We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

US Treasury Yields Ease Sharply on Ceasefire Agreement

April 8, 2026

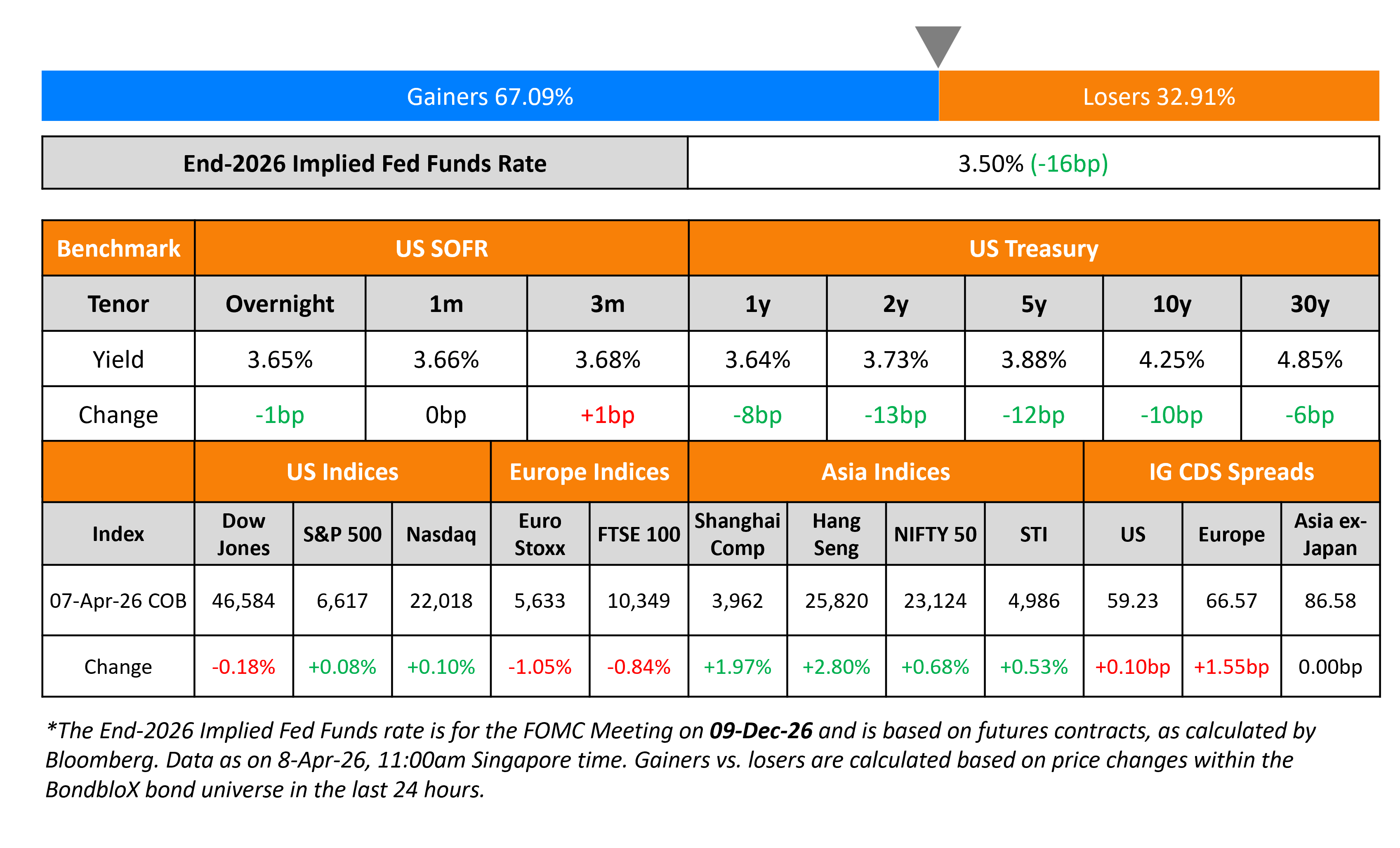

US Treasury yields dropped sharply across the curve after US President Donald Trump and Iran agreed to a two-week ceasefire. Brent crude sold-off by over 15% on the back of the positive update, down to $94/bbl. On the data front, the preliminary Durable Goods Orders for February fell by 1.4%, softer than expectations of -1.2%. Core Durable Goods Orders came in at 0.8%, better than the surveyed 0.5%. Separately, the US Treasury’s 3Y auction received solid demand with a bid-to-cover of 2.68x and an indirect take-up of 74.8%.

Looking at US equity markets, the S&P and Nasdaq closed higher by 0.1% before the ceasefire agreement was made. US IG CDS spreads widened by 0.1bp while HY CDS spreads were 0.3bp tighter. European equity indices ended lower. The iTraxx Main CDS spreads widened by 1.6bp and Crossover spreads were 9.8bp wider. Asian equity markets have opened sharply higher this morning. Asia ex-Japan CDS spreads were flat.

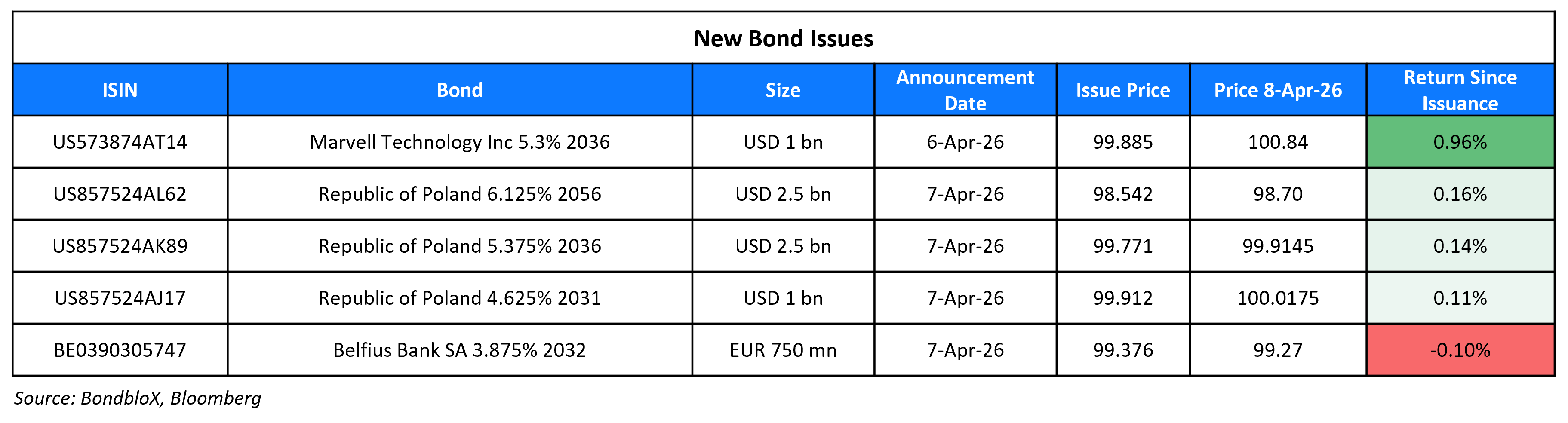

New Bond Issues

The Republic of Poland raised $6bn via a three-trancher. It raised:

- $1bn via a 5Y bond at a yield of 4.645%, 30bp inside initial guidance of T+95bp area.

- $2.5bn via a 10Y bond at a yield of 5.405%, 30bp inside initial guidance of T+135bp area.

- $2.5bn via a 30Y bond at a yield of 6.233%, 30bp inside initial guidance of T+160bp area.

The senior unsecured notes are rated A2/A-/A-. Proceeds will be used for general budgetary purposes.

New Bonds Pipeline

- Sasol $ 7NC3 bond

Rating Changes

- France-Based Seismic Services Company Viridien S.A. Upgraded To ‘B’ On Consistently Lower Leverage; Outlook Stable

- The Manitowoc Co. Inc. Upgraded To ‘B+’ On Resilient Operating Performance; Outlook Stable

- BCPE Empire Holdings Inc. Upgraded To ‘B’ From ‘B-‘ On Deleveraging Merger With BradyPLUS; Outlook Stable

- Cornerstone Building Brands Inc. Downgraded To ‘CCC+’ On Weak Credit Metrics; Outlook Negative

- Community Health Systems Inc. Outlook Revised To Positive From Negative On Operating Improvement; ‘CCC+’ Rating Affirmed

- Moody’s Ratings changes Matador’s outlook to positive, affirms Ba3 CFR

- Moody’s Ratings affirms Blue Owl Credit Income Corp.’s Baa2 senior unsecured ratings; changes outlook to negative from stable

Term of the Day: 144A Bond

144A bonds refer to privately placed debt instruments that can be traded among qualified institutional buyers (QIBs) and with a shorter holding period of six months. These bonds get their name from Rule 144A, which exempts the securities from SEC registration that typically requires extensive documentation and a two-year holding period. 144A bonds can be issued with a lesser amount of documentation as the underlying assumption is that QIBs are sophisticated investors who do not need the same level of information and protection as individual investors. The SEC defines a QIB as institutional investors that have at least $100mn in assets under management.

Talking Heads

On Bond Traders Risking Being Wrongfooted by 2022 Playbook – UBS

“The markets are pricing this like it was 2022 where you price up all central banks together — it’s a very different situation… in the front end, there is value being created, particularly in the UK, particularly in the US

On Iran war may boost inflation, but not expectations – Dallas Fed Research

An extended disruption of the world’s oil trade from the Iran war could lift headline U.S. inflation to well over 4% by year-end, with even bigger increases possible in the short term… effect on inflation expectations, however, looks likely to be modest in the short term and negligible in the longer term.

On US Equities’ Valuation Premium Bringing Stagflation Era Flashbacks

Dennis DeBusschere, 22V Research LLC

Current equity risk premium “is consistent with the 1970s stagflation”

Michael O’Rourke, JonesTrading Institutional Services

“In an environment that lacks visibility, investors will be inclined to take a more defensive position… will require “a higher risk premium before allocating capital”

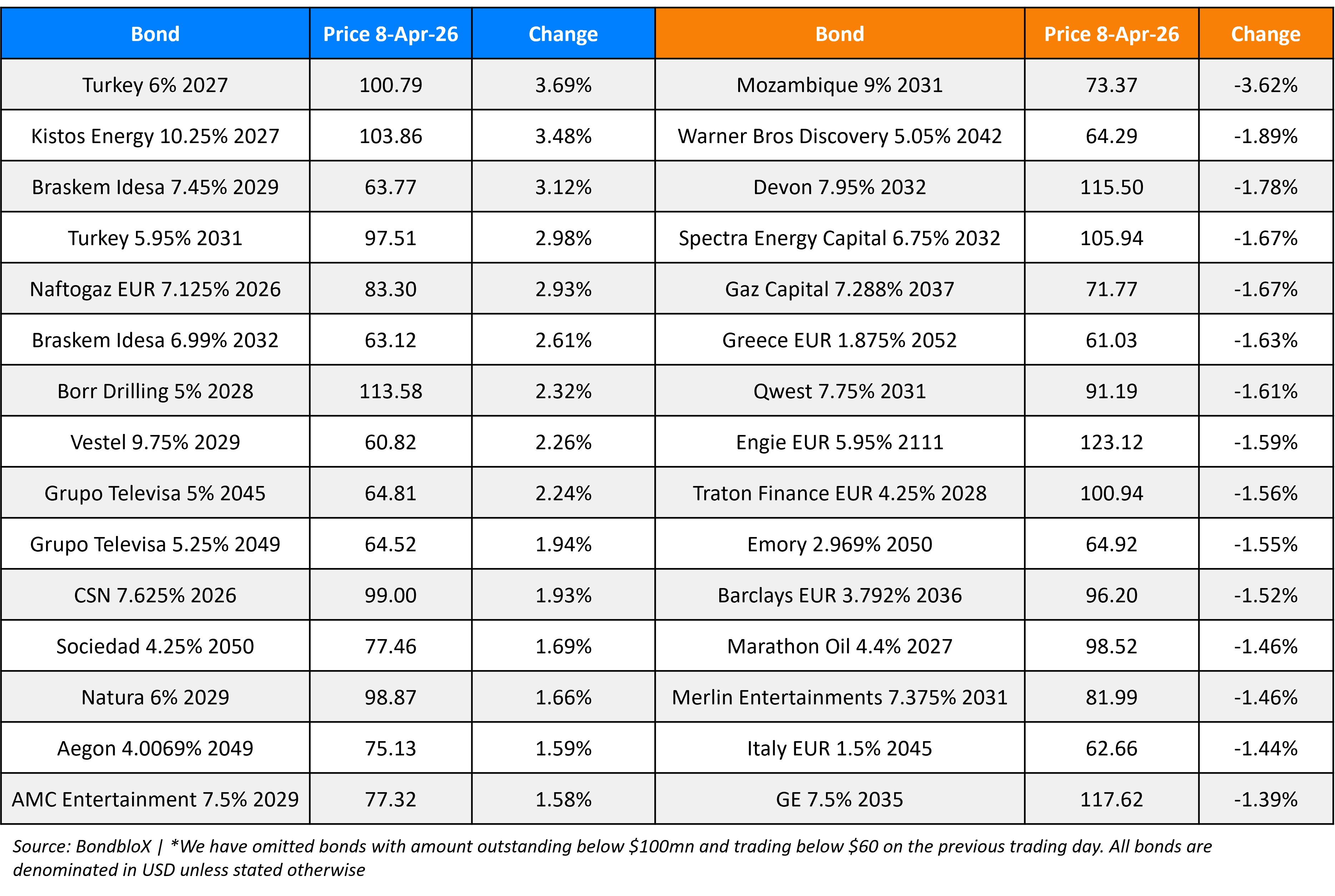

Top Gainers and Losers- 08-Apr-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.