This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Treasury Yields Stabilize amid Potential Geopolitical De-escalation

March 20, 2026

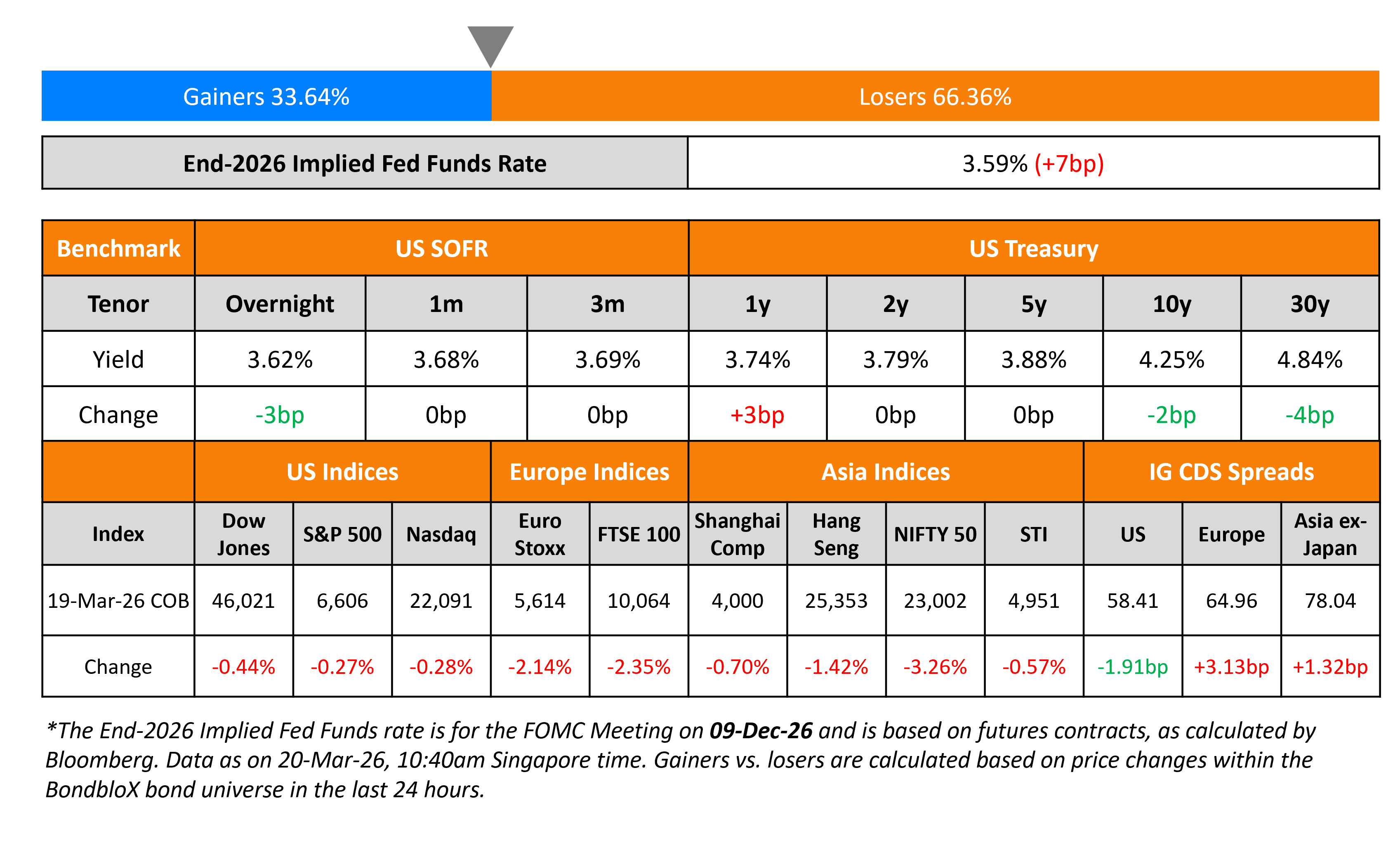

US Treasury yields are trading broadly stable despite intraday volatility yesterday. For instance, the 10Y yield jumped to nearly 4.33% in yesterday’s trading session, as Brent crude hit its highest level since July 2022 at $119.05/bbl. However, Brent crude eased since then and is currently trading at $107/bbl – this comes after US President Donald Trump said that they were not considering deploying ground troops in Iran. Also, Israeli Prime Minister Benjamin Netanyahu said that Israel would refrain from additional attacks on Iranian energy facilities and that the war could end sooner than expected. Separately, US Treasury Secretary Scott Bessent said that the US is exploring the possibility of removing sanctions on Iranian oil.

Markets are currently pricing in no Fed rate cuts this year. Looking at US equity markets, the S&P and Nasdaq ended lower by 0.3% each. US IG CDS spreads tightened by 1.9bp and HY CDS spreads were 10.5bp tighter. European equity indices ended sharply lower. The iTraxx Main CDS spreads were 3.1bp wider and the Crossover CDS spreads were 12bp wider. Asian equity markets opened mixed this morning. Asia ex-Japan CDS spreads widened by 1.3bp. The Bank of Japan (BOJ) kept its target rate unchanged again at 0.75%, in line with market expectations.

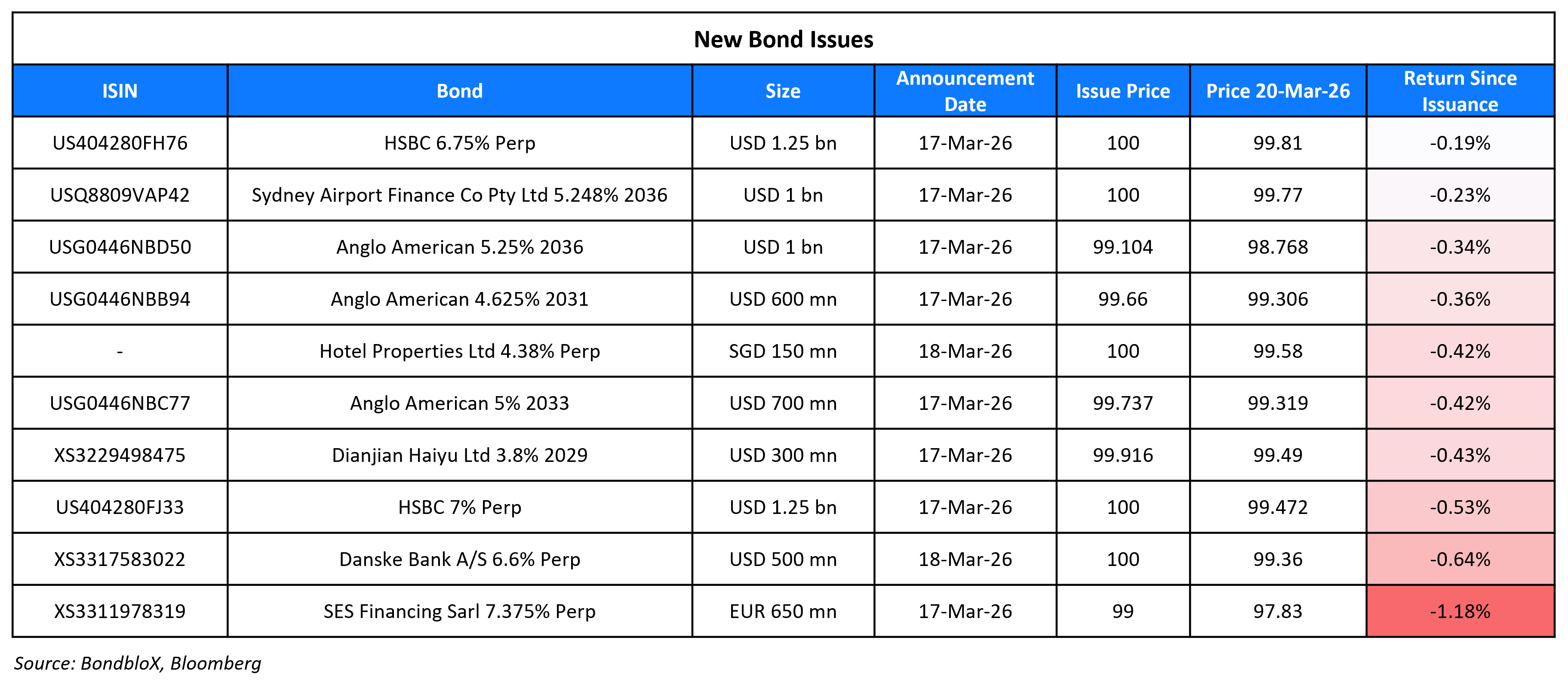

New Bond Issues

New Bonds Pipeline

- Kexim $ 3Y/5Y bond

- Korea National Oil Corp $ bond

Rating Changes

- Tutor Perini Corp. Upgraded To ‘BB-‘ From ‘B’ On Anticipated Strong Cash Generation; Outlook Stable

- Honda Motor Downgraded To ‘BBB+’ On Earnings Downturn; Outlook Stable

- Brandywine Realty Trust Downgraded To ‘BB-‘ From ‘BB’ On Debt Maturity Risk; Outlook Negative

- China Jinmao Outlook Revised To Negative On Increased Challenges In Deleveraging; ‘BBB-‘ Rating Affirmed

- Moody’s Ratings changes AstraZeneca’s outlook to positive from stable on continued pipeline progress; affirms A1 ratings

Term of the Day: American Depositary Receipts (ADRs)

American Depositary Receipts (ADRs) are USD-denominated certificates that trade on American stock exchanges and track the price of a foreign company’s domestic shares. They trade like regular US stocks and can represent a single share, multiple shares, or a fraction of a share of the foreign stock. They offer portfolio diversification and convenient trading during US market hours. However, unlike common stock, ADRs do not grant investors ownership rights.

Talking Heads

On Bond Markets Hit by Oil Shock as Traders Bet on Higher Rates

Brij Khurana, Wellington Management

“There was a consensus view that this was going to be over relatively quickly. The fear is now finally in the market that this could last a lot longer.”

Kevin Flanagan, WisdomTree

“This is just a wake-up call for the Treasury market to come around to that notion that we’re nearer to the end of the Fed’s rate cut cycle”

Thierry Wizman, Macquarie Group

“Central banks are beginning to address the prospect of higher inflation by adjusting their guidance and biases away from interest rate cuts, and toward hikes”

On Predicting Fed Next Month Will Flag Possible Rate Hike – BNP Paribas

“We believe the FOMC has already adopted in substance a symmetric policy outlook, with two conditions: that the war will leave a lasting imprint on energy prices, and that the US labor market will prove as resilient to this as it did to earlier negative policy shocks”

On Wall Street ending lower as traders see no rate cuts before 2027

Mike Dickson, Horizon Investments

“The market is digesting a little bit more of Powell and what some other central banks said overnight, that this is a real inflation risk”

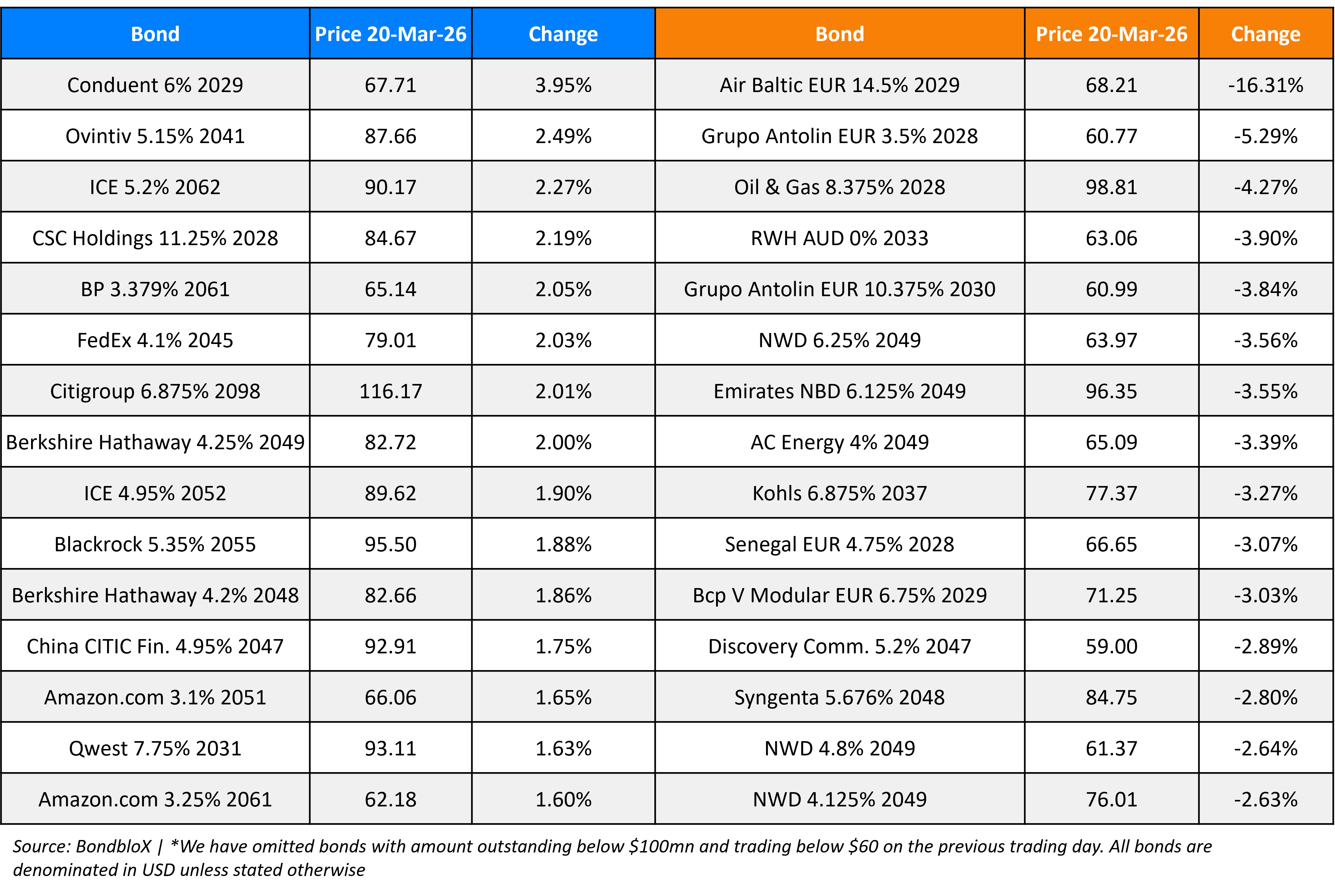

Top Gainers and Losers- 20-Mar-26*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.