This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

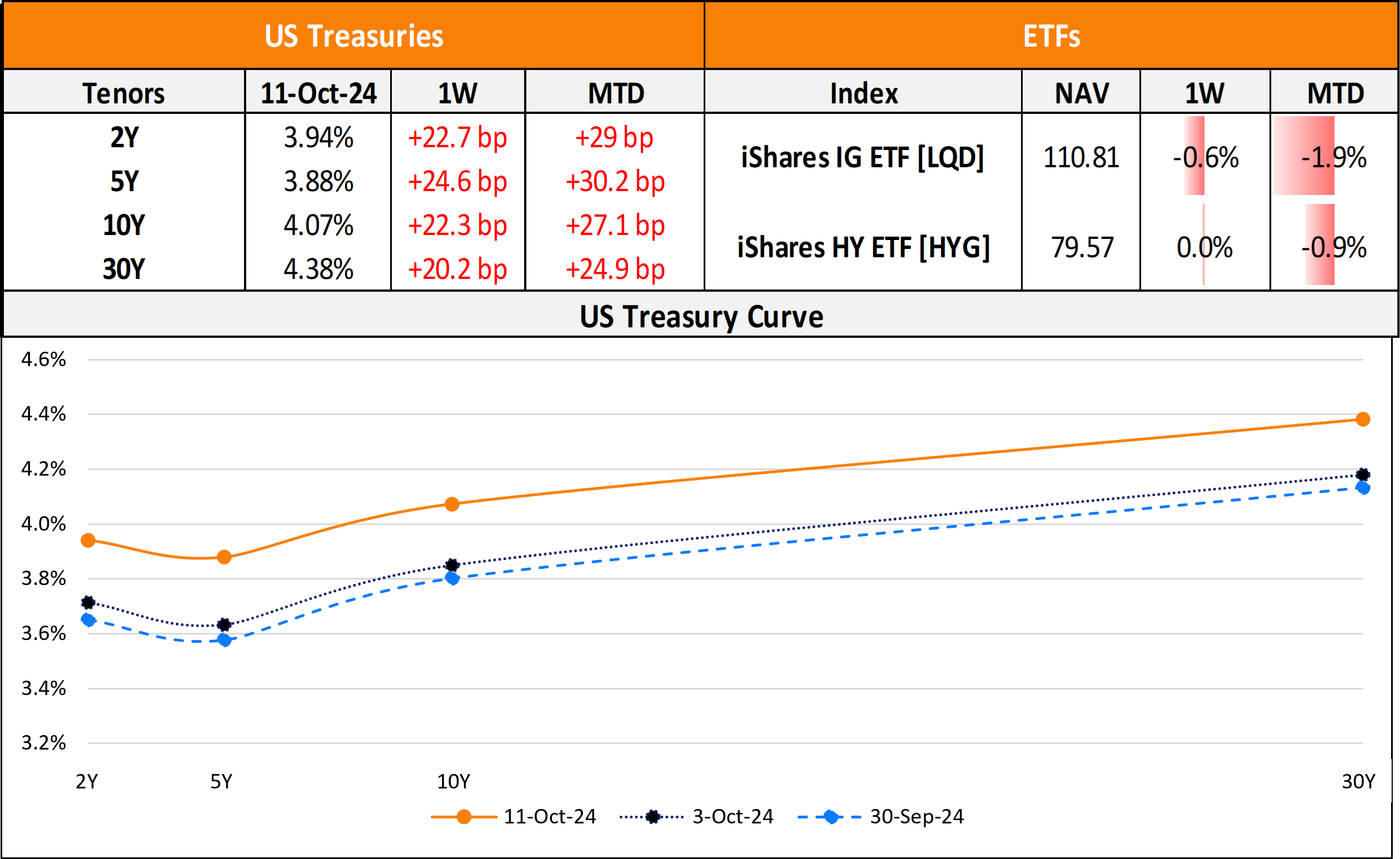

The Week That Was (7 – 13 October, 2024)

October 14, 2024

US primary market issuances fell last week to just $12.3bn vs. $20.3bn seen in the prior week. IG issuers took up $7.7bn of the total, led by Toyota Motor Credit’s $3bn three-trancher and Eastern Energy Gas’ $900mn deal. Last week saw $4.4bn in HY issuances from the region, led by Cleveland Cliff’s $1.8bn two-part deal and Glatfelter’s $800mn issuance. In North America, there were a total of 27 upgrades and 33 downgrades across the three major rating agencies last week. US IG funds saw $1.83bn of inflows last week, adding to the $3.8bn of inflows during the week before that. HY funds witnessed a net $145.6mn in outflows during the same period reversing the $2.2bn of inflows in the week prior to it.

EU Corporate G3 issuances dropped marginally last week to $24.5bn vs. $25.1bn in the prior week. KfW’s €3bn issuance led the tables, followed by StanChart’s $1.5bn deal and Banque Credit Mutuel’s €1.25bn issuance. The region saw 31 upgrades and 36 downgrades, across the three major rating agencies. The GCC dollar primary bond market saw a total issuance of $1.3bn vs. compared to $4.4bn seen in the prior week, thanks to two deals led by Sharjah’s $750mn sukuk and DIB’s $500mn sukuk perp. In the Middle East/Africa region, there were 6 upgrades and 25 downgrades across the major rating agencies. LatAm saw $3.2bn in issuances last week vs. $1.8bn in the week prior to it. Issuance volumes were led by Chile Electricity Lux’s $1.44bn deal, Braskem Netherlands’ $850mn and YPF Energia’s $420mn deals each. The South American region saw no upgrades nor downgrades across the rating agencies.

G3 issuance volumes from APAC ex-Japan rose to $3.9bn vs. $2bn seen in the previous week. KDB’s $1bn deal led the table, followed by HKMC’s $850mn issuance and ASB Bank’s €500mn deal. In the APAC region, there were 4 upgrades and 5 downgrades, across the three rating agencies last week.

Go back to Latest bond Market News

Related Posts:

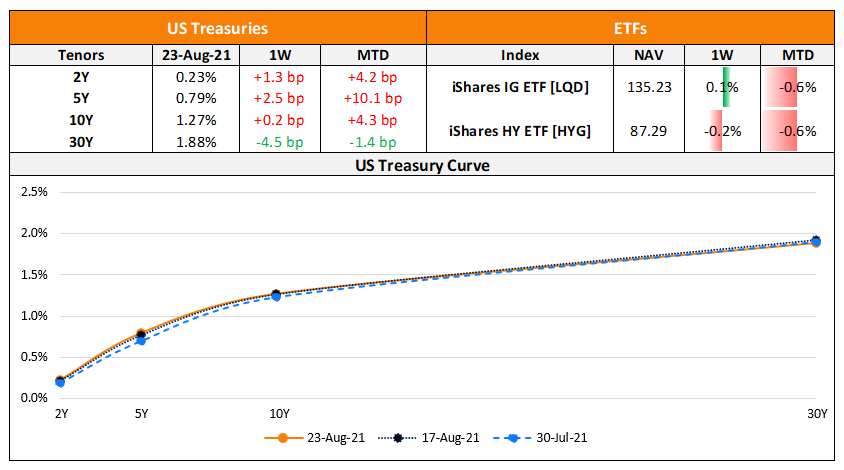

The Week That Was – (16th -22nd Aug)

August 23, 2021

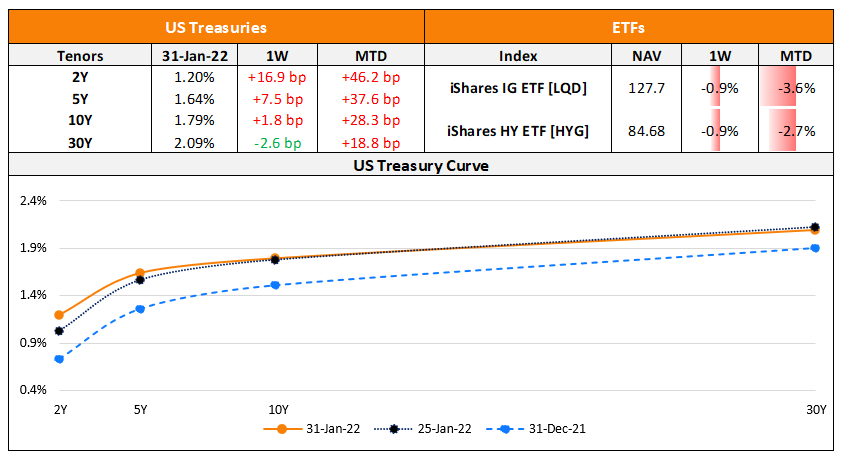

The Week That Was (24 – 30 Jan, 2022)

January 31, 2022

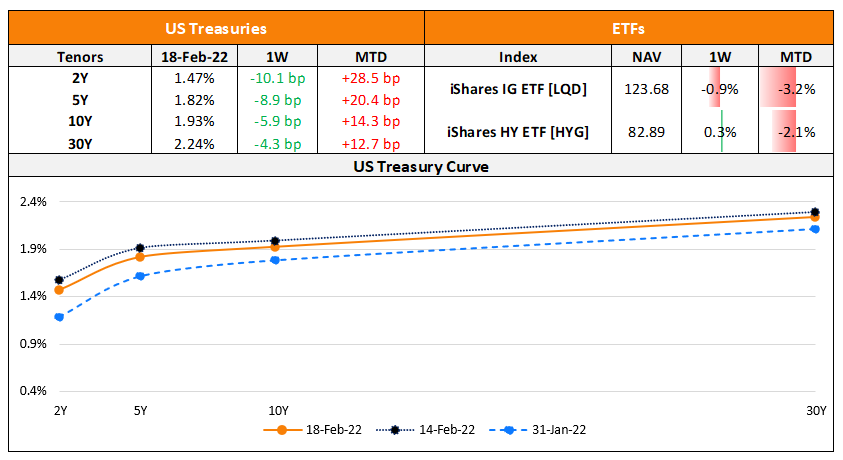

The Week That Was (14 – 20 Feb, 2022)

February 21, 2022

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.