm SG/HK

New Bond Issues

-

China $ 3/5/10/30Y at T+35/45/55/85bp area

-

Chengdu Hi-Tech Investment Group $ 5Y at 3% area

-

Rudong County Jinxin Transportation Engineering $ 3Y at 2.75% area

.png)

Goldman Sachs raised $9bn via a jumbo five-tranche deal. It raised:

- $2bn via a 3NC2 bond at a yield of 0.925%, 20bp inside the initial guidance of T+70bp area. The bonds priced 0.5bp tighter than its older 4% bonds due 2024

- $450mn via a 3NC2 floater at a yield of 0.54% or SOFR+49bp vs. initial guidance of SOFR-equivalent

- $3.25bn via a 6NC5 bond at a yield of 1.948%, 22bp inside the initial guidance of T+100bp area

- $300mn via a 6NC5 floater at a yield of 0.91% or SOFR+92bp vs. initial guidance of SOFR-equivalent

- $3bn via a 11NC10 bond at a yield of 2.65%, 15bp inside the initial guidance of T+120bp area. The bonds priced 11bp wider than its older 1.992% bonds due 2032.

The bonds have expected ratings of A2/BBB+. Proceeds will be used for general corporate purposes.

GuocoLand raised S$300mn via a 5Y bond at a yield of 3.29%, 21bp inside the initial guidance of 3.5% area. The bonds are unrated, and received orders over S$400mn, 1.3x issue size. The bonds will be issued by GLL IHT and guaranteed by GuocoLand. Private banks and corporate investors bought 67% of the deal, while fund managers and banks bought 33%. Singapore accounted for 96% while the remaining 4% went to others.

Korea Development Bank raised $1.5bn via a three-tranche deal. It raised:

- $700mn via a 3.25Y green bond at a yield of 0.889%, 25bp inside the initial guidance of T+40bp area. The new bonds are priced 36.1bp tighter to its existing (non-green) 1.25% 2025s that yield 1.25%

- $500mn via a 5.5Y bond at a yield of 1.475%, 25bp inside the initial guidance of T+55bp area

- $300mn via a 10Y bond at a yield of 2.052%, 25bp inside the initial guidance of T+70bp area. The new bonds are priced 11.2bp wider to its existing (non-green) 1.625% 2031s that yield 1.94%.

The bonds have expected ratings of Aa2/AA/AA–. Proceeds of the green note will be allocated to financing and/or refinancing eligible green projects under the Korean policy bank’s sustainable bond framework, whereas proceeds for the non-green notes will be used for general operations, including extending foreign currency loans and repayment of maturing debt and other obligations.

ASB Bank raised $1.2bn via a two-tranche deal. It raised $700mn via a 5Y bond at a yield of 1.708%, 25bp inside the initial guidance of T+80bp area, and $500mn via a 10Y bond at a yield of 2.486%, 15bp inside the initial guidance of T+105bp area. The bonds have expected ratings of A1/AA– (Moody’s/S&P). Proceeds will be used for general corporate purposes.

Huikai International Investment raised $45mn via a 364-day bond at a yield of 3.8%, unchanged from initial guidance. The bonds are unrated and guaranteed by ultimate parent company Wuxi Huishan Hi Tech and its Hong Kong subsidiary Huikai Hong Kong Economic Development. Wuxi Huishan Hi Tech is wholly owned by the Wuxi Huishan Economic Development Zone SASAC in China.

Clover Aviation Capital decided against a 3Y bond deal, which had a final guidance of T+205bp and received orders over $425mn. The bonds had expected ratings of Baa1 (Moody’s). Proceeds were to be used for general purposes including capital expenditure and debt repayment. The bonds were planned to be issued by wholly owned subsidiary CAFC Taurus Company and guaranteed by Hong Kong aircraft lessor Clover Aviation. Mizuho Bank had provided a keepwell and liquidity support deed. This is the first investment grade rated bond deal from APAC to be pulled since IRFC cancelled a two-tranche deal in March. However, IFR notes that some investment grade rated issuers have dropped specific tranches since then (like Country Garden’s cancelled 10Y tranche in May).

New Bond Pipeline

- IOI Corp hires for $ bond alongside tender offer

- DBS hires for € 5Y bond

- TSMC hires for $ bond

- KB Securities hires for $ bond

- Indofood CBP Sukses Makmur hires for $ 10.5/30.5Y bond

- Hunan Xiangjiang New Area Development Group hires for $ bond

- Muang Thai Life hires for $ tier 2 bond

- Hualu Holdings hires for $ debut bond

- Hibiscus Petroleum hires for $ 5NC2 bond

Rating Changes

- Moody’s downgrades Greenland Holding’s and Greenland HK’s ratings; places ratings on review for downgrade

- Moody’s downgrades Kaisa to B2/B3; places ratings on review for further downgrade

- Moody’s downgrades Guangzhou R&F to B3 and R&F HK to Caa1; outlook negative

- Moody’s downgrades Yango to B2/B3; changes outlook to negative

- Moody’s downgrades Golden Wheel to Caa1; outlook negative

- Moody’s affirms Zhongliang’s B1 rating; changes outlook to stable

- Moody’s affirms Jiayuan’s B2/B3 ratings, changes outlook to stable

Term of the Day

Stagflation

Stagflation refers to a period of (stag)nant economic growth and high in(flation). It is an economic phenomenon when economic growth is stagnant and the unemployment rate and inflation are high. Stagflation is most commonly caused by supply shocks leading to higher commodity prices or monetary policies that increase money supply in the economy too quickly. An example of stagflation was in the US during the 1970s, when high inflation and high unemployment was at its peak on the back of a surge in commodity prices. Generally. monetary and fiscal policies are not effective at solving economic problems related to a supply side shock, hence it is tougher to get through a period of stagflation.

Reuters reports that several Worries that several high-profile bond market investors believe that risks regarding the US economy heading into stagflation are overblown.

Talking Heads

On Markets Being “Addicted” to Central Bank Stimulus – Gugenheim Partners’ CIO Scott Minerd

“For the time being we’re just addicted to this…Central banks are functioning in a role that they were never designed to do. Central banks are now running the markets.”

“We believe the Fed’s rate hike path will be shallower than the current market pricing. Clearly there is a very active debate here given the high levels of inflation we are seeing… It will be with us for some time. But we believe it will slowly ease…We will see yields rising over time in part because we believe they are at the wrong level to begin with given the level of economic activity we have seen. So there will continue to be adjustment higher in interest rates albeit not as violent as what we’ve seen in the last two weeks.

On Lehman Brothers May Still Cash In on Its Own Big Short From 2009

John Williams, a partner at Milbank LLP

“Any time the underlying instruments are unusual and illiquid, this kind of dispute can arise. There can be very big differences between what one person thinks the contract is worth versus another.”

Julia Lu, a partner at law firm Ashurst

“Everybody knows that the market-quotations framework is great, except when it doesn’t work. When there is a major market dislocation, you may not be able to get a quote anywhere because nobody’s willing to look at your trades.”

Andrew J. Rossman of Quinn Emanuel Urquhart & Sullivan

“Nearly half of the subprime-mortgage loans underlying these indices were already more than 60 days delinquent, in bankruptcy, in foreclosure, or owned by a lender after a failed foreclosure auction.”

On Turkish lira at new low with little reprieve in sight

Commerzbank Analysts

“In the end the decisions on monetary policy are no longer taken by the central bank itself but are taken in the President’s Palace”

SocGen Analysts

“There is no longer any point to ascribing traditional economic arguments in considering the (central bank’s) likely course of action”

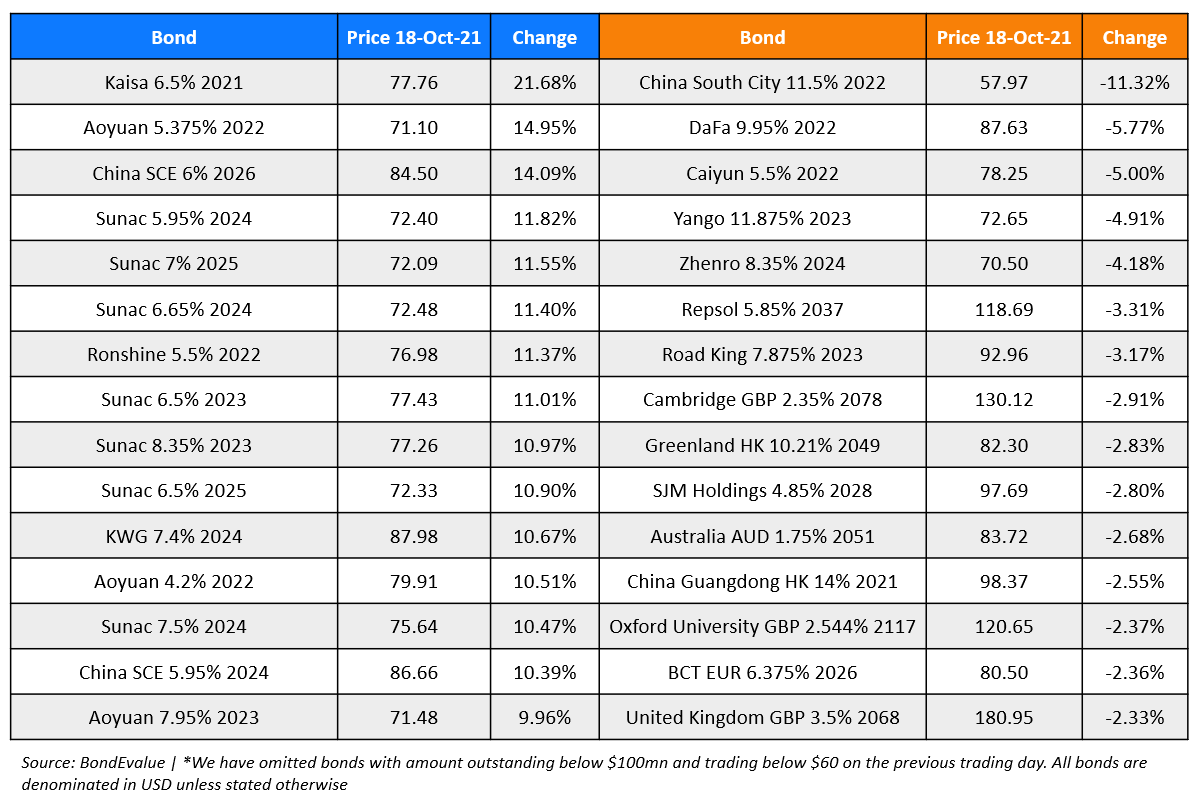

Top Gainers & Losers – 19-Oct-21*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.