This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

75% $ Bonds Traded Up in Q3; American Air Downgraded; Moody’s Says Asian HY Covenant Quality at All Time Low

October 1, 2020

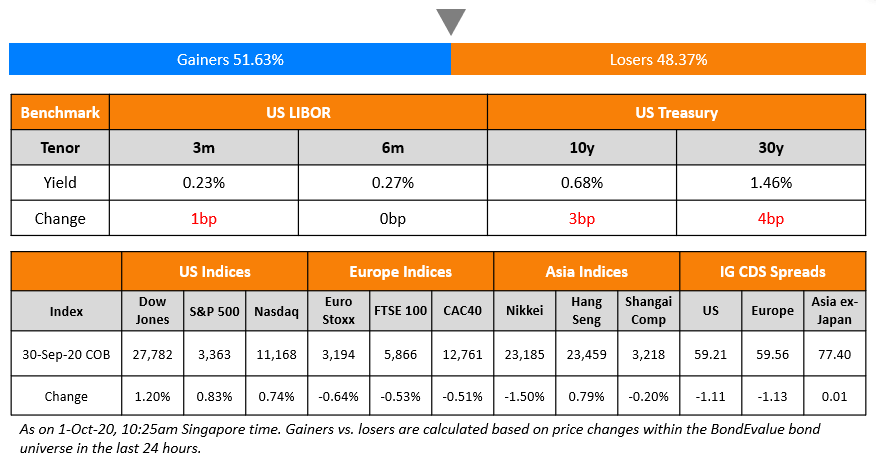

S&P ended the day higher by 0.8% after it went as much as 1.5% higher midday. The rally was led by tech and healthcare. Amazon reversed most of its rally to end flat. Asian equities are modestly higher today. 10Y US Treasuries sold off 6bp intraday to end with yields up ~4bp aided by ADP Jobs data. ADP Nonfarm Employment printed 749,000 well past expectations of 649,000 signalling some labour market recovery – creating higher anticipation for the Nonfarm Payrolls (NFP) report tomorrow. Earlier yesterday, the first presidential debate saw more accusation than content with Trump seeming to overpower Biden, although CNN polls suggested six in ten saying Biden was better. Meanwhile US Treasury Secy. Mnuchin said an agreement between $1.5tn and $2.2tn for a new stimulus bill was possible but would not make significant progress in discussions last night with House Speaker Pelosi. US IG CDS tightened 1.5bp, HY was flat, LatAm CDS spreads widened 5.5bp and Asia Ex-Japan CDS tightened marginally.

Only 2 seats remaining for our masterclass on Understanding Bond Calculations Using Excel with George Thomas today at 5pm Singapore time. Reserve your seat now!

New Bond Issues

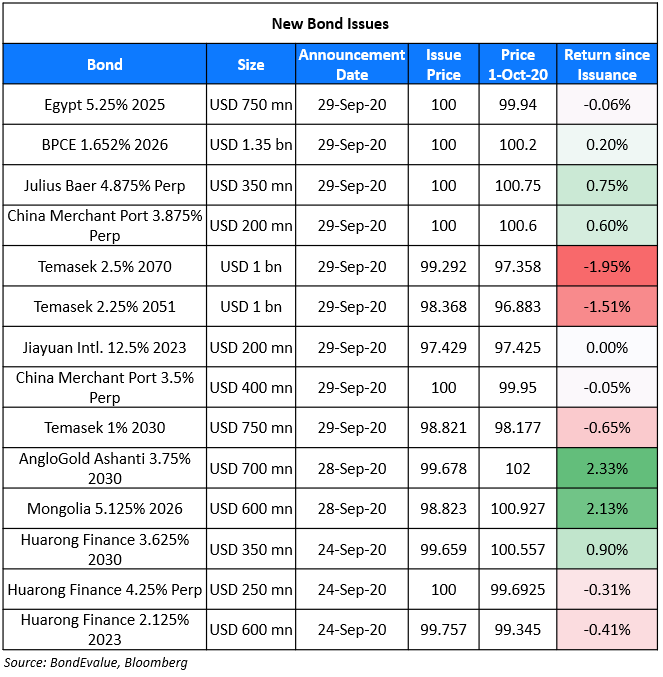

Singapore-based Keppel REIT raised S$150mn ($110mn) via a tap of its 3.15% subordinated Perpetual NC5 at par. The bonds carry a coupon reset if not called on September 11, 2025 and every five years thereafter to the prevailing SGD SOR plus a spread of 257.7bp.

New Bonds Pipeline

Star Energy $ Green amortizing bond

Pakistan $ Bond/Sukuk

Sumitomo Mitsui Trust Bank 7Y EUR covered bond

Mizuho EUR 5Y green and/or 10Y bond

Rating Changes

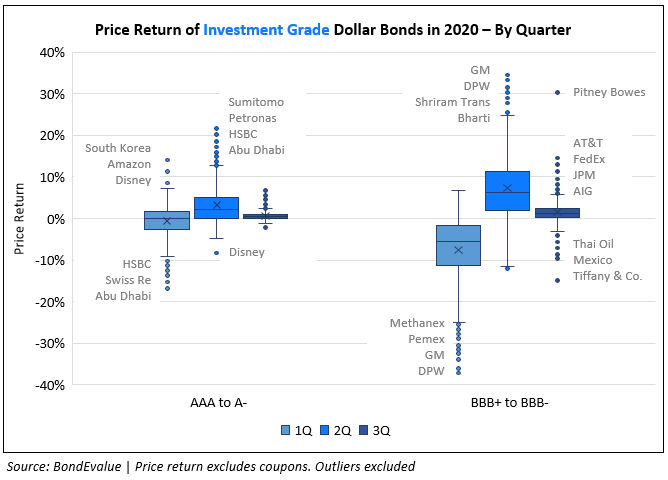

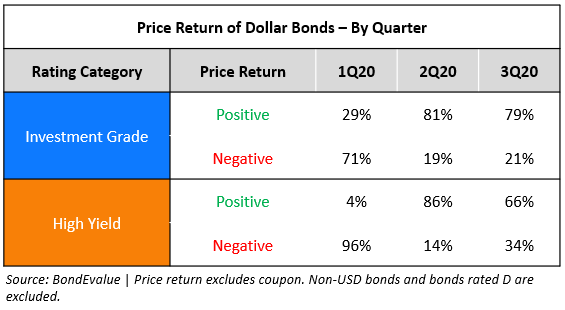

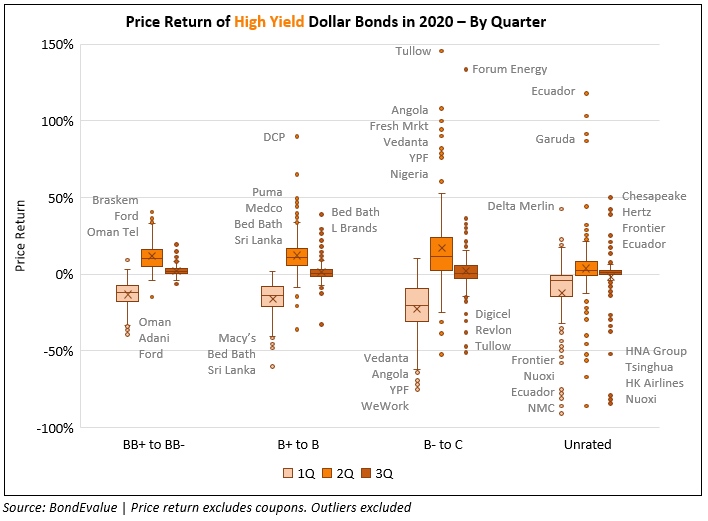

Q3 2020: 75% of Dollar Bonds Traded Higher; IG Led The Rally

The third quarter of 2020, ended September 30, finished on a cheerful note for bond investors as 75% of dollar bonds in our universe delivered a positive price return ex-coupon. The rally translated into unrealized gains of $55bn, calculated by multiplying the change in bond price in Q3 by the amount outstanding. For perspective, Q2 saw 81% of dollar bonds delivering a positive price return, which translated into an unrealized gain of $226bn.

Q3 was stronger for investment grade (IG) credits compared to high yield (HY) or junk credits. 79% of IG dollar bonds had a positive price return. In comparison, 66% of HY dollar bonds had a positive price return in Q3. In the table below, we have listed the quarterly price return for IG and HY dollar bonds.

We further broke down the quarterly price return by rating to see how they moved through 2020. In the box and whisker plots below, we have plotted the price return ex-coupon on the Y axis and the rating category on the X axis. The horizontal line inside each of the boxes indicates the median price return, while the box area above and below it represents the upper and lower quartile respectively. The dots that fall above and below the bounds are outliers with each dot representing a bond, some of which are labeled by the issuer name.

In the box and whisker plot for IG dollar bonds, we can see that while 79% of bonds moved up in price, the quantum of price increase was significantly lower compared to the rally in Q2. AT&T, FedEx, JP Morgan and AIG led the rally in the BBB category, while Tiffany & Co., Mexico and Thai Oil saw their bonds sell-off in Q3.

HY dollar bonds, true to their nature, witnessed a much higher variance in their price returns vs. IG. Within HY, bonds rated between B- and C and Unrated had more outliers vs. bonds rated BB and between B+ and B. Bed Bath and L Brands led the rally in the B+ to B category while Hertz, Frontier and Ecuador led the rally in the Unrated category.

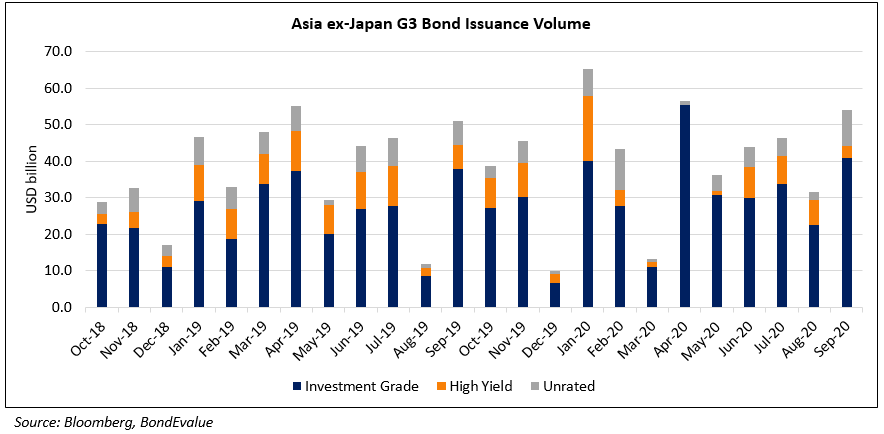

Q3 2020: New Bond Issuance

Global corporate dollar bond issuance in September stood at $165bn, bringing the Q3 volume to $398bn. This was lower compared to the $560bn in Q2 and slightly higher than the $392bn in Q1. The month of September marked a milestone for US HY issuance, which reached a record annual high of 329.8bn with three months remaining in the year.

G3 issuance volume for Asia ex-Japan stood at $54bn for September, up 71% over issuance in August. Q3 issuance stood at $132bn vs. $137bn in Q2 and $122bn in Q1. September saw an increase in IG and Unrated deals while HY issuance saw a decrease compared to the earlier few months.

September 2020: Largest Deals

Delta Air Lines issued a jumbo deal of $9bn in three tranches, the largest ever by an airline with the deal backed by its frequent flyer program. Delta’s $3.5bn tranche was the highest single issuance last month.

ICBC issued the largest Asian deal in September totalling $2.9bn of 3.58% Perpetual preference shares, though it was toned down from the envisaged $4bn.

.png?upscale=true&width=1500&upscale=true&name=Largest%20Deals%20Sep-Asia%20(1).png)

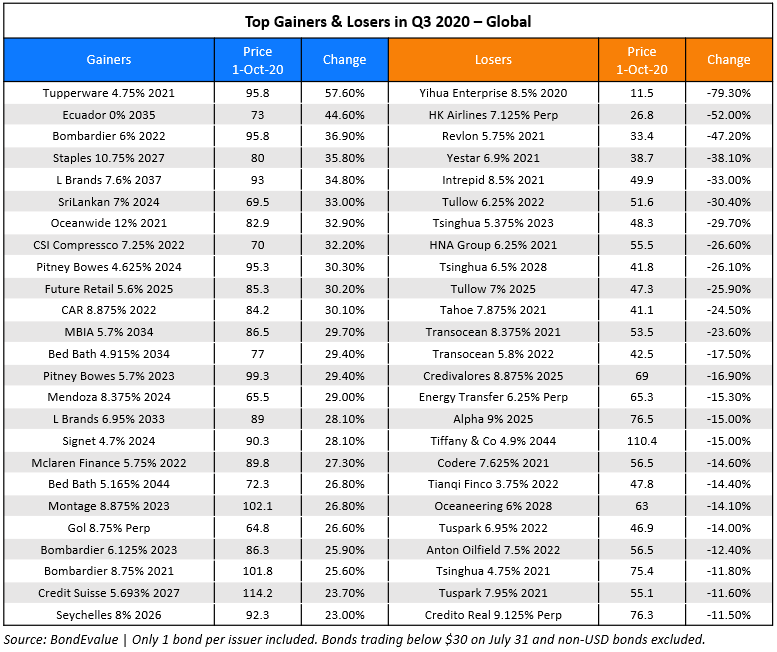

Q3 2020: Top Gainers & Losers

Tupperware, Ecuador, Bombardier and L Brands topped the gainers list with its dollar bonds yielding a price return of 58%, 45%, 37% and 35% respectively. The losers were led by Yihua Enterprises, HK Airlines and Revlon.

In Asia and Middle East, SriLankan Airlines, Oceanwide and Future Retail led the gainers list yielding a price return of ~30%. Future Retail recovered after the Indian retailer paid its first coupon on its first dollar bond on the last day of the grace period and then announced Reliance’s acquisition of the company. This led to a rally in its dollar bonds.

Fed Extends Limits on Bank Dividends and Buybacks; European Banks Criticize ECB on their Limits

The US Federal Reserve announced extension of limits it had set in June for the biggest US banks till the end of the year. Large banks with assets greater than $100bn are prohibited from making share repurchases while dividends have been capped and tied to a formula related to recent income – an assessment based on June’s stress tests. The stress tests showed loan losses for the 34 large banks ranged from $560bn to $700bn in the sensitivity analysis and aggregate capital ratios declined from 12% in 4Q2019 to between 9.5% and 7.7% under hypothetical downside scenarios. The Fed mentioned that capital positions remained strong in the last quarter with these restrictions but wants to continue the policy to provide further cushion against loan losses and to help lending.

In Europe, Societe Generale and Banco Santander criticized the European Central Bank’s (ECB) dividend ban policy enforced in March which required banks not to pay FY2019 and FY2020 dividends at least until October 1 2020. ECB also mentioned that banks should refrain from buybacks. Two weeks back, sources said that ECB was planning to lift the ban and now we are close to an update by the ECB on the same. Banco Santander last week became the first EU major bank to propose dividends on this year’s earnings for 2021 as per Bloomberg but acknowledged it would depend on ECB lifting the ban. Even tying dividends to capital levels would mean “the incentive for banks is to have more capital and lend less, to support the economy less,” a former ECB executive board member said.

Moody’s Notes Asian HY Covenant Quality at All-Time Lows

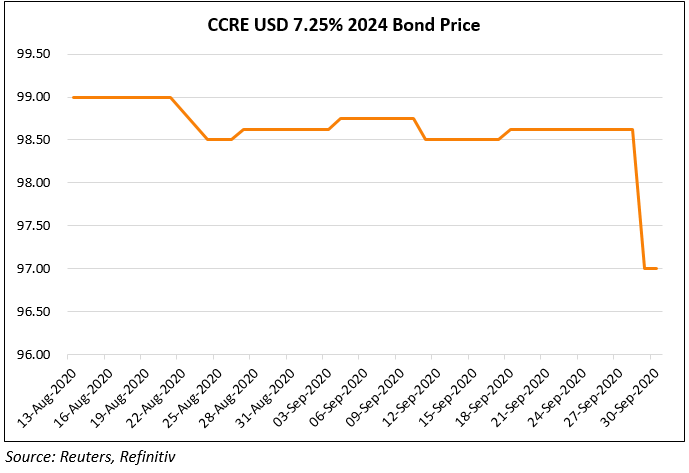

Moody’s in a report today said that the average Covenant Quality (CQ) for Asian HY bonds reached an all-time weakest score of 3.48 in 3Q2020 from the earlier 3.11 in 2Q2020. The CQ is scored on a scale of 1-5 where 1 denotes strong CQ and a higher score towards 5 denotes weak CQ. The assessment was done on 23 HY bonds totalling $8.1bn in issuance with an average coupon of 7.6%. The drop in CQ was led by Chinese property bonds from repeat issuers. “The average CQ score for full-package Chinese property bonds from January 2011 through September 2020 is 3.13 (moderate), 25% weaker than the 2.50 (good) score for full-package Asian bonds excluding Chinese property bonds”, they noted. Moody’s highlighted that prior to Central China Real Estate (CCRE) USD 7.25% 2024 senior note, no full-package Asian bond had ever scored in the weakest category going by their prospectus and assessment of:

-

-

- Lien subordination – CCRE’s prospectus notes “Permitted Liens also gives us and our Restricted Subsidiaries flexibility to incur debt secured by certain assets, the security interest of which may not be shared with holders of the Notes. The Notes will therefore rank behind such secured debt to the extent of the value of such security, the amount of which may be material”

- Restricted payments income basket predated to 2010 with no disclosure of accumulated credit. The prospectus mentions “For the avoidance of doubt, the 2010 Dividend shall not be included in such calculation”

- Leveraging – credit facility under joint debt basket capped to 35% of total assets, which can be secured under the permitted liens carve-out. This could be done without rating and securing the bonds.

-

In related news, Chinese developer Evergrande’s dollar bonds continued to rally with the 13.75% 2023s moving the most, up ~9.5%.

Bondholders To Block Zambia’s Plans to Delay Interest Payments

Bondholders of Zambia’s sovereign debt including hedge funds Pharo and Amia Capital have raised concerns over the amount of Chinese debt held by the government. The concerns have been voiced after Zambia had asked for a meeting on Oct 20 with holders of three eurodollar bonds worth $3bn to get consent to defer coupon payments till April next year. The bondholders who own 40% of the sovereign bond debt are likely to resist the deal by the Zambian government as they are troubled by the lack of transparency on the ‘true scale of the Chinese debt’. The bondholders’ skepticism increased after Bwalya Ng’andu, Zambia’s finance minister, did not provide an opportunity for clarifications to the bondholders after his address on Tuesday. “We know it’s the Chinese debt that’s pushed Zambia over the edge,” said Kevin Daly, a portfolio manager at Aberdeen Standard Investments, which holds some Zambian bonds. “Bondholders want more transparency but also to know what they intend to do about Chinese loans. That’s essential to debt sustainability.” The investors remain wary of the perceived inconsistencies on borrowing plans between the presentation and the recent budget and one investor said that “Bondholders are not going to accept a restructuring on terms worse than other lenders,” adding that “The big question was whether Zambia was ‘serious’ about getting a loan from the IMF and agreeing a plan to tackle its debt.”

Fitch had lowered Zambia’s credit rating to C earlier this week. As per the rating agency the rating action is “reflecting Fitch’s view that a sovereign default will follow the ‘consent solicitation’ issued by the Zambian government on suspending debt service payments on its three outstanding global bonds”. According to the rating agency Zambia downgrade highlighted the risk of African sovereign defaults specially for Angola, Republic of Congo, Gabon and Mozambique as the most vulnerable countries. Zambia’s dollar bonds were down ~3%. Its 8.97% and 8.5% bonds maturing in 2027 and 2024 traded at 48.9 and 49.3 cents on the dollar respectively.

For the full story, click here

American Air Downgraded to B- from B by Fitch Ratings; American and United To Lay off Thousands of Employees

Fitch has downgraded American Airlines to B- from B. The downgrade for the heavily indebted carrier comes due to slower than expected recovery in the air travel sector. The airline also remains on negative watch due to the uncertainty surrounding the aviation sector. The top line revenues of the company is extremely stressed due to the low demand for travel and the company reported a daily cash burn of $30mn at the end of June earlier this year. This cash burn could increase in the future as per the rating agency. That said, the airline has adequate liquidity to meet its obligations in the near term. It has a liquidity of ~$13bn bolstered by a $5.5bn loan from Coronavirus Aid, Relief, and Economic Security (CARES) Act. The liquidity could further strengthen in case the aid under CARES is enhanced to $7.5bn and/or the airline could also be included in the list of companies which would get an extension of the Payroll Support Program. The next major maturity of $750mn for American’s unsecured bonds is in June 2022. However, the principal amortization, interest costs and pension obligations over the next year will continue to weigh heavily and will continue to be a drain on cash.

For the full story, click here

Meanwhile Bloomberg reported that American and United are looking at laying off 19,000 and 13,000 employees respectively unless the payroll support is extended for the US carriers. The US Treasury Secretary Steven Mnuchin has urged the airlines to delay layoffs and is negotiating a $25bn in payroll aid for the airlines with the Congress. Delta Air Lines is not likely to go the layoff route since 17,000 of its employees left voluntarily and another 40,000 took unpaid leave. The American Airlines CEO, Doug Parker in a letter to its employees wrote that “I am extremely sorry we have reached this outcome,” and added that “It is not what you all deserve.”

For the full story, click here

Within all gloom there was some hope for the US airlines. United revealed through an SEC filing on Sep 28 that it entered into a Loan and Guarantee Agreement for a term loan facility of up to $5.17bn with the US treasury. These are likely to be disbursed in up to three disbursements on or before March 26, 2021. The filing also revealed that the Treasury could allocate additional loan commitments under the CARES Act in October 2020 and the amount available under the Term Loan Facility could be increased to up to $7.5bn.

For the full story, click here

Oasis Petroleum File for Chapter 11 Bankruptcy; Downgraded to D-PD from B3-PD

Oasis Petroleum joined the bandwagon of the companies which have filed for bankruptcy protection under Chapter 11 of the Bankruptcy Code which provides for reorganization. The petroleum sector has been hit hard due to the low oil prices after Russia and Saudi Arabia had engaged in the price war at the beginning of this year. The fall in demand due to the Coronavirus induced slowdown only exacerbated the situation and the oil prices went in the negative territory for the first time after there was an oversupply of petroleum due to the low demand. The company had failed to pay its interest on bonds maturing in 2022 and 2023 and thus was likely to go for restructuring. Oasis aims to reduce its debt by $1.8bn and receive $450mn in debtor-in-possession financing through a debt restructuring process. As per Houston law firm Haynes and Boone, 36 oil and gas producers have filed for bankruptcy in the last eight months and this number is only likely to increase. The Chief Executive of Oasis, Thomas Nusz said that “Due to historically low global energy demand and commodity prices, we determined that it is best for Oasis Petroleum to take decisive action to strengthen our liquidity and overcome the headwinds now challenging both our company and industry,”.

After the company filed for bankruptcy, Moody’s downgraded Oasis Petroleum’s Probability of Default to D-PD from B3-PD, Corporate Family Rating (CFR) to Caa3 from B3 and senior unsecured notes rating to Ca from Caa1. A D-PD probability of default rating is assigned after a failure to pay interest or principal extends beyond any grace period specified by the terms of the debt obligation.

The company’s bonds have been trading at stressed levels. However, after the news the bonds surged by 30%. The 6.5% bonds maturing in 2021 traded at 22.9 cents on the dollar, up 6.44 points and the 6.875% bonds maturing in 2022 traded at 23.75 cents on the dollar, up 7.25points.

For the full story, click here

Adidas Places its First Sustainability Bond

Adidas placed a €500mn 0% 2028 bond to be listed on the Luxembourg Stock Exchange adding that the offer was more than five times oversubscribed. “Following the first-time bond placements as an investment-grade-rated issuer earlier this month, today’s successful sustainability bond offering marks another milestone for our company,” said Adidas CFO Harm Ohlmeyer. The proceeds will go to fund environmental and social initiatives at Adidas in accordance with the sustainability bond framework validated by a second-party opinion from Sustainalytics. S&P rated Adidas A+ while Moody’s gave them an A2 rating, both with a ‘Stable’ outlook. Adidas placed two bonds amounting to €1bn in total – a €500mn 0% 2024 and €500mn 0.625% 2035.

Term of the Day

PMI

PMIs or Purchasing Managers’ Index are an index composed of a monthly survey of purchasing managers/supply chain managers across industries. This is a diffusion index, a statistical measure of summarizing the common tendency of a series – if there are more number of values rising than falling, the index is above 50 and the index goes below 50 if the falling values exceed those rising. For PMIs, a value below 50 indicates contraction and a value above 50 shows expansion. These surveys are taken over different areas of the supply chain business: New Orders, Employment, Inventories, Supplier Deliveries and Production covering imports, exports, prices and backlogs. In most countries, Markit publishes the PMI numbers while other organizations publish them too. Markit generally publishes the month’s PMIs in last week of the month.

Talking Heads

“There may be enough resources right now, at least for 2020,” Bullard said. “It probably not so much hinges on whether Congress acts or not before the election here or after the election,” he said. “You could probably wait until next year and then you could assess the situation at that point and make a decision.”

“I have been more bullish on the economy and think it is recovering faster than what was expected,” Bullard said, adding that growth trackers for the third quarter show the economy expanding at an annualized pace above 30%.

“The markets and the public have pretty good clarity,” Kaplan said. “The markets expect that the fed funds rate is going to stay at zero probably until 2023.” “Beyond that point, I believe that the committee should retain greater policy rate flexibility to decide on the appropriate stance of monetary policy,” he said.

“Large-scale purchases of government bonds can be a legitimate and effective tool of monetary policy,” he said. “But, as I have stressed numerous times, they risk blurring the lines between monetary policy and fiscal policy.”

“We should also pay close attention to how we interpret our mandate,” he said. “The more widely we interpret our mandate, the greater the risk that we will become entangled with politics and overburden ourselves with too many tasks.”

He warned “now is not the time for the economics of Chicken Licken,” referring to a folk tale known as Chicken Little in other parts of the world, in which a bird believes the sky is falling because an acorn fell on its head.

“If the economy were sat on a psychiatrist’s sofa, the diagnosis would not be especially difficult,” Haldane said. “These are the psychological symptoms of anxiety. And collective anxiety is as contagious, and could be as damaging to our well-being, as this terrible disease.”

“I wouldn’t sell Italian bonds on a risk-off event, simply because the ECB is there,” said Christiansen. “That commitment with its yield curve cap and flexibility embedded in the PEPP shouldn’t be underestimated.”

On Mexican authorities warning of additional Pemex downgrade as pandemic rages on

Alonso Hidalgo, Latin America officer at the Natural Resource Governance Institute’s (NRGI)

“Well into the second year of the administration, the government’s struggle to turn Pemex around has been well documented. Now, with the pandemic in full swing – and no relief in sight for oil producers – there are reasons to question this strategy.” Longer term, Hidalgo said, “the propping up of Pemex as the economic backbone of the country could entail huge risks for Mexico’s overall financial stability,” especially if an accelerated global energy transition leads to lower long-term oil prices.

In a statement by Consejo de Estabilidad del Sistema Financiero (CESF), Mexico’s financial system stability council

As for the economy, “global and national financial conditions are subject principally to the pandemic,” CESF said. “It could be necessary to implement new confinement measures, with the risk of limiting the economic recovery.” “In this context, Mexico showed a reduction in risk premiums and interest rates for government bonds showed moderate movement throughout the yield curve.”

“The shift to green, on a broad level, is too slow, way too slow,” she said. “The green bond market is far too little.” She warns that “the interest from investors will diminish over time” if green issuers don’t step up.

“If green bonds account for about 5%-7% of the European bond universe, it doesn’t give us much if you make those bonds ultra green,” she said. “We’d get much more bang for the buck if we make the 95% which aren’t yet green a little greener.”

Lindahl says “the investor base is going mainstream with sustainability,” and that means all corporate issuers “need to have a good and credible ESG story — full stop!”

Top Gainers & Losers – 1-Oct-20*

Other Stories

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.