This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

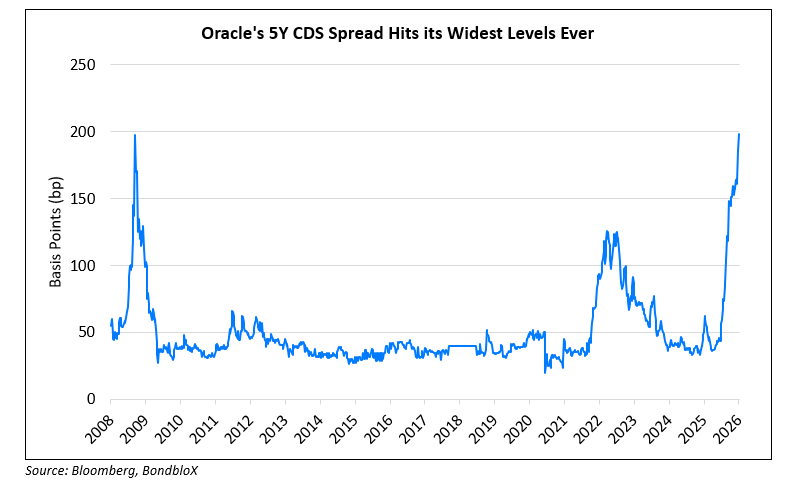

Oracle’s 5Y CDS Spread Hits All-Time Highs

March 31, 2026

Oracle’s 5Y CDS spreads exceeded 198bp, hitting its widest levels ever, surpassing the levels seen during the 2008 Global Financial Crisis. Since late-2025, Oracle has been seen as a barometer for gauging AI-related credit risk after big tech companies went on a borrowing spree to fund and develop AI-based infrastructure. Analysts note that investors are focused less on the company’s top-line momentum and more on when Oracle can convert its capital expenditure into sustainable earnings and cash flows. Earlier this year, Oracle was sued by bondholders in a proposed class action suit, alleging that the company had concealed its need to issue significant additional debt to fund its massive AI infrastructure buildout. Oracle issued $18bn in the primary markets in October 2025 and again raised another $25bn in February 2026. Oracle is currently rated Baa2/BBB/BBB (Moody’s/S&P/Fitch).

Oracle’s dollar bonds were trading stable with its 4.125% 2045s at 68.6, yielding 7.2%.

For more details, click here

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.