This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Mongolia, CICT Launch Bonds; Haven Assets Gain on Middle East Risk-off

March 2, 2026

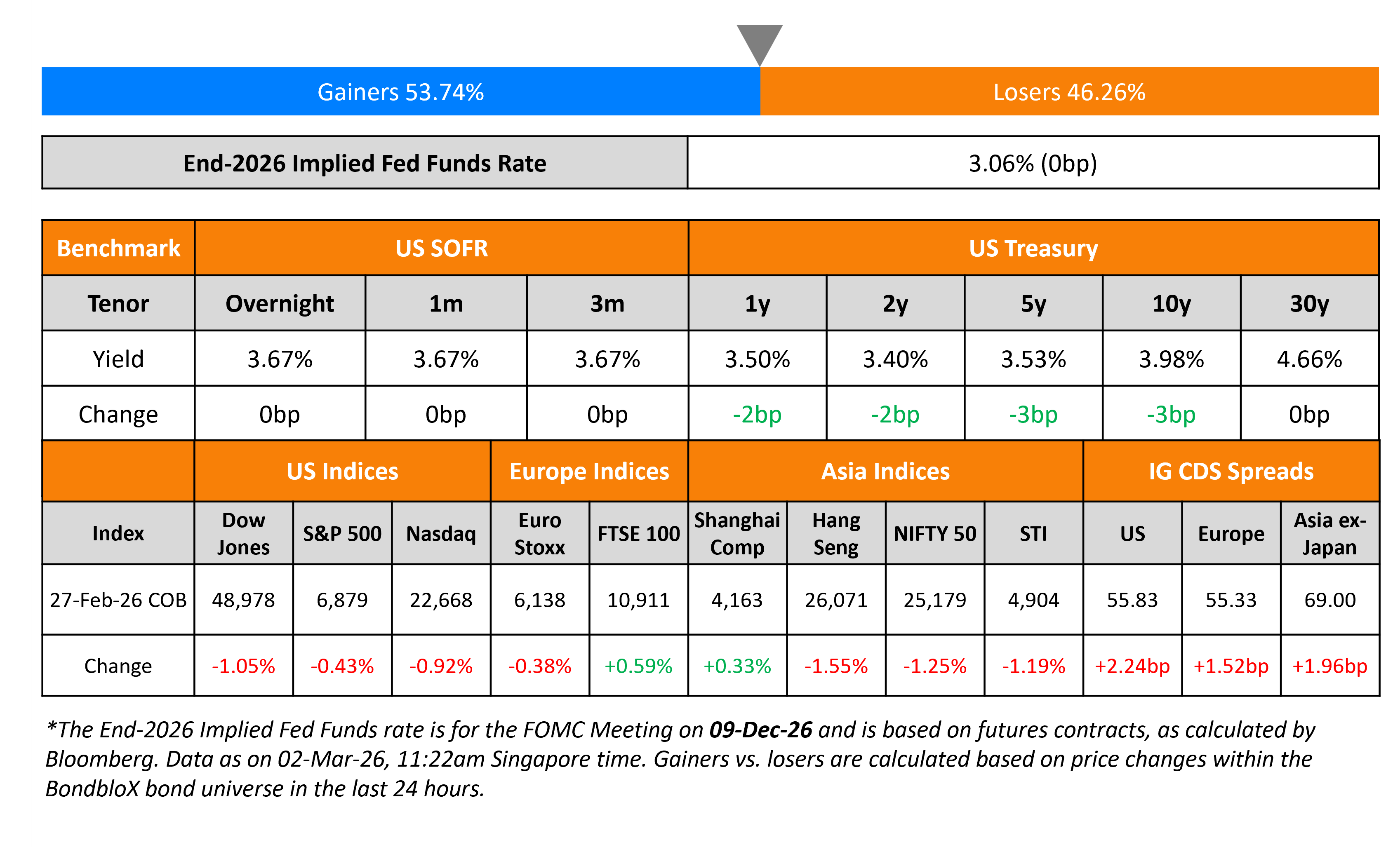

US Treasury yields were lower by 2-3bp across the curve. Markets have opened this morning with a risk-off sentiment with haven assets gaining amid the geopolitcal risks arising out of the Middle East. Over the weekend, the death of Iran’s Supreme Leader Khamenei was confirmed during the US-Israel airstrikes. In response, Iran launched a series of missile and drone attacks targeting US military bases across the gulf, impacting nations like Bahrain, UAE, Qatar and Jordan. Oil prices jumped by 10% due to the disruptions in the Strait of Hormuz and the missile strikes in the Middle East. Gold prices rallied, crossing the $5,350/oz mark. On the data front, US PPI for January rose by 0.5%, better than expectations of 0.3%. The core reading rose by 0.8%, again beating expectations of 0.3%.

Looking at US equity markets, the S&P and Nasdaq ended lower by 0.4% and 0.9% respectively. US IG CDS spreads widened by 2.2bp and HY CDS spreads were 10.6bp wider. European equity indices ended mixed. The iTraxx Main CDS spreads were 1.5bp wider and the Crossover CDS spreads were 5.2bp wider. The Dubai and Abu Dhabi stock markets will remain shut for two days. Asian equity markets have opened lower this morning. Asia ex-Japan CDS spreads widened by 2bp.

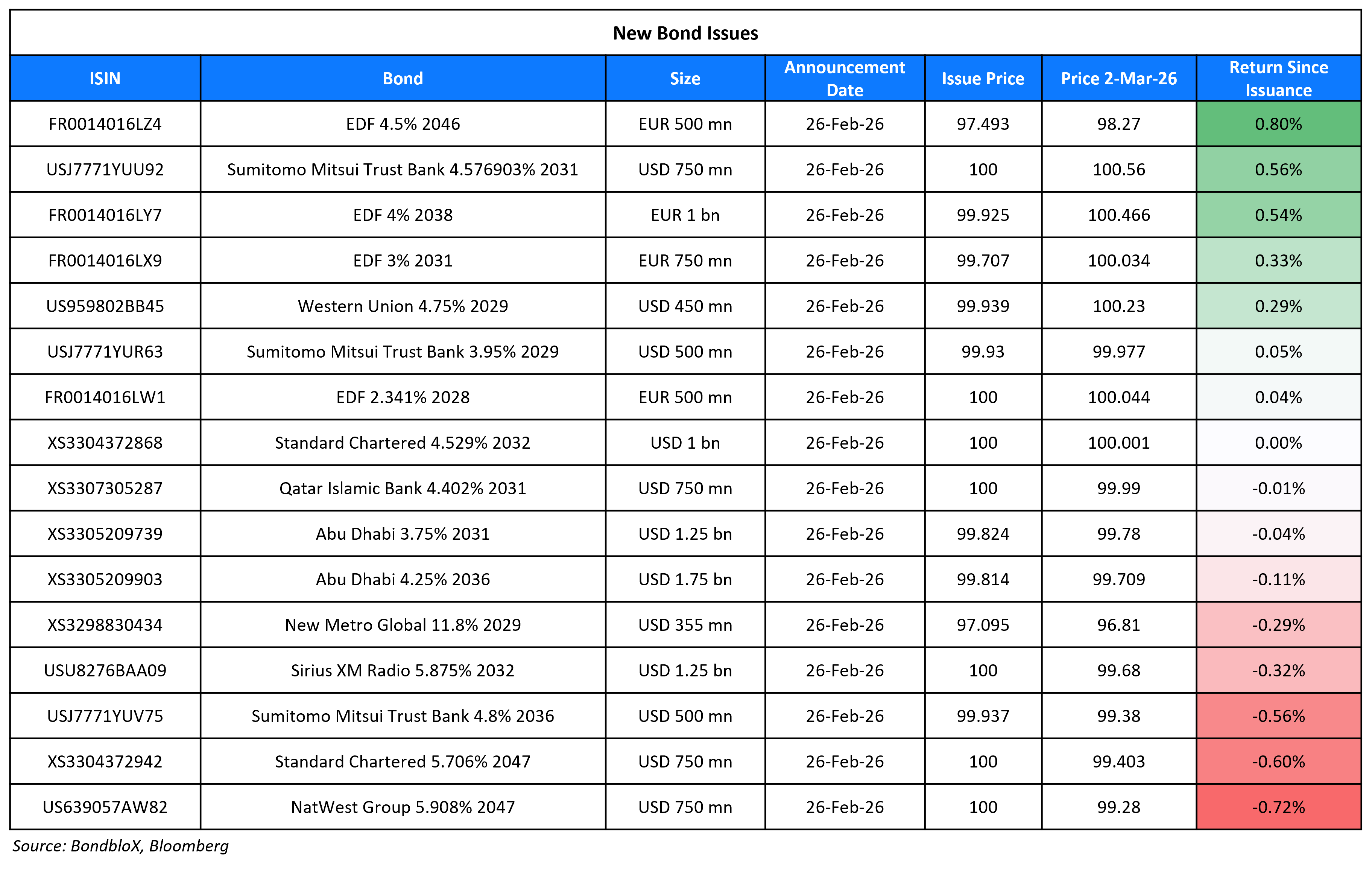

New Bond Issues

-

CICT S$ 5Y at 2.4% area

-

The Government of Mongolia $ 6Y at 6.3% area

New Bonds Pipeline

- NBN A$ 10Y and/or 15Y sustainability bond

Rating Changes

- Moody’s Ratings upgrades Tutor Perini’s CFR to B1, outlook is stable

- MHP SE Upgraded To ‘CCC+’ On Completed Debt Refinancing; Off CW Positive; Outlook Stable

- Fitch Downgrades Cosan’s IDRs to ‘BB-‘; Places Ratings on Rating Watch Negative

- Moody’s Ratings has downgraded Dow’s rating to Baa3 from Baa2; Outlook negative

- Mercer International Inc. Downgraded To ‘CCC+’ From ‘B-‘ On Cost Pressures And Lower Cash Flow; Outlook Negative

- Fitch Downgrades Huntsman Corp. to ‘BB+’; Outlook Negative

- Xerox Corp. Secured Debt Ratings Lowered, Recovery Ratings Revised Following Joint-Venture Financing Transaction

- Moody’s Ratings says Warner Bros. Discovery, Inc.’s ratings remain on review for downgrade after the Paramount acquisition announcement

- Paramount Skydance Corp. Ratings Placed On Watch Negative Following Completion Of Bidding War For Warner Bros. Discovery

- Portugal Outlook Revised To Positive On Resilient Economy And Declining Debt; ‘A+’ Ratings Affirmed

- Fitch Places Metinvest’s ‘CCC-‘ Rating on Rating Watch Negative

Term of the Day: Haven Assets

Haven assets aka ‘safe havens’ refer to those class of assets/securities which are in demand when market conditions deteriorate. Examples of haven assets include US Treasury bonds, German Bunds, UK Gilts, Japanese Government Bonds (JGBs) and gold. These are in contrast to ‘risk assets’ which are generally those assets/securities that are in demand when market conditions are buoyant, like equities, real estate and high yield bonds.

Talking Heads

On selling German Bunds After Best Start in Six Years – Barclays

Bunds are now the most expensive they’ve been relative to short-dated interest rates swaps since March 2025 … Selling German debt “leans against the wind, given the mood music in markets” and that a further flight to safety could work against the trade”

On analysts reacting to US-Israel strikes on Iran

Helima Croft, RBC Capital

“The ultimate oil price impact of today’s military action will likely hinge on whether the IRGC folds in the face of the aerial onslaught or if it pursues further escalatory actions… all of this is taking place against a backdrop of minimal OPEC shock absorbers”

Jorge Leon, Rystad Energy

“Alternative infrastructure in the Middle East can be used to bypass the Strait’s flows, but the net impact remains an effective loss of 8-10 million bpd of crude oil supply”

Eurasia Group

“Oil prices will rise sharply when markets open. Should the conflict continue into Sunday, oil prices are likely to respond by increasing by $5-10 above the current $73 baseline”

On Global Credit Spreads Widening Most in Months as Strains Mount

Clement Chong, Eastspring Investments

“Valuations in the Asian market have tightened in sync with developed markets like the US, and we will not be immune to volatility there”

Zerlina Zeng, CreditSights

“For now, we don’t see severe contagion risk to public credits”

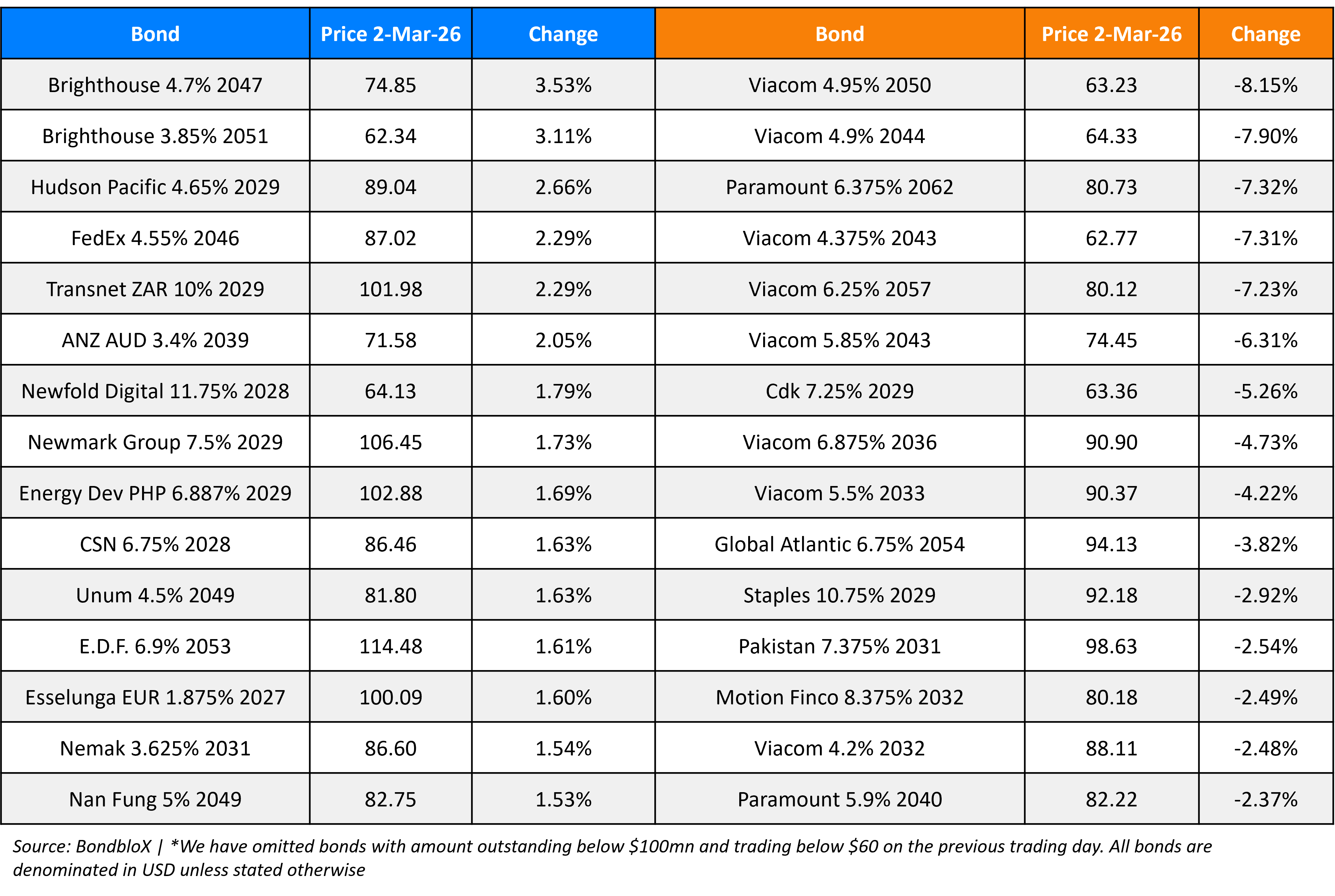

Top Gainers and Losers- 02-Mar-26*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.