This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

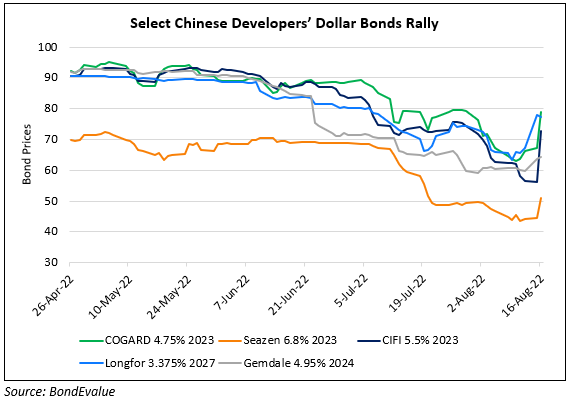

Yuexiu Downgraded to Ba2; Seazen Upgraded to B3

March 9, 2026

Yuexiu Property was downgraded by a notch to Ba2 from Ba1 by Moody’s. The downgrade reflects slower-than-expected deleveraging and prolonged weak profitability amid the continued downturn in China’s property sector. According to Moody’s, margin pressure will stem from efforts to clear inventory from projects with higher historical land costs and pricing pressures, which will likely constrain earnings. Yuexiu’s dollar bonds traded stable. For instance, its 3.8% 2031s were at 89.9, yielding 6.2%.

On the other hand, another Chinese property developer, Seazen Group was upgraded by a notch to B3 from Caa1 by the rating agency. The upgrade reflects reduced refinancing risk after Seazen regained access to offshore bond markets. Since June 2025, the company has issued about $865mn of dollar bonds with 2–3 year tenors, allowing it to refinance near-term maturities and improve its debt profile. Moody’s also noted the growing recurring rental income from Seazen’s large investment property portfolio, which provides stable cash flow and helps offset weakness in its property development business. Seazen’s newly issued 11.8% 2029s were trading stable at 96.4, yielding 13.3%.

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.