We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

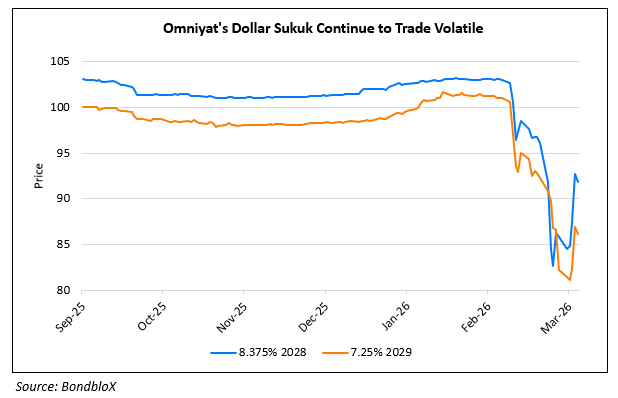

Omniyat Highlights Its Strong Liquidity; Dollar Sukuk Continue to Trade Volatile

March 27, 2026

Dubai-based luxury developer Omniyat pushed back against a potential Fitch downgrade, by highlighting that its liquidity position is strong. As of December 2025, the company held over AED 5.3bn ($1.44bn) in total liquidity. This included AED 2.7bn ($740mn) in unrestricted corporate cash, which was further boosted by a AED 2.2bn ($600mn) sukuk issued in March 2026. It claims this is enough to cover its next major debt obligation — a $500mn 8.375% sukuk due 2028 without needing new sales, collections, or refinancing. Last week, Fitch placed Omniyat’s BB- rating on Rating Watch Negative, citing geopolitical risks from the Iran war. This risk emanating from the war could dampen housing demand in Dubai, increase unsold inventory, and raise cancellation risk across the Gulf region, its analysts noted. Omniyat’s overall debt profile comprises three sukuk totalling $1.5bn, with near-term bank debt maturities of only ~AED 60mn ($16.3mn) in 2026 and ~AED 150mn ($40.8mn) in 2027. Omniyat’s dollar sukuk have dropped by almost 10 points across the curve since the start of the US-Iran war and continue to trade volatile.

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.