This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

The Week That Was (16 – 22 March, 2026)

March 23, 2026

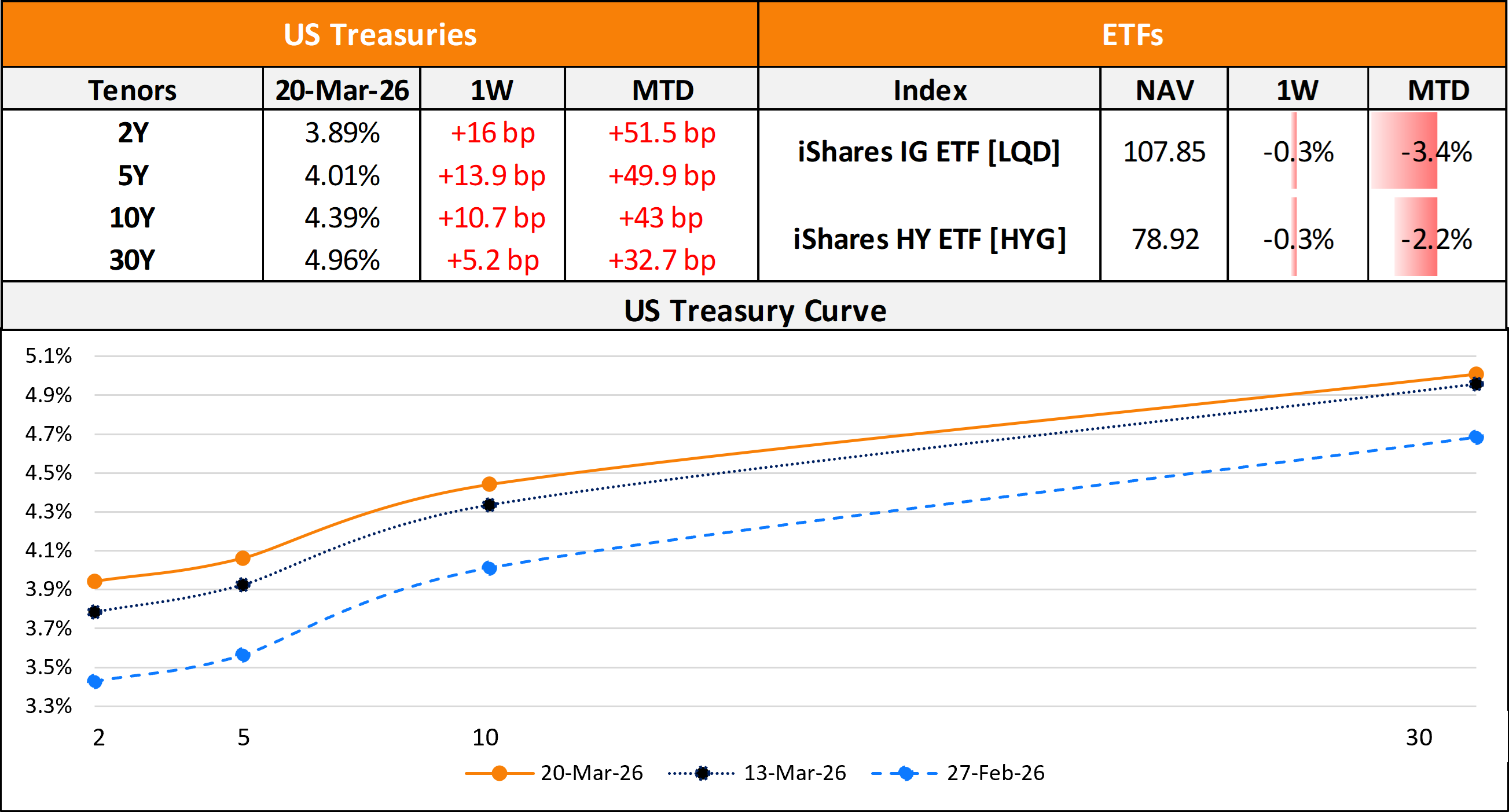

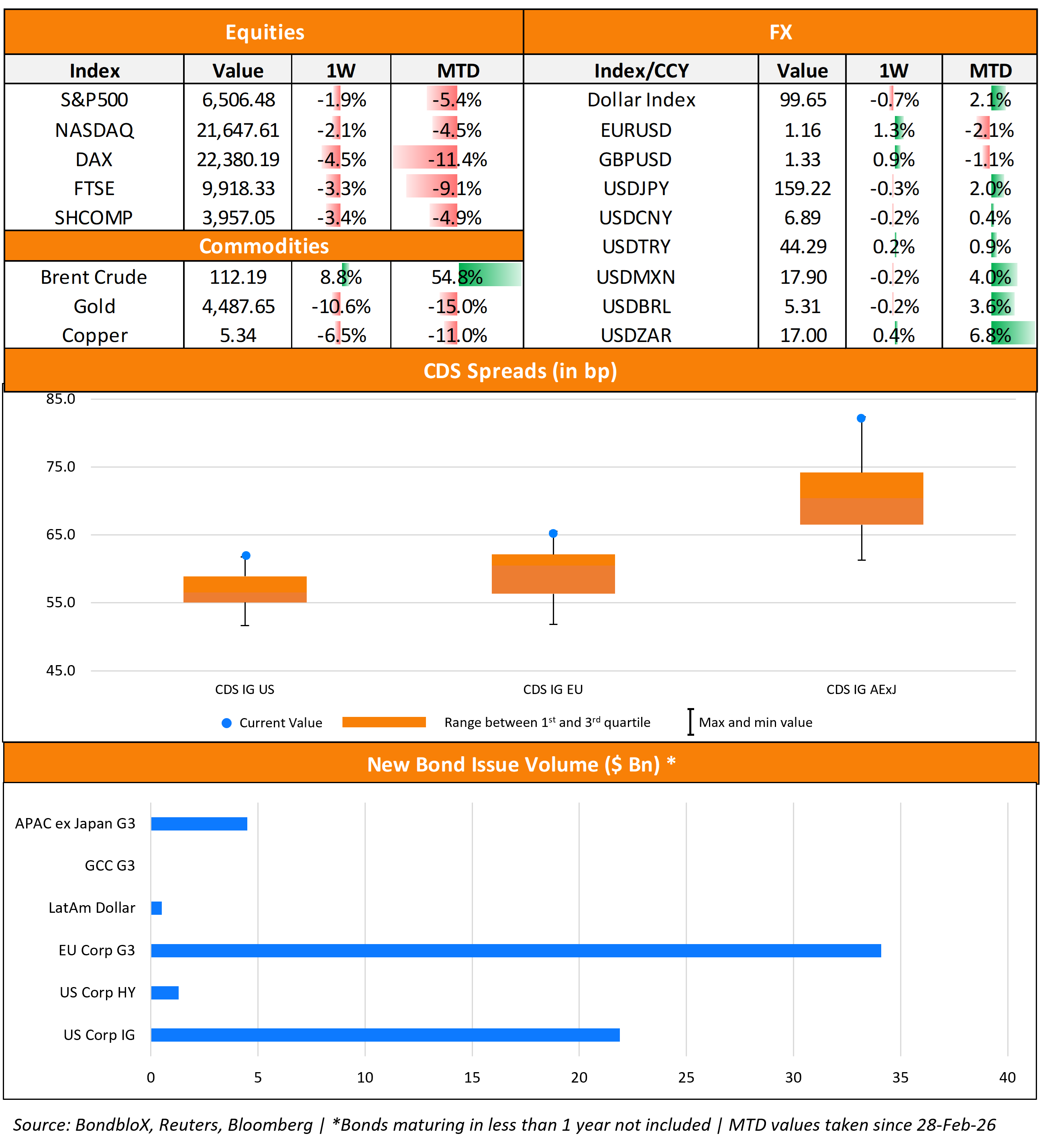

US primary market issuances fell to $23.3bn vs. a massive $114.9bn in the week prior to it. IG issuers took up $21.9bn of the total, led by Novartis’ $11bn seven-part deal and Waters Corp’s $3.5bn five-trancher. HY deals stood at $1.3bn, with volumes led by Emera US’s $750mn issuance and Infinity Natural Resources’ $550mn issuance. In North America, there were a total of 34 upgrades and 28 downgrades, across the three major rating agencies last week. US IG funds saw $4.79bn in inflows during the week ended March 18, adding to the $3.29bn inflows seen during the week before that. US HY bond funds saw $3.34bn in outflows during the week, adding to the $1.53bn outflows seen in the prior week. This marked the sixth straight weekly outflow for high yield funds, and was the largest outflow since early April 2025.

EU Corporate G3 issuances rose to $34.1bn vs. $11.7bn a week earlier. BMW’s $3.7bn four-trancher led the tables, followed by Nebius Group’s $4bn two-part issuance and Deutsche Bank’s €3.2bn issuance. The region saw 26 upgrades and 18 downgrades across the three major rating agencies. Last week, the GCC dollar primary bond market saw no new deals as compared to $1.75bn in issuances seen in the prior week. In the Middle East/Africa region, there were no upgrades nor downgrades across the major rating agencies. LatAm issuance stood at $500mn vs. $570mn in new deals in the week prior led by sole deal by Banco Santander SA. The South American region saw 1 upgrade and 2 downgrades, across the three major rating agencies last week.

G3 issuances from the APAC ex-Japan region last week stood at $4.5bn vs. $4.4bn a week prior to it. ANZ Group’s $2.25bn issuance and Sydney Airport’s $1bn deal led the tables. In the APAC region, there were 3 upgrades and 14 downgrades across the three rating agencies.

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.