This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

US Imposes Global Tariffs of 15%

February 23, 2026

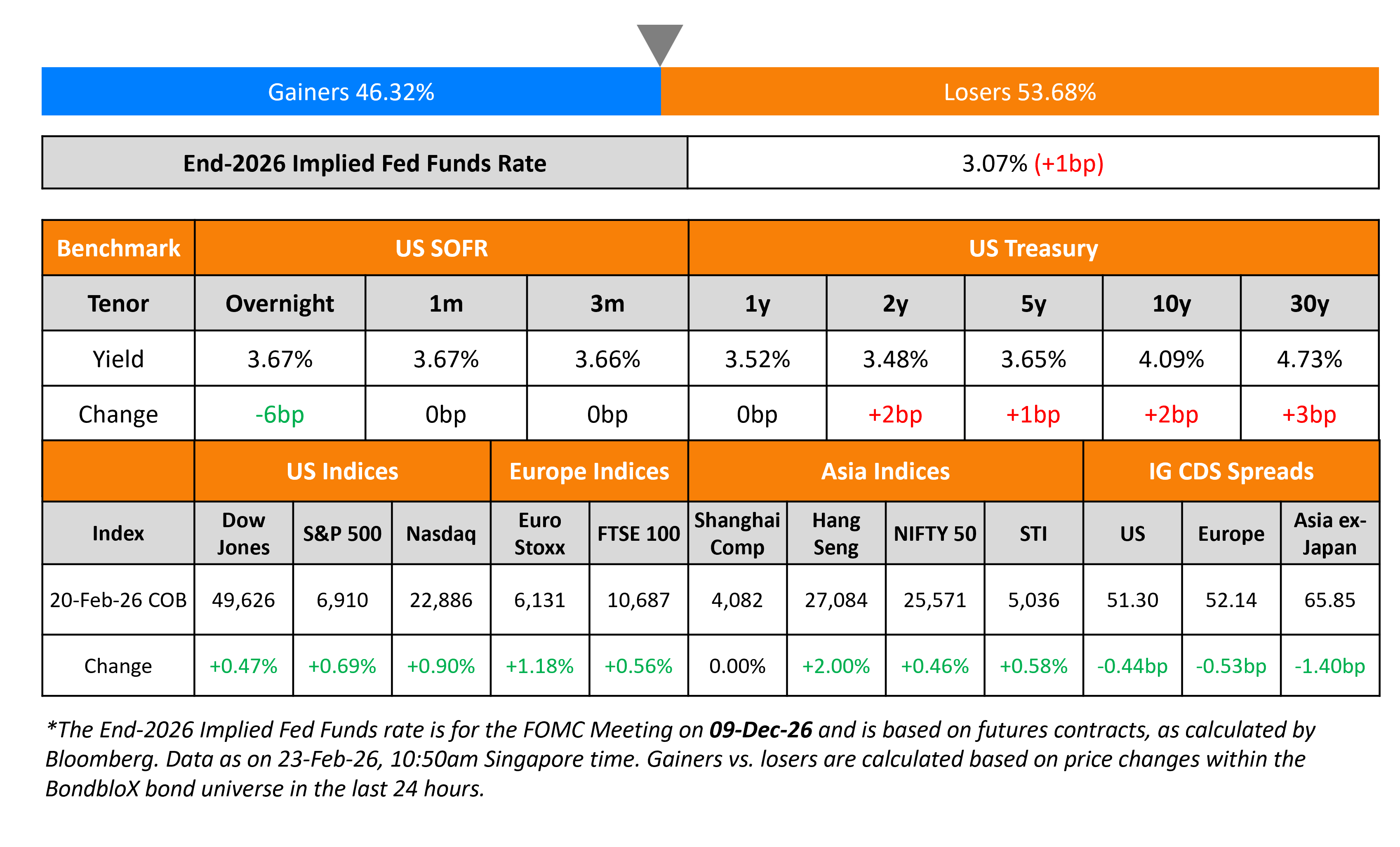

US Treasury yields had a mixed reaction on Friday — moving lower by ~4bp intially and then paring back the move, to end higher by ~2bp across the curve. The initial rally in Treasuries came on the back of the Supreme Court ruling where they voted 6-3 in favor of striking down most of the tariffs set by US President Donald Trump. This was seen as a positive against concerns of a rising US fiscal deficit and an increase in the supply of treasuries thereof. However, later on Friday, Trump announced a global tariff of 10% on all countries effective February 24, and further raised it to 15% over the weekend. Besides, he also noted that the current administration will work towards finding “new and legally permissible tariffs” over the next few months, renewing deficit-related concerns.

On the data front, the preliminary US Q4 GDP print came in at 1.4%, missing expectations of a 2.8% growth. The soft print came on the back of a slowdown in government and consumer spending. The Headline and Core PCE YoY readings for December came in at 2.9% and 3.0%, slightly higher than expectations of 2.8% and 2.9% respectively.

Looking at US equity markets, the S&P and Nasdaq ended higher by 0.7% and 0.9% each. US IG CDS spreads tightened by 0.4bp and HY CDS spreads were 1.5bp tighter. European equity indices ended higher too. The iTraxx Main CDS spreads were 0.5bp tighter and the Crossover CDS spreads were 2.4bp tighter. Asian equity markets have opened mixed this morning. Asia ex-Japan CDS spreads tightened by 1.4bp.

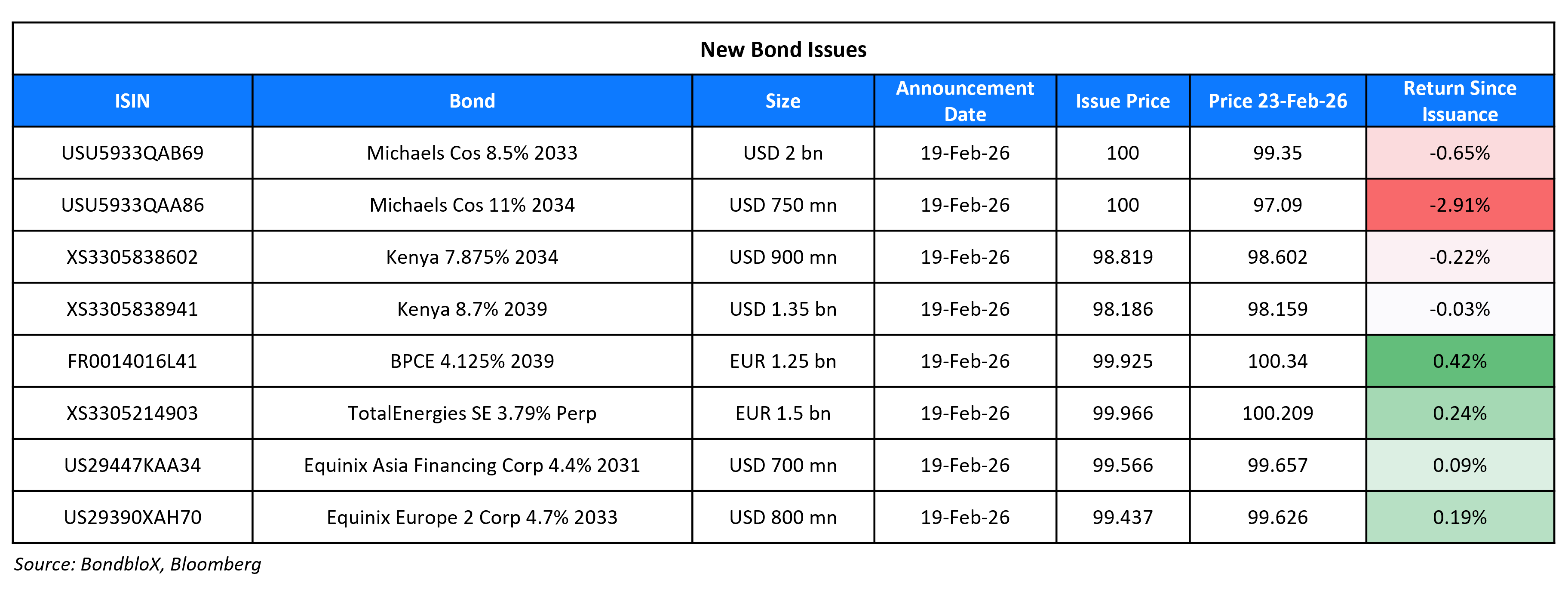

New Bond Issues

New Bonds Pipeline

- CBA A$ 10NC5 FRN/fixed and/or 20Y bullet subordinated notes

- Mirae Asset $ 3Y/5Y Dual-Listed Formosa Notes

- Advanced Info Service $ 5Y and/or 10Y

Rating Changes

- Moody’s Ratings upgrades Lumen’s CFR to B2 concluding ratings under review; outlook changes to stable

- Fitch Upgrades MHP to ‘CCC’ on Refinancing Completion; Removes Rating Watch Positive

- Fitch Downgrades CSN’s IDRs to ‘B’; Maintains Rating Watch Negative

- Fitch Downgrades Olin Corporation to ‘BB+’; Outlook Negative

- Moody’s Ratings downgrades Alpek’s rating to Ba1; outlook remains negative

Term of the Day: Personal Consumption Expenditures (PCE)

Personal Consumption Expenditures (PCE) is an inflation metric measuring consumer spending on goods and services, released by the US Department of Commerce. The Fed’s preferred measure of inflation is the Core PCE – this refers to the Headline PCE after stripping out two volatile components, namely, food and energy.

The US also publishes another inflation metric, the CPI (Consumer Price Inflation), a key inflation indicator. CPI and PCE differ on four fronts: formula, weight, scope and other factors. As per the BLS, “CPI sources data from consumers, while PCE sources from businesses. The scope effect is a result of the different types of expenditures CPI and PCE track…CPI only tracks out-of-pocket consumer medical expenditures, but PCE also tracks expenditures made for consumers, thus including employer contributions. The implications of these differences are considerable.”

Talking Heads

On Bond Market Momentum Shifts Bears’ Way as Sell Signals Flash

James Athey, Marlborough Investment

“We are underweight US Treasuries and happy to run those positions”

Jay Barry, JPMorgan

“We don’t expect a breakout, but within these ranges, we are bearish… data still looked good”

John Briggs, Natixis

“The initial reaction seemed too much to me, I don’t think many felt they would stay on”

On US Tariff Moves Risk Upsetting Equilibrium With EU – Christine Lagarde, ECB President

“You want to know the rules of the road before you get in the car… If it shakes the whole equilibrium which people in the trade had got used to .. to sort of shake it up again is going to bring about disruptions in the business for sure”

On Tariffs Have Damaged the US More Than Others – ECB Panetta

“Foreign exporters seem to have shouldered a portion of it, estimated at around 10%. Initially, the impact was absorbed by US firms’ profit margins, and was then partially passed on to consumers… no country can prosper for long by isolating itself”

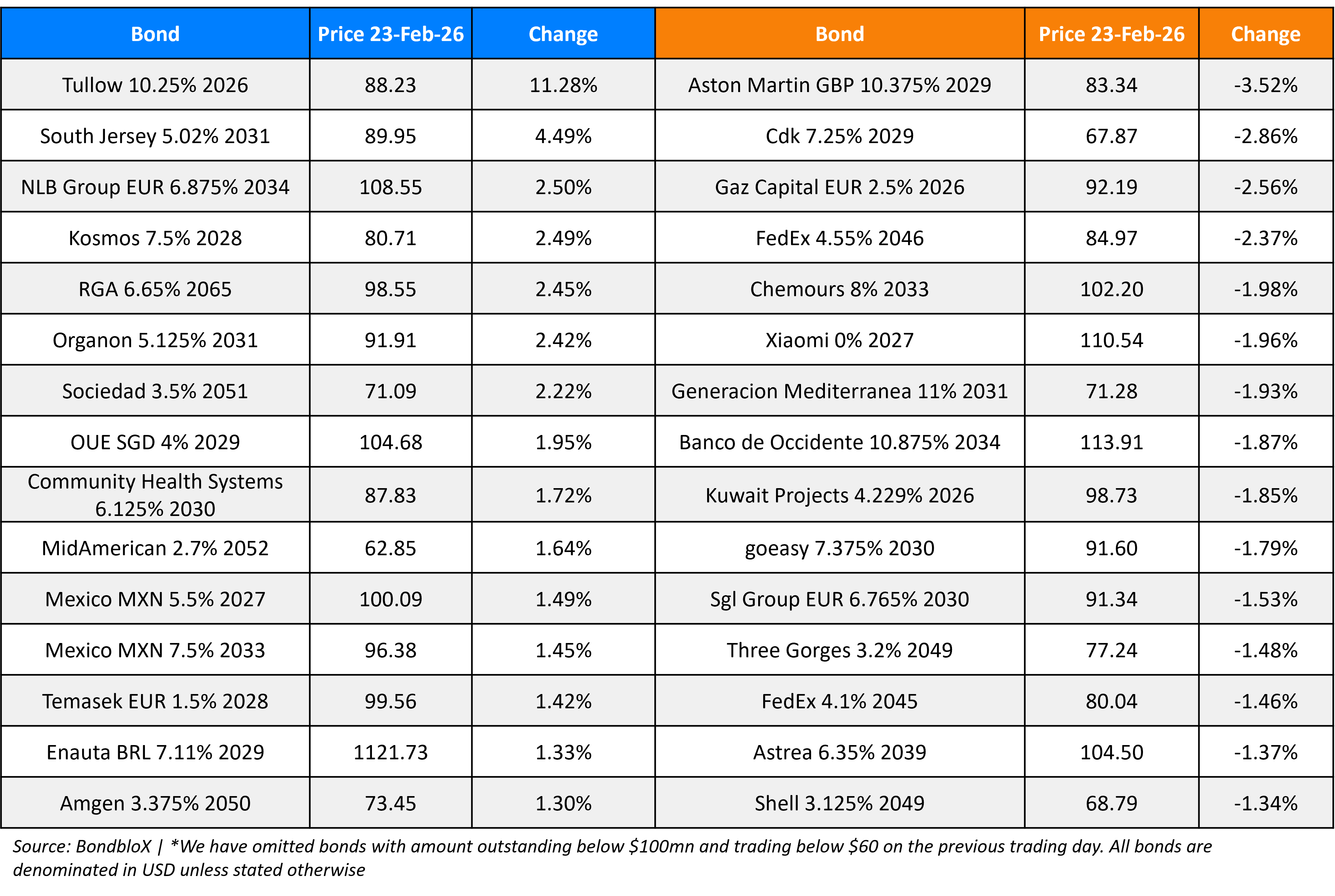

Top Gainers and Losers- 23-Feb-26*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.